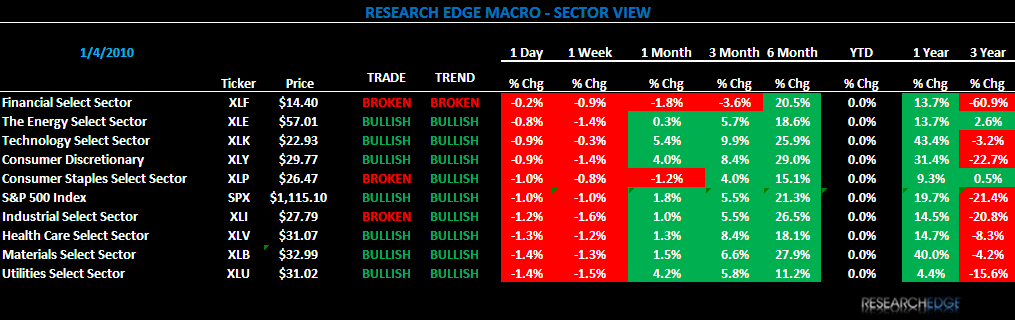

US equities finished lower in their final day of trading for 2009 with the Dow declining (0.87%), the S&P down (1.01%), the NASDAQ (0.72%) and the Russell (1.37%). Last Thursday, the Industrials (XLI) and Consumer Staples (XLP) joined the Financials (XLF) and are now broken on TREND.

In the last week of trading for the year the S&P 500 declined 1.0%. On the MACRO calendar the week's economic data points included: the October S&P Case-Shiller 20-city home price index, December consumer confidence, December Chicago PMI and weekly initial claims; all came in better than expectations. There was nothing in the MACRO data points to account for a shift in sentiment surrounding the momentum behind the RECOVERY theme.

Corporate news flow was again on the light side last Thursday, with the Jobless claims data the only release of interest on the economic calendar. Initial claims fell 22,000 to 432,000 in the week-ended December 26th; the lowest level since July of 2008 and below the 460,000 consensus. The four-week moving average fell to 460,000 from 466,000 the week before.

The MACRO data points out of China continue to be a net positive; we believe that things will slow as we move thru the first quarter. In China, the official purchasing managers index improved to 56.6 last month up from 55.2 in the previous month. China's manufacturing sector is now expanding at the fastest pace since the financial crisis in late 2008. The index’s low was at 38.8 in November 2008. Domestically, we are looking for additional data points on the RECOVERY theme with the release of December ISM manufacturing.

The Utilities (XLU) and the Materials (XLB) sectors were the two worst performers last Thursday, with the Road (R) and Air Freight (FDX) names performing the worst. Financials (XLF) and Energy (XLE) were the best relative performers, with the larger-cap banks (WFC) and brokers (GS) among the standouts. Every sector declined last Thursday.

Last Thursday, the VIX closed at 21.68, up 8.6% day-over-day; last year the VIX declined 44.7%. The Dollar Index traded in a tight range last week, and was down 4.2% for all of 2009.

Today, the range for the S&P 500 is 22 points or 2.0% upside and 1.0% downside. At the time of writing the major market futures are trading higher.

Copper is trading higher for a sixth day in London to a 16-month high as a strike began at the world’s second-biggest mine and manufacturing in China expanded by the most in five years.

In early trading today GOLD is trading in a narrow range around $1,095/OZ an ounce on Monday in a cautious start to the year after ending 2009 with their biggest absolute annual gain in three decades.

Crude oil rose for an eighth day, trading above $80 a barrel for the first time in seven weeks, as freezing weather and improving economic prospects around the world helped the outlook for demand.

Howard Penney

Managing Director