Below are analyst updates on our fourteen current high-conviction long and short ideas. We will send Hedgeye CEO Keith McCullough's refreshed levels for each in a separate email.

Please note that we removed Utilities (XLU) from the short side and added Tesla (TSLA) to the short side of Investing Ideas this week.

IDEAS UPDATES

UUP

Early this week we made the decision to remove Utilities (XLU) from Investing Ideas on the back of one of our key themes in Q2: #Reflation’sRollover. Hedgeye CEO Keith McCullough summed up the effect of a flatter curve which directly benefits yield-sensitive sectors like utilities:

"With Reflation’s Rollover clearly keeping the long-end of the curve (bond yields) lower for longer, there’s no need to keep this under-performing SELL idea on."

Our longer-term structural view on the U.S. dollar hasn’t changed despite giving up ground so far in 2017, especially against the Euro. While not focal points for this weekend’s updates, myriad of market-related signals suggests the consensus crowd is increasingly favoring the Euro despite a relatively negative economic set-up through the rest of 2017 (Europe already had its big inflection in growth).

Focusing instead this week on long-term demographic trends which appear impossible to ignore, the U.S. is much better positioned well into the next decade.

Below we present a key chart in the currency debate which breaks out a country-specific position of demographic health which we’ll observe for a large chunk of our lives going forward.

What the chart shows is the relationship between the 65+ year old population and the growth rate in a developed economy’s peak spending demographic (35-54 year olds). Lower and farther right represents more risk. The Eurozone on the whole has a high 65+ population dependency ratio near 35% while the working age population will be declining steadily well into the future (the 5-year compound annual growth rate in that demographic is ~1% which will be a HUGE growth headwind. Ouch - A declining working age population that will be spending less but required to support a growing retired population. Something will have to give.

While the dollar looks to screen just o.k. in the chart with a population dependency ratio of ~27% and a flat 5 year growth rate in the 35-54 year old population, remember that every economy in the top left corner is in emerging market territory without globally renowned currencies. Among developed economies, the U.S. is in good shape, especially relative to the Eurozone economies.

EXAS

Click here to read our analyst's original report.

No update on Exact Sciences (EXAS) for this week’s Investing Ideas but Hedgeye Healthcare analyst Tom Tobin reiterates his long call on the company.

TWX

Click here to read our original analysis on why we think the AT&T/Time Warner (TWX) deal will be approved. Below is the most recent update from Telecom & Media Policy analyst Paul Glenchur:

It appears the AT&T-Time Warner (T-TWX) merger remains on track toward approval. As we’ve noted previously, the Justice Department’s review represents the sole federal obstacle to government clearance because the FCC has no jurisdiction over this particular deal. On several occasions, as part of his confirmation process, President Trump’s nominee to head the Antitrust Division, Makan Delrahim, emphasized that he will review transactions independently. This reinforces the view that Candidate Trump’s statements against the merger last fall are not likely to influence the Justice Department’s consideration of the deal.

We think the merger should win approval this year although AT&T could agree to merger-related conditions in a consent decree. AT&T’s CEO Randall Stephenson has always suggested a willingness to accept some conditions to facilitate clearance of the transaction.

The completion of the merger could be transformative for AT&T, diversifying the company into content creation while enhancing the combined entity’s digital advertising capabilities. It could also increase pressure on other major broadband distributors, including Verizon, to pursue transactions that further diversify their strategic assets in a rapidly-evolving market for consumer and enterprise services.

WMT

Click here to read our analyst's original report.

Wal-Mart (WMT) stock dropped on Friday with the announcement that Amazon is acquiring Whole Foods. At the same, this week Aldi announced new store growth plans in the US.

The market is concerned about the competitive dynamics within the grocery space for WMT, and probably for good reason, after all grocery is 56% of sales. However at a high level the grocery share call is understood by the consensus, and the M&A and investment cycle is playing out the way we expected. Amazon is expanding investment into B&M, while WMT invests in ecommerce assets. WMT officially announced its acquisition of Bonobos within minutes of the Amazon announcement.

We think this will be a two horse race in the mass market game for some time. Target will lose share, which is good for WMT, and the integration of Whole Foods could present a near term opportunity for WMT for gain share.

MIC

Click here to read our analyst's original report.

Macquarie Infrastructure (MIC) operates a mediocre businesses with a combined pre-tax ROIC of 10%. IMTT has limited growth opportunities and pricing power has faded with new competitive entrants coming online in 2017 likely to pressure both pricing and utilization. The aviation business roll-up model will be challenged to create value given valuations, BEC is a merchant power facility and spark spreads and capacity prices are weak, and Hawaii Gas is likely a dying business with the state increasingly focused on renewables.

Moreover, these disparate businesses are externally managed creating an extra layer of substantial fees. We believe that their target of 10-15% “FCF” growth is highly unlikely and note there is a massive discrepancy between what MIC calls “free cash flow” and MIC’s actual free cash flow. MIC’s self-help tailwinds of the past 5 years are unlikely to be repeated over the next 5. Further, MIC’s businesses are cyclical and are near peak margins.

RLGY

Click here to read our analyst's original report.

