The S&P 500 finished higher by 1.1% in light, pre-holiday trading yesterday. The news worthy items in focus yesterday were the amended healthcare reform legislation out of the Senate, continued M&A activity and the sell-side generally getting more bullish at the end of the year.

Yesterday, Sanofi-Aventis agreed to acquire Chattem for $1.9B in cash. In addition, TreeHouse Foods gained 12.3% after announcing that it had signed a definitive agreement to acquire Sturm Foods, a private label manufacturer of hot cereal and powdered soft drink mixes.

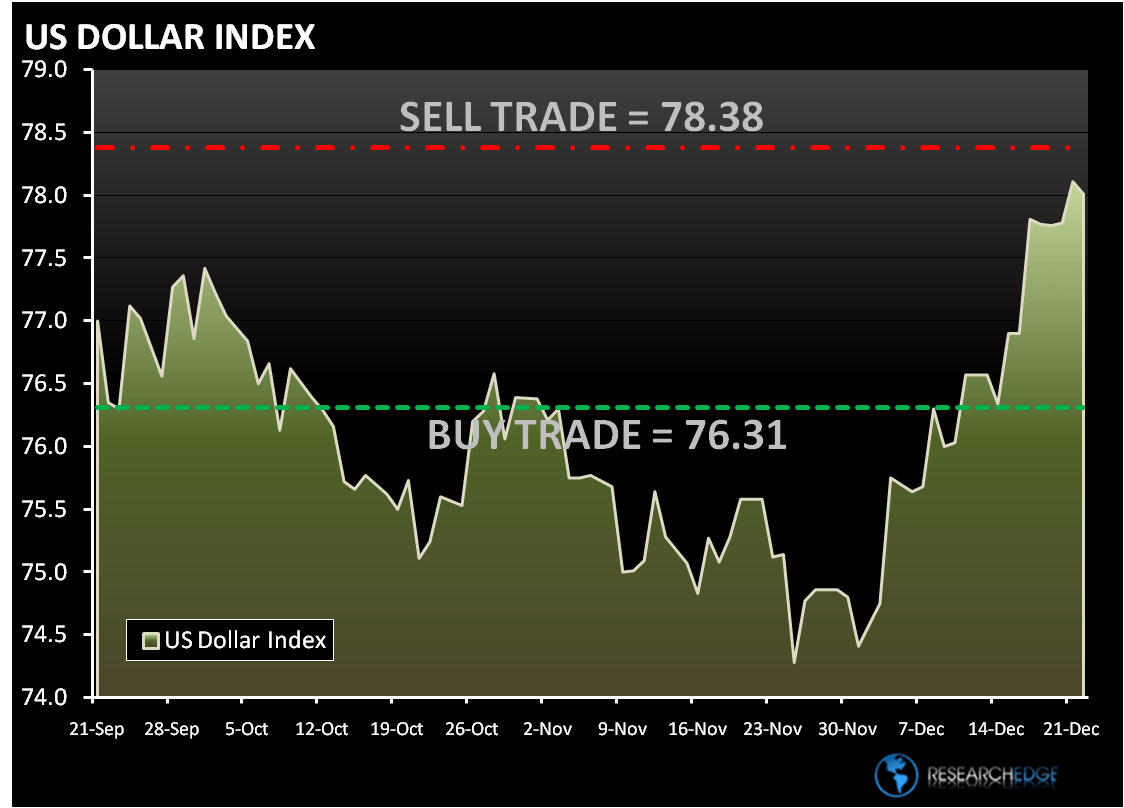

For the second day in a row the Dollar index was higher and stocks followed. Yesterday, the Dollar index rose 0.3% to 78.03. Every sector was positive on the day with the high beta Financials, Materials and Consumer discretionary leading the way. Utilities and Consumer staples were the two worst performing sectors.

The Healthcare (XLV) underperformed on a relative basis, but managed care stocks were among the best performers with the HMO index up 3.0%. The performance was driven by developments out of Washington as Senate Democrats reached a deal on healthcare reform legislation. The news of the demise of the elimination of the public option was welcome news. Also showing strong relative outperformance were the PBMs such as CVS +3.6%, ESRX +3.3% and MHS +1.7%.

The Materials (XLB) was the second best performing sector yesterday despite the continued bounce in the dollar. Upbeat sell-side commentary provided support for the steel and fertilizers sectors.

