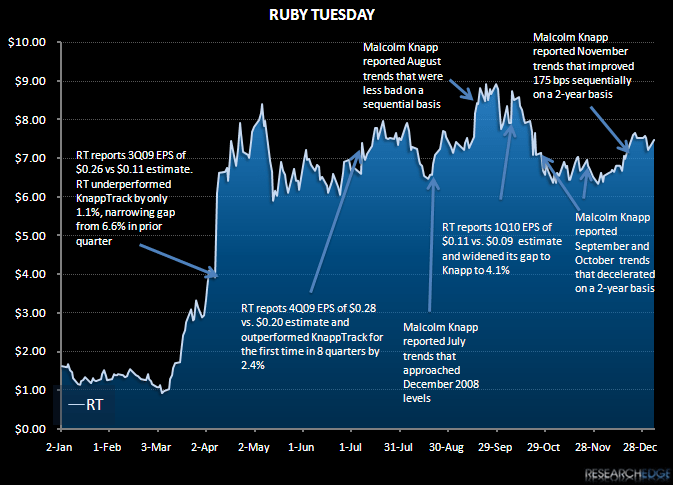

Ruby Tuesday is scheduled to report fiscal 2Q10 earnings after the close tomorrow and I am expecting EPS to come in a penny better than the street’s estimate of a loss of $0.02. Fiscal 2Q10 marks RT’s last quarter of relatively easier comparisons from both a top-line and EBIT margin perspective. I am expecting company-operated same-store sales growth to come in -2% relative to the street’s -2.7% estimate. On a 2-year average basis, this assumes a 50 bp acceleration from the first quarter, a level that is even with that of the casual dining industry as measured by Malcolm Knapp. As it relates to YOY comparisons for both RT and the industry as a whole, if RT’s trends improve by the same amount on a 2-year average basis as the industry in RT’s fiscal 2Q, the company’s gap to Knapp will narrow on a sequential basis to about 3% from 4% in 1Q10. For reference RT’s performance has gotten better on a sequential basis relative to the industry for the last six reported quarters.

Even with the relatively easier EBIT margin comparison from 2Q09, I am expecting about 70 bps of contraction in 2Q10 (following a nearly 100 bp improvement in 1Q10). In the back half of the year, however, margins will come under increased pressure as RT will be lapping two quarters of 200-plus bps of YOY improvements. Making the second half more difficult is the fact that RT will be lapping lower SG&A spending as a result of the company’s increasing its span of control for both regional and area supervisors in the back half of last year and lower depreciation expense from the 3Q09 closures.

Relative to RT’s full-year guidance, I am comfortable with the company’s ability to achieve EPS of $0.50-$0.60; though I think the lower end of the range is more likely. Management gave same-store sales growth guidance of -1% to -3%. Again, I think the lower end is more likely and could even be at risk as it assumes more than 300 bps of sequential improvement in 2-year average trends from 1Q10 to 4Q10. For reference, same-store sales comparisons get relatively more difficult in the back half of the year so even if 2-year trends continue to improve, numbers will likely begin to come down on a 1-year basis in 3Q10.

This improvement in top-line trends will have a lot to do with how the overall industry fares going forward (we will have to see if the better November trends are sustainable), but RT is also lapping its significant promotional efforts from January 2009 in fiscal 3Q10. In the last couple of quarters, RT’s top-line outperformance has been driven by traffic growth. This growth has come at the expense of average check growth. On RT’s 1Q10 earnings call, management stated it still has a goal to increase average check to the $12.50 to $14.50 range from the current mid-$11 range and that with customer traffic up, the company can now work on increasing average check. It will be important to see if the company can continue to sustain traffic growth with average check growth and the true test will come in 3Q10.

One area of management’s guidance that my numbers don’t currently match up with is the company’s outlook for restaurant level margins to decline 50 bps to 150 bps. I am modeling closer to a 160 bp decline in margins for the full-year. Obviously, where these numbers come in will be driven largely by how same-store sales trends play out for the balance of the year. RT’s restaurant level margins have declined on a YOY basis for the last 11 quarters. The YOY declines have continued despite the sequentially better same-store sales numbers because the company’s food costs as a percentage of sales have come under increased pressure from the company’s discounting and promotional efforts. If the company is able to increase its average check and traffic in the back half of the year, then it will take some of the pressure off the food cost line and subsequently, restaurant level margins.

Fiscal 2010 should be another year of strong free cash flow for RT. This free cash flow along with the $73 million in proceeds from the company’s equity offering in 1Q10 should allow the company to achieve its goal of paying down $165 million to $175 million of debt during the year.

RT has grossly outperformed its peers in the last year and that is with the group on average trading up 76%. In the last six months, this outperformance has narrowed with RT up 10.7% versus its peers +9.6% move. With RT’s top-line outperformance relative to Knapp Track likely to narrow from 1Q10 levels and margin comparisons getting more difficult in the back half of the year, I think it is unlikely that RT’s stock will have another year of outperformance.