Some people think I am trying to be funny when I call He Who Sees No Bubbles (Bernanke) names. Not calling these v-bottom charts in macro for what they are isn’t funny at all. For those who continue to be willfully blind, it’s just professionally embarrassing.

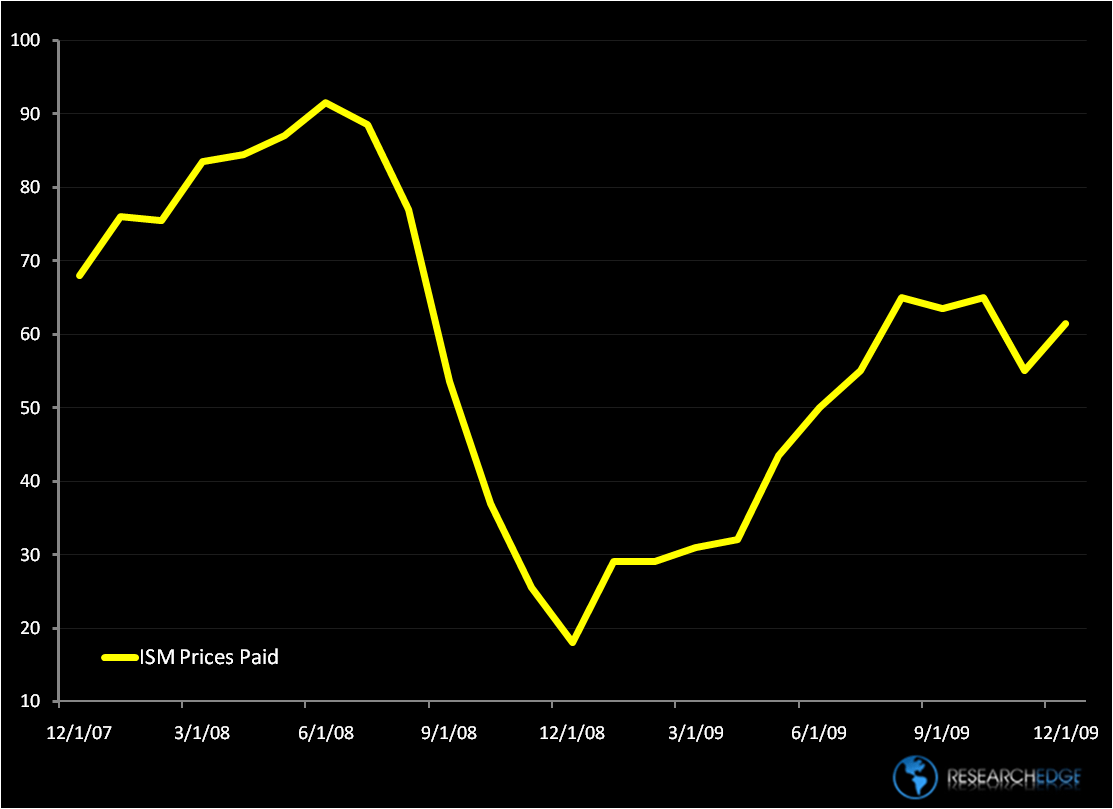

Below, we have attached the latest readings on from the ISM: the Manufacturing Index and Prices Paid.

- ISM Manufacturing for December just made another higher-high at 55.9 (versus 53.6 in November).

- Prices Paid continue to ramp, coming in at 61.5 in December (versus 55 in November).

On the ISM Manufacturing reading, never mind 2008, this chart is comfortably higher now than where it was in late 2007.

On the Prices Paid survey, is it still below the 2008 highs? Yes, but remember that those highs also carried $152/barrel oil prices!

In the Virtual Portfolio we bought the US Dollar today. He Who Sees No Charts (Bernanke) is running out of pictures that both the bond and currency markets want to ignore. Yields across the Treasury curve continue to breakout to the upside. The US Dollar is on sale today, but holding its new intermediate term TREND line of support ($76.31).

KM

Keith R. McCullough

Chief Executive Officer