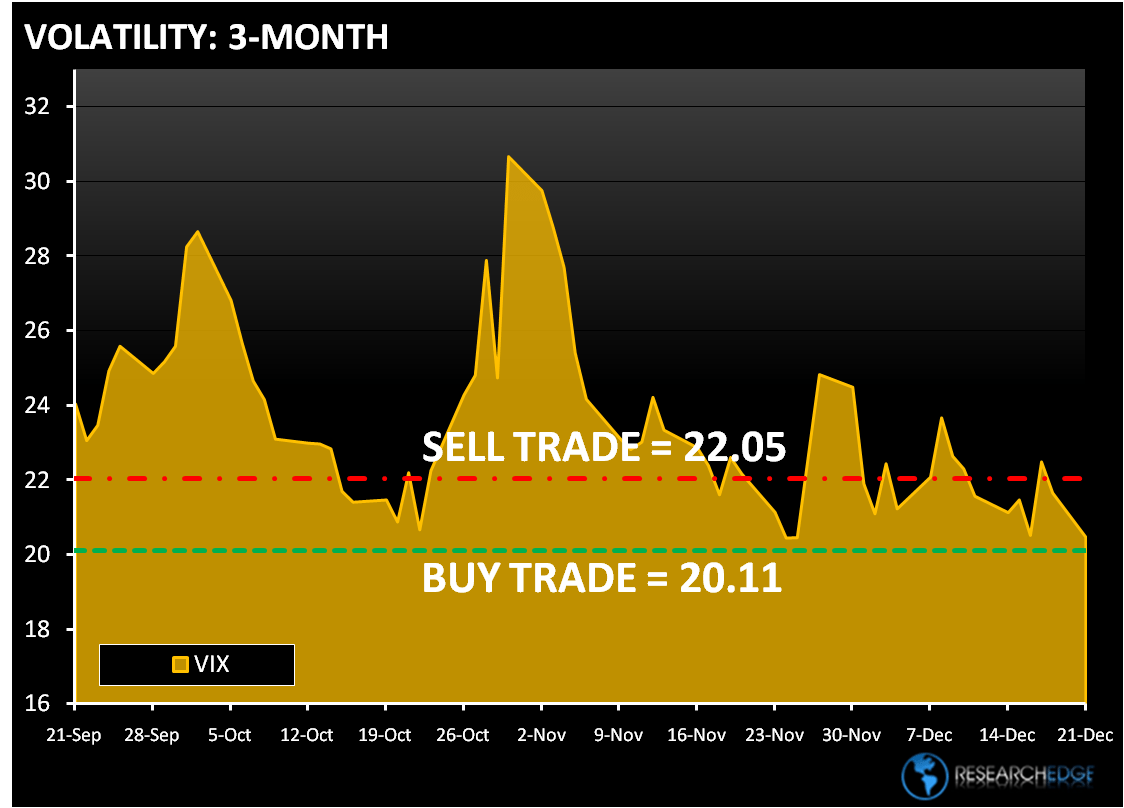

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 16 points or 0.5% upside and 1.0% downside. At the time of writing the major market futures are slightly higher.

