OVERVIEW: The annual Home Health Agency payment update is at the White House awaiting approval by the Office of Management and Budget. In the last two annual rules, there were discussions about converting the payment system from one that relies on therapy as a payment factor to one that more fully captures patient characteristics.

We do not anticipate that CMS will propose a shift to a new payment system this year. We do believe that they will use the rule to discuss the work that has been done on developing a new model and, perhaps, signal a timetable. When CMS does propose a change, we anticipate there will be at least two years for implementation.

Regardless of timing, it doesn't hurt to be ready for what CMS may say when they release the CY 2018 Home Health Prospective Payment System update in the next few weeks. We reviewed CY 2014 utilization data for each of the publicly traded home health companies in the context of CMS's policy goals. For those most part, it does not appear that a shift in the payment system, as far as we understand it, will have a negative effect on AMED, LHCG and HLS. KND's contract therapy business may be negatively impacted by the de-emphasis of therapy as a payment factor.

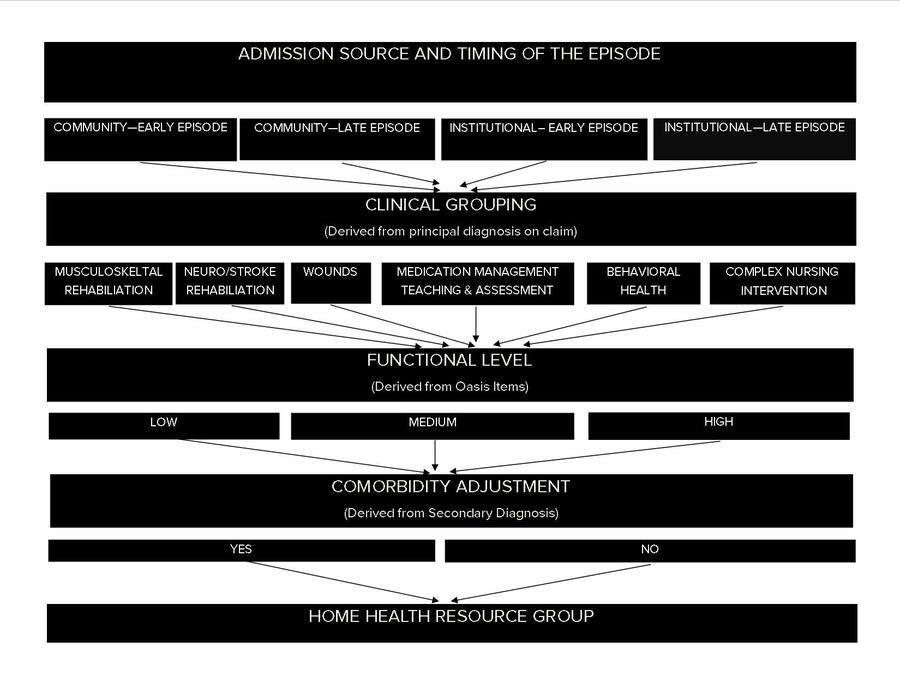

THE NEW PAYMENT MODEL: Dubbed the “Home Health Groupings Model,” the new payment system would reduce the number of patient classifications from 153 to 128 and base them on four major factors:

-

Admission Source and Timing of Episode

-

Clinical Grouping

-

Functional Level

-

Comorbidity

These major factors are further divided into subgroups with the exceptions that Musculoskeletal Rehabilitation and Behavioral Health can only be grouped into a Functional Level of “low” or “high.” The complex nursing intervention group would use clinical diagnoses and OASIS items to group episodes.

Payment groups are assigned a case-mix weight that would determine how the national, standardized 60-day episode rate would be adjusted for each episode of care. The case mix weights are determined by first calculating the predicted resource use for episodes with a particular combination of admission source, episode timing, comorbidity group, clinical group and functional level. The combination specific calculation is then divided by the average resource use of all episodes that CMS’s consultant, Abt Associates, used to estimate the model. The resulting ratio represents the case-mix weight for that particular combination of payment factors.

Another major change to the payment system would be the reduction of an episode from 60 days to 30. Agencies would still only have to complete the OASIS assessment once every 60 days as they do under the current system. The change to a shorter episode would be designed to more accurately reflect the use of HHA resources – which tend to concentrate in the first 30 days. The shorter episode would permit more frequent billing, thus potentially eliminating the need for Requested Anticipated Payments (RAP) many small HHAs use for working capital.

