THE HEDGEYE EDGE

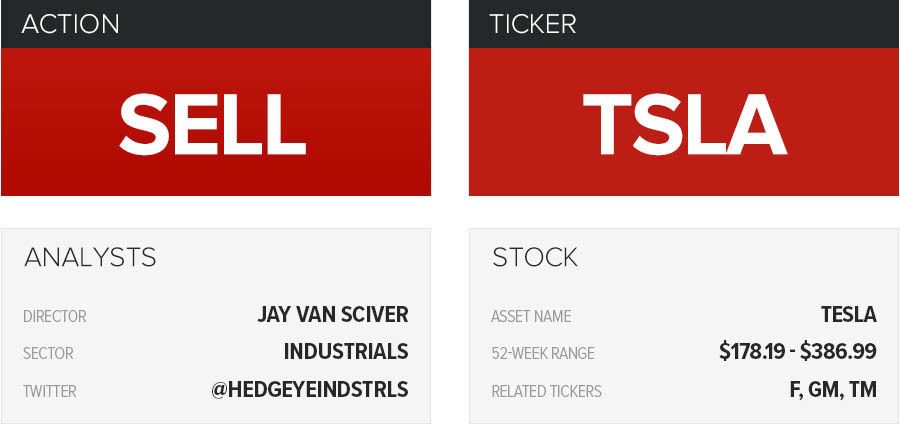

We see Tesla (TSLA) underperforming as the company’s exciting concepts transition to mundane execution. Concepts, ideas, and vision can easily win the market’s beauty pageant. Grinding out a cheap version of a high-end platform in a competitive market, with a less tolerant customer and expiring tax credits? That gets ugly.

The goal in a story stock is to anticipate the next chapter. Tesla’s valuation is silly, and we suspect most sophisticated investors realize it. Short squeezes, as we would characterize the recent move in Tesla shares, often prove attractive short entry points. Currently, many longs are gloating and shorts are no doubt miserable. All this drama comes just ahead of new competition that may permanently degrade Tesla’s growth prospects. Longs should be fearful and shorts greedy, as we see it.

INTERMEDIATE TERM (TREND)

We are reasonably confident that behemoths like Daimler, VW, Tata, Toyota, or GM would be able to introduce credible competing EV cars. Products are absolutely entering the market, from what we can see. VW, for example, is obligated to invest $2 billion in zero emission vehicle infrastructure, access, and awareness as part of its emissions settlement. VW plans to have 30 EV models by 2025 across its brands (Audi, VW, Porsche….), already has the Audi e-Tron Sportback in testing, and claims that “being the best doesn’t always mean being the first.” Daimler is investing $11 billion in EVs and has (literally) laid the foundation for its own battery facility, to be complete by 2020/2022. GM already has the Bolt, Nissan can build the Leaf 2 on an existing platform, and Jaguar is introducing the i-Path in Europe this fall. Competition is both credible and reasonably imminent.

Realistically, Tesla has a high cost footprint, lacks scale in its supply chain, and doesn’t do a great job designing cars for profitable manufacturing (at least so far, e.g. Model X). Other manufacturers can flex vastly more robust sourcing capabilities, with cost advantages over Tesla provided by an order of magnitude more scale. There is really no reason to believe a Daimler, VW, Toyota, or similar experienced OEM couldn’t design, price, market, and distribute profitable EVs.

LONG TERM (TAIL)

Tesla is a temporarily subsidized maker of capital goods. Established equipment markets have seen almost no competitive entry for decades; important structural hurdles typically preclude entry into markets like automobiles and electrical equipment. As Tesla’s tax credits are exhausted (in mid-2018 by our read), existing car makers can introduce EV models with as yet unused tax credits, adding to their already substantial edge. If Tesla even survives to profitability, it would be an exceptional accomplishment.

In reality, Tesla has sold about 120,000 cars in the US, its biggest market, (<0.1% of US fleet) and those sales are of heavily subsidized, high priced cars, produced at a huge loss over the last few years in a good economy, and mostly to huge fans/tech early adopters. It really doesn’t look like any of the other exponential growth winners (Amazon, Apple, Google, etc.). Tesla will compete at a tax credit disadvantage on Model 3 orders going forward, b) entry into capital equipment is exceptionally difficult for structural reasons, c) Tesla doesn’t have an obvious path to profitability, and d) story stocks do not like dates with reality.

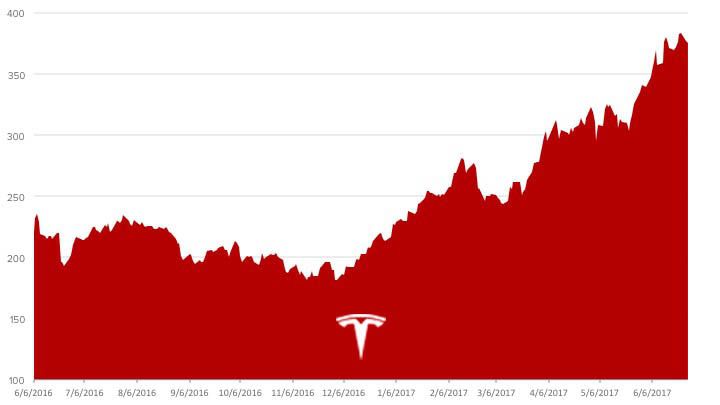

ONE-YEAR TRAILING CHART