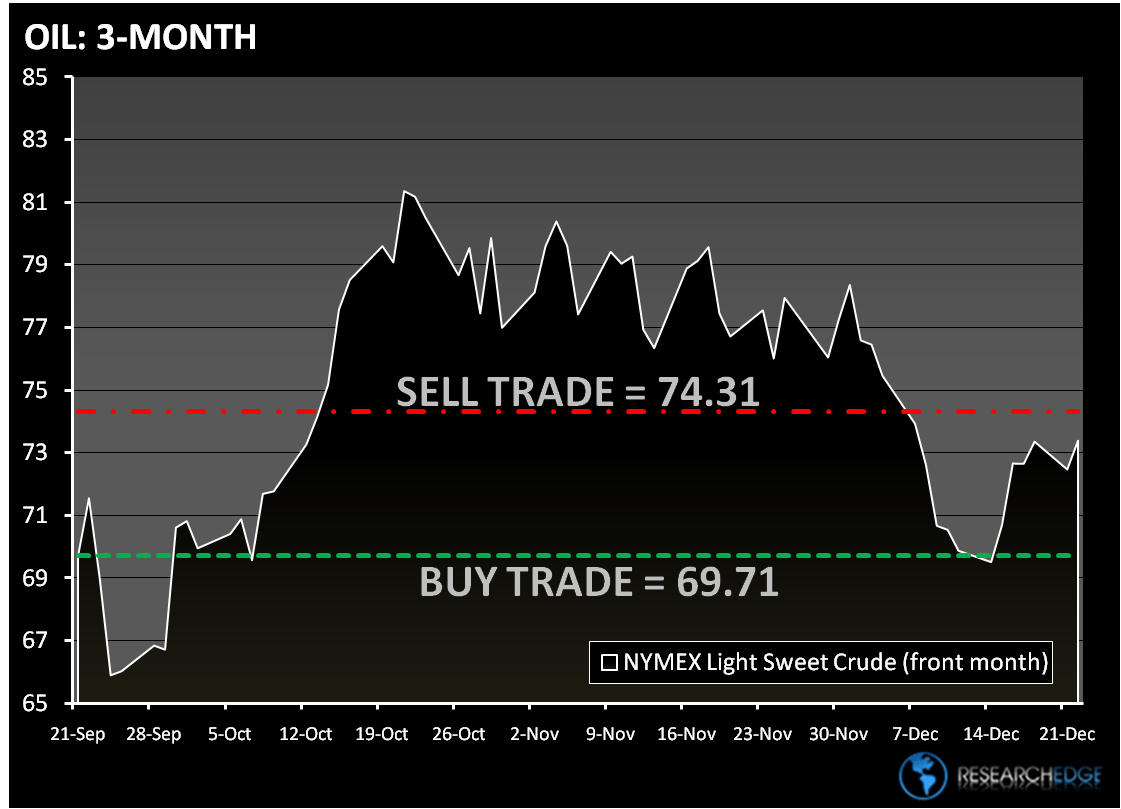

In early trading crude oil dropped after OPEC agreed to maintain production targets at a meeting in Angola. OPEC will hold total production quotas at 24.845 million barrels a day. The Research Edge Quant models have the following levels for OIL – buy Trade (69.71) and Sell Trade (74.31).

Gold declined $15.00 to 1,097 in Hong Kong; gold is trading at its lowest level in six weeks. The Research Edge Quant models have the following levels for GOLD – buy Trade ($1,090) and Sell Trade ($1,151).

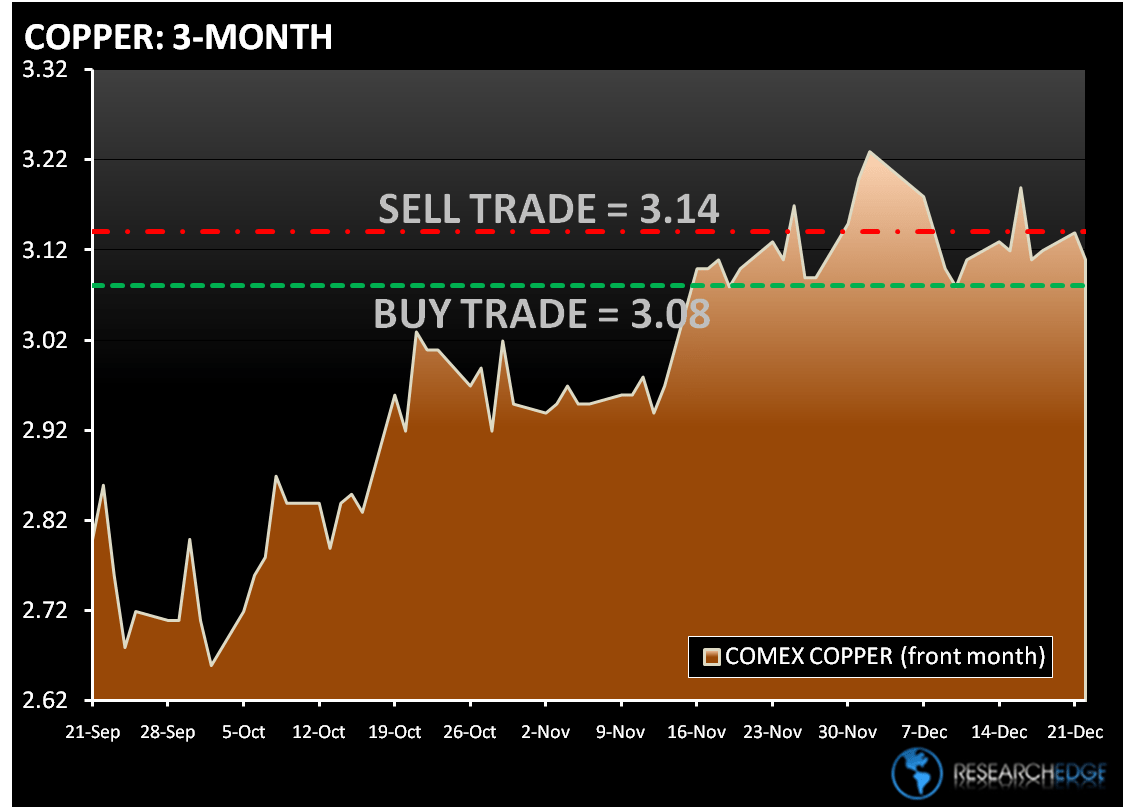

Copper fell in London as stockpiles expanded to almost a seven-year high, signaling demand related issues. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.08) and Sell Trade (3.14).

Howard Penney

Managing Director