You know when you wake up, see a headline re one of you positions and you have one of those ‘oh crap, this sucks…’ moments? I don’t think we’ll have one of those with HBI Tuesday. And I’ll be shocked – literally I’ll fall out of my chair – if I see anything that’s a thesis-changer. I think this is ultimately a $5 stock, with the revenue and cash flow miss to support it. It’s the result of a decade’s worth of bad behavior fueled by misaligned incentives at the time of the IPO to get management paid in light of sticking with $2.4bn in debt from/by from Sara Lee. [Note, I was at Morgan then when we did the deal – well before current IR knew they’d have their current jobs. That’s not a dig. It’s a #fact]. But this is a BIG call for Hedgeye…and we risk-manage pretty much everything.

This cash flow miss – what should be a BIG one – is fueled entirely by deleveraging revenue miss(es) – both units and pricing – rising costs, deferred investments, deleveraging , weaker pricing (thanks in part to GIL), rising costs, eroding rate of special charges that are partially funding margins, and the inability to leverage interest expense (and 4.3x leverage) due to a series of (ultimately) dilutive acquisitions.

With nearly every ‘this company will implode’ call, as we know, the quarters leading up to the implosion include irrational cost cuts, channel stuffing, aggressive terms, and whatever a company (and Price Waterhouse Coopers) could do to push the needle on accounting – while staying on the legal side of questionable. In that vein, here are the things that could make Tuesday evening on the uncomfortable side if you’re big-time short this name…

- Revenue upside: The is a company that did four acquisition in conjunction with the CEO leaving and selling stock. Perhaps it’s irrelevant that HBI missed cash flow targets massively over that time period. But deals are boosting revenue by 12% per quarter, and will do so for another month. Check out CRI last week…it sandbagged revenue impact from its latest deal. There was a big guide down…but the revenue upside in the quarter mitigated a sell off.

- This Nanjing plant closure six months ago gives about a 170bp tailwind in gross margin to mitigate the margin pressure we should otherwise see in the core. It’s in our model, and it should push factory utilization to about 95%+ -- which is hardly sustainable and mitigates upside to actually grow. But still…

- Cotton should be a factor this quarter. HBI is attempting to pass through cotton costs while competitors are not – and while the channel is shrinking. We are modeling a small cotton impact assuming a yy increase of about 10% in pricing, but perhaps the company can pushed this fully out into 2018. And while it is losing space to pegs instead of ‘the valley’ at WalMart and Target. [none of those things make taking price easy]. But maybe the company actually gets price in the form of putting less value in the box/package. WMT is smarter than that. But still…

- Maybe its latest plan to perennially restructure and 1) grow sales, 2) while improving GM, 3) while cutting costs, 4) while working capital is a source of cash, while capex is declining’ actually works for a quarter – even though a company like Nike, Apple, and even Hedgeye are all incapable of doing that. But still…

- Amazon…This is a risk, not an opportunity. Period. HBI does not tier product – and arguably the category does not lend itself to doing so. Amazon, jet.com (and every start-up apparel e-comm player) opens up a distribution channel for every little brand out there (meundies, pair of thieves, Tommy John, etc…) that could not exist 10 years ago. I’m confident in McLean’s model in the negative organic growth but Amazon could prove itself to be ‘de-facto channel stuff’. Amazon makes up only about 2% of sales, so it would have to growth 200-300% to give HBI a chance at hitting revenue goals. It seems very unlikely, but still...

- Investment push… We’ve consistently seen HBI push both R&D, Marketing, and slotting fees over the past decade – usually to the tune or 2-3%Could we see further cuts in these critical areas to prevent a dividend cut and ultimate covenant breach? This is the most likely factor mentioned here…

Here’s the full investment thesis broken out in our latest Black Book…

HBI Black Book | The descent to sub-$10. LINK: CLICK HERE

Brian McGough

Here’s McLean’s model…

We’re Expecting the Following

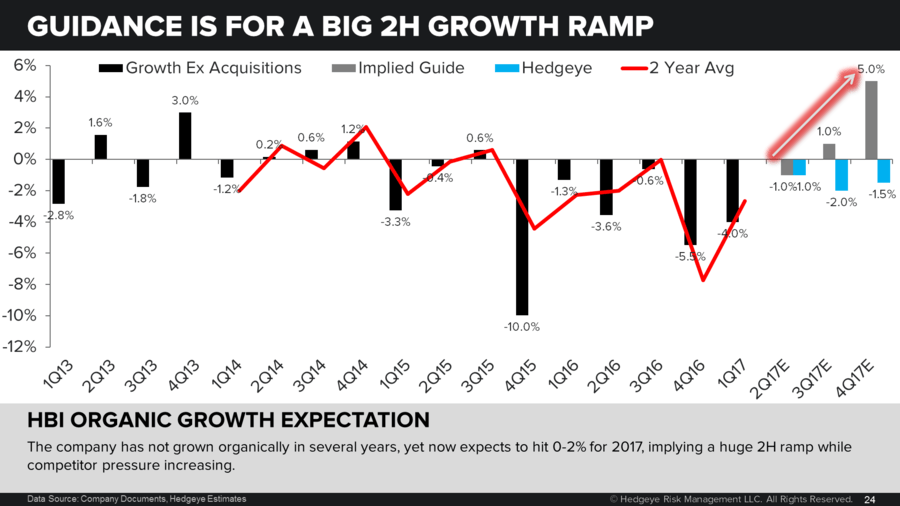

- 2Q EPS print in-line with consensus – setting up for a miss in 2H.

- Revenue slightly ahead of consensus driven entirely by 13.5% growth contributed by acquisitions -- organic growth down 1%.

- Gross margin will be up from the contribution of the higher retail penetrated international acquisitions and Nanjing tailwind. We’re giving the company the benefit of the doubt on this one – for now. That said…

- GM upside should be given back and then some on the SG&A line.

- As for guidance, we don’t foresee a major revision to the full year on this print. HBI management has historically delayed bad news as late as possible, and we think they'd rather give themselves more time to hit the big 2H goals rather than revise them down. This is not only in the c-suite – but rather a culture that allows bad news to be kept quiet at the divisional level while managers run faster to put out fires.

Trend Outlook

- Looking to the back half of the year, we think HBI will miss organic growth expectations. Guidance implies that the company will do low to mid single digit organic growth with the first 2 quarters of the year at -4 and -1%.

- If we're right, 3Q is a revenue miss and about a 10% earnings miss. Then 4Q revenue misses by about 4% and earnings by 20%+ and full year cash flow misses by 25%.

- If we had to point to one event where we are most likely to see fireworks, it would be 4Q. This is not a hedge to our thesis…it’s simple math.

- That is when the company is lapping a big inventory clean up while adding on 4 acquisitions and winding down operations in a major factory, as well as going against whatever purchase accounting adjustments that we think would obfuscate GAAP earnings.

- Last year management remained confident in cash flow targets until just weeks before the fiscal year ended, falling 20% short for the full year -- this means that the fourth quarter actually missed by 30-40% and management did not know until quarter close. And then it guided to organic growth for the year, and announced a 33% dividend increase (that’s 50% plus of our CFFO model). We think this year will play out similarly. Also, a reminder that Richard Moss, CFO since 2011, has announced he is leaving at the end of the year, and will most likely be gone before the 4Q print.