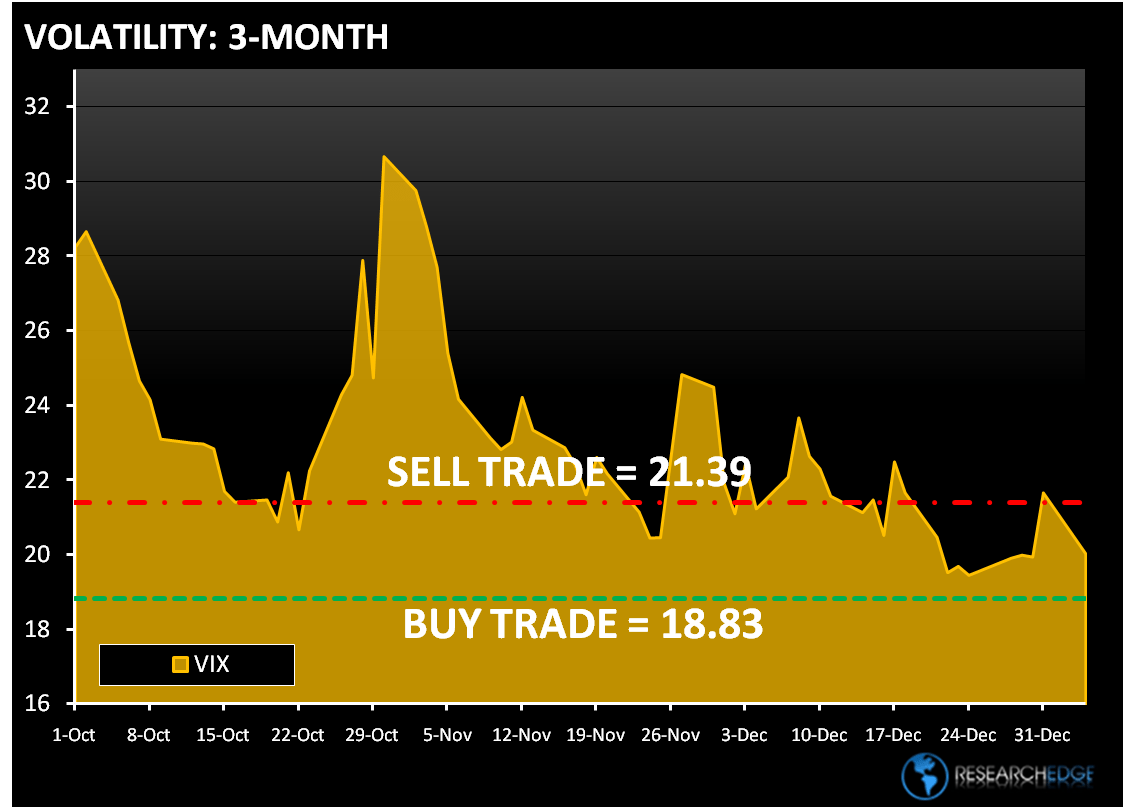

The S&P 500 started out the new decade on a strong note on Monday, with the index up 1.6%. The rally was broad based as all the major indices finished at least 1.5% higher on the day. The Research Edge quant models now have all nine sectors positive on TRADE and TREND. It should be noted that the move came on very light volume.

On the MACRO front there were a number of positive dynamics at work yesterday, including a batch of largely upbeat global PMI readings, particularly out of China and the US. The improved PMI readings led to a big move in the high beta RECOVERY trade. The official December Chinese PMI rose to 56.6 from 55.2 in November, expanding for the tenth straight and marking the highest level since April of 2008. In the US, ISM manufacturing rose to 55.9 in December from 53.6 in November, the highest level since April of 2006. December marked the fifth consecutive month of manufacturing expansion. Importantly, the forward-looking new orders component rose to 65.5 from 60.3.

The two best performing sectors were Energy (XLE) and Materials (XLB). Both sectors have the most leverage to the RECOVERY theme and a weaker dollar. The Dollar index declined to 77.52, down 0.43%.

