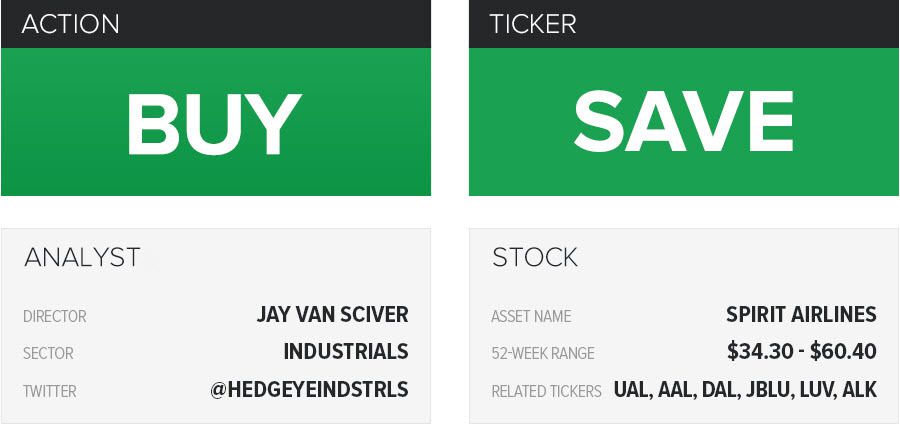

THE HEDGEYE EDGE

Given the recent decline in shares of SAVE, we see an entry opportunity into a major structural change in the airline industry: the rise of the ultra-low-cost carrier (ULCC). We have waited quite a while for a chance to issue a long call on Spirit, as we think some investors incorrectly specify the market potential for ULCCs. We expect SAVE to benefit as they gain scale and leverage their lower cost operating model.

INTERMEDIATE TERM (TREND)

SAVE does have a few intermediate concerns: the pilot’s contract and the current pricing war with UAL. Given these issues, the selloff in the stock may not correct immediately. But we do believe it turns by 1Q2018 as we do not think these issues will remain. Spirit is a competitively advantaged, growing airline that is valued more cheaply than non-growth, less profitable peers.

LONG TERM (TAIL)

As a high quality industrial transport, SAVE deserves revaluation, legacies do not. In terms of entry, we have waited a long time to issue our long call on SAVE. This is a decent spot to enter a young ULCC, as the data points to sustained ULCC growth. SAVE’s flexibility to compete, relent or acquire to fend off competitors, bodes well for a long-term investment worth ~$60/share, all else being equal.

* * * *

Click here or the image below, to watch a brief video from a recent institutional research call on Spirit Airlines (SAVE).

In it, Hedgeye Industrials analyst Jay Van Sciver explains why the “Legacy players have consistently lost share.” In particular, the highest cost players, like United Continental (UAL), have a real problem. “They are basically ceding share to keep pricing high,” Van Sciver says. One possible way to play this trend? Get long Spirit Airlines (SAVE).

ONE-YEAR TRAILING CHART