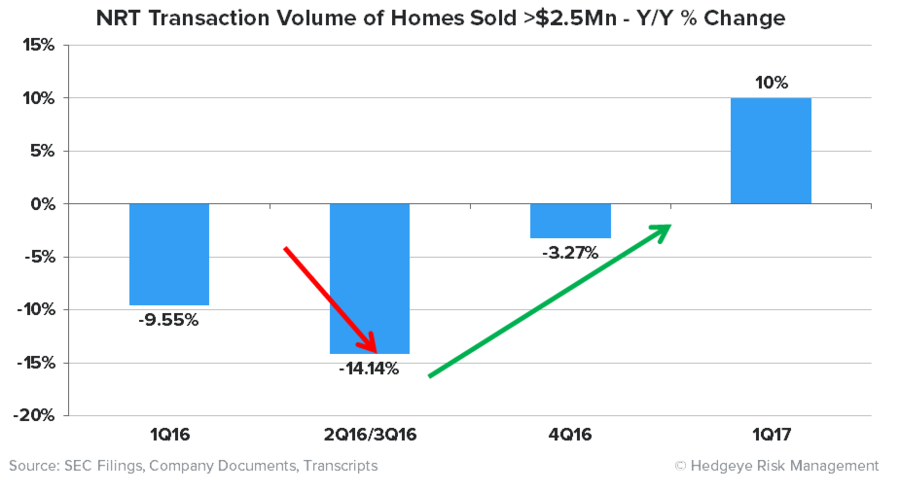

Below is an update on Realogy (RLGY) from the Hedgeye Housing team:

In the first quarter, we saw that sales greater than $2.5mn were up +10% Y/Y in the NRT segment, and sales in this price tier accounted for 20% of NRT's first quarter volume.

In prior weeks, we have noted that the trend in high end real estate volume comports with the broader rebound in luxury spending nationwide. High ticket discretionary consumption (pleasure boats, aircraft, jewelry and watches - our proxy for the state of luxury consumerism) has grown +5.5% thus far in 2017, a notable acceleration off of 2016's post-recession low watermark of 1% growth. We see the recent uptick in luxury discretionary spending as positive for the high end housing market, and Realogy specifically.

DE

Click here to read our analyst's original report.

If Continuing Sales Declines Are Evidence Of A Trough, A Trough It Is: As we understand it, a trough in Deere’s (DE) U.S. & Canada equipment market would require sales to not go down. So, one might think, would “stabilization”. But sales did decline in the U.S. & Canada. DE reported strength in ex-U.S. and Canada markets, mostly South America. Weak crop prices and tougher comps now leave South America as a potential headwind. In the key U.S. & Canada market, crop prices are down year-on-year, and so are equipment sales.

GEL

Click here to to read our analyst's original report.

We continue to like Genesis Energy (GEL) on the short side for its high valuation, super-aggressive non-GAAP accounting, high leverage, and low quality asset base and management team. GEL is a slow-moving train wreck that may be able to hang in through 2018 as GoM crude volumes continue to grind higher, but we think that ultimately the Company will be forced to reduce the distribution and the stock will trade to fair value, which we estimate to be ~$15/unit based on our DCF.

RRGB

Click here to read our analyst's original report.

On Red Robin (RRGB), the key tenants of a LONG thesis are very much in place:

- The development strategy, under Chief Development Officer Les L. Lehner, is now very rational and focused on growing strategically and improving ROIIC.

- Operationally, there is significant low hanging fruit, and Carin Stutz is the right COO to instill the right operational mentality.

- Putting it all together, CFO, Guy Constant, laid out in his presentation the 5-year growth model, which seems very manageable.

In summary, we are seeing the transformation of a company in the early stages of fixing operations with tremendous upside potential!

SNAP

Click here to read the Snap (SNAP) stock report Hedgeye Internet & Media analyst Hesham Shaaban sent Investing Ideas subscribers earlier this week.

CAKE

Click here to read our analyst's original report.

Approximately one month after repeatedly stating that they are seeing absolutely no effects at Cheesecake Factory (CAKE) units, as it relates to slowing mall traffic, CAKE pre-announced a significant same-store sales miss this morning for 2Q17 (-1% vs Consensus Metrix +1.6%). With the stock down ~9% this week, it is clear that many were taking the management team at their word, especially given how they repeatedly pushed back when questioned on the effects of mall traffic on their 1Q17 earnings call.

As we have harped on before, CAKE has seen declining traffic for 17 of the last 18 quarters, and on a two-year stack basis, traffic has been down 13 of the last 14 quarters.

RRR

Click here to read the Red Rocks Resorts (RRR) stock report Gaming, Lodging and Leisure analyst Todd Jordan sent Investing Ideas earlier this week.

KATE

No update on Kate Spade (KATE) for this week’s Investing Ideas but Hedgeye Retail analyst Brian McGough reiterates his long call on the company.

TSLA

Below is a brief note from Hedgeye CEO Keith McCullough explaining why we added Tesla (TSLA) to Investing Ideas:

"Jay Van Sciver is adding Short TSLA to our Best Ideas (Institutional Research) list today, expecting underperformance as Tesla’s exciting concepts transition to mundane execution. Concepts, ideas, and vision can easily win the market’s beauty pageant.

Grinding out a cheap version of a high-end platform in a competitive market, with a less tolerant customer and expiring tax credits? That gets ugly."