Rounding out the top three best performing sectors was the Financials (XLF). The XLF posted its best one-day gain since November 30, 2009. Within the XLF, the banks snapped a four-day losing streak.

Next to the Utilities, the two notable underperformers were the Consumer Staples (XLP) and Consumer Discretionary (XLY). The retail group was a notable standout with the S&P Retail Index finishing unchanged on the day.

The range for the S&P 500 is 12 points or 0.5% upside and 1.0% downside. At the time of writing the major market futures are trading flat on the day.

Copper is trading lower ending a sixth day winning streak. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.25) and Sell Trade (3.42).

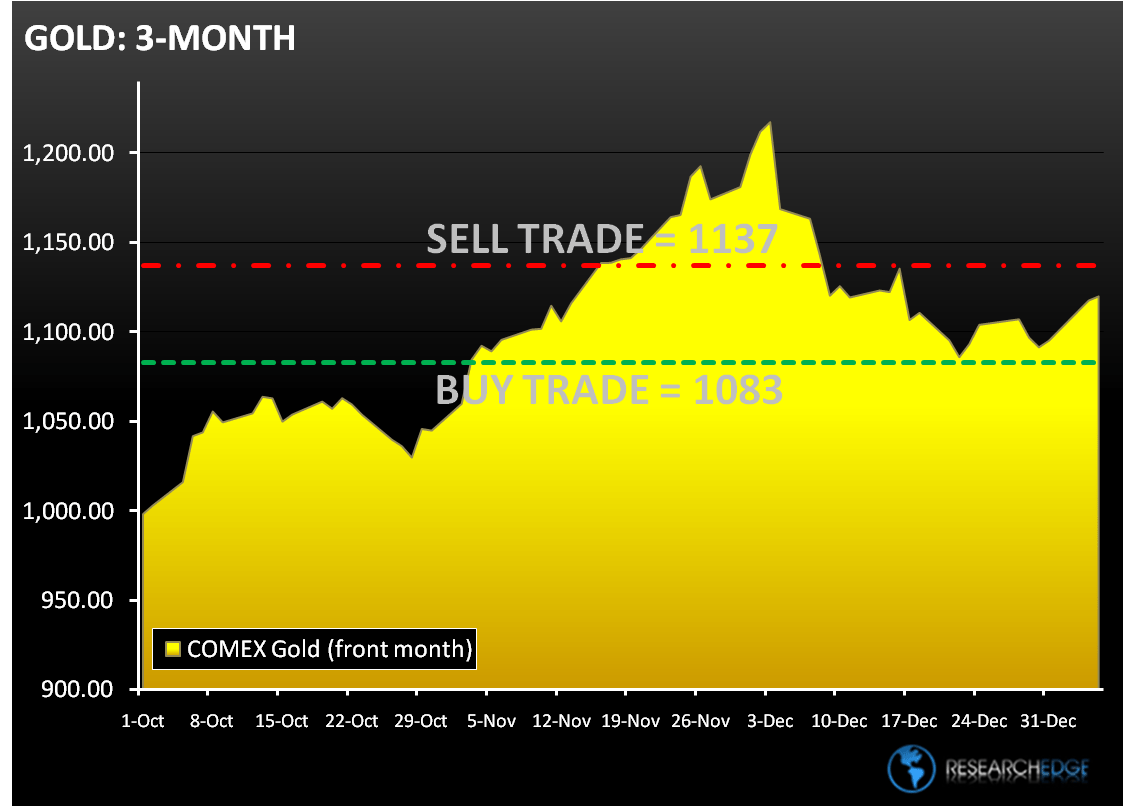

GOLD continues to trade in a very narrow range around $1,127/OZ. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,083) and Sell Trade (1,137).

Crude oil traded near a 14-month high as cold weather in the U.S. and signs of economic recovery are helping demand. The Research Edge Quant models have the following levels for OIL – buy Trade (77.85) and Sell Trade (82.59).

Howard Penney

Managing Director