Finally, the proposed model suggests the elimination of payments for non-routine supplies. Instead, the costs associated with providing these supplies would be accounted for as resource use in the HHGM. Under the current system, CMS pays for NRS based on certain clinical factors expressed in the OASIS data set. Agencies receive NRS payments regardless of whether they actually provide the supplies.

The new payment system, would, of course, shift the paradigm dramatically for home health care. The incentives provided by the current federal payment structure encourage the delivery of therapy services. This payment structure implies that services delivered to beneficiaries who will return to full or near full function are priorities. The HHGM payment system would eliminate therapy as a payment factor and instead rely on patient characteristics as described by the 128 groupings.

The concern of Congress, when it asked CMS to review the home health benefit in Section 3131(d) of the Affordable Care Act, was that the benefit did not adequately address the needs of Medicare’s most vulnerable populations. At Congress’s direction, CMS reviewed claims data and cost reports and concluded that home health margins were lower for patients that:

-

Require parenteral nutrition or substantial assistance bathing

-

Have traumatic wounds or ulcers

-

Have poorly controlled conditions including peripheral vascular disease, pulmonary disorders, diabetes, heart disease and severe visual impairment

-

Are dually eligible for Medicare and Medicaid

-

Lack caregiver assistance with ADLs, medication administration and/or procedures or treatments

-

Reside in a low-income community

-

Do not use therapy services during an episode

It is that report and its central conclusion – the home health benefit does not provide adequate incentives to agencies to care for vulnerable populations – that are the foundation of the HHGM payment system.

IMPACTS ON HOME HEALTH PROVIDERS: An Abt Associates report describing the new HHGM includes their assessment of the impact of the payment system change on home health agencies. Using simulated 30-day episodes, Abt calculated a $1,519.22 average episode payment across all agencies under the current payment system and the HHGM, reflecting the anticipated budget neutrality of the change. Abt then estimated payments under the current system and the HHGM system for agencies having different characteristics.

As this select list of agency and utilization characteristics demonstrate, the point of the HHGM payment system is to pay more for patients that require services other than therapy and to address the concerns raised by the ACA Section 3131(d) report.

We have included the agency ownership information in Abt’s report for reference and because the street tends to extrapolate the impact on publicly traded home health providers from this data point. However, Abt relied on the CMS Provider of Services file in which we have found a number of errors in the ownership data. Also, there are 11,000 home health agencies in the U.S. Of this amount, about 85 percent are for-profit and can be as small as two employees or as large as AMED, making us hesitant to draw any conclusions about the role ownership status has relative to the impact of the new HHGM payment system.

Instead, we believe the more helpful analysis is to compare AMED, LHCG, KND and HLS’s utilization patterns to national data. Any proposal from CMS will be budget neutral. In other words, the amount CMS projects to spend under a new payment system will be the same as what they project to spend under the current payment system. So, how much an impact the change will have on any one company will depend on how much their practices differ from national norms.

Using 2014 utilization data and those provider numbers were able to isolate for AMED, LHCG, HLS and KND, we looked at episode distribution and average number of skilled nursing and physical therapy visits. We also looked at the frequency with which each company had an average number of skilled nursing and physical therapy visits of less than one, suggesting a number of episodes that had zero visits.

Because the street tends to forget that the home health industry does not begin and end with the publicly traded companies, we included data on Bayada Home Health, a large privately held provider.

Note: CMS data reflect 2014 utilization. For privacy reasons, when there are less than 10 episodes in a given Home Health Resource Group for any one agency, the data are suppressed. There are data on 4.2 million episodes. Total episodes for which payment was made in 2014 is 6 million.

For the most part, AMED's episode distribution reflects national trends. LHCG has more late episodes and HLS and KND provided more high therapy episodes. With the execption of HLS, average Medicare Standard Payment Amount is consistent with national data.

If the groupings model is adopted, agencies will be paid more for episodes where no therapy is provided. This change should reduce the pressure to ‘push the therapy” to protect margins. The current patterns of utilization would very likely adjust accordingly.

CMS has expressed concern in the past about episodes where no therapy was delivered. With the exception of LHCG, CMS’s concern does not seem to apply to the public home health companies. LHCG's utilization pattern is probably best explained by their emphasis on skilled care and general lack of reliance on therapy visits - something management has mentioned more than once.

Skilled Nursing visits will be rewarded more so than under the new model. AMED, LHCG and KND’s patterns are in-line with or somewhat better than the industry as a whole. HLS appears to be a bit of an outlier in its provision of skilled nursing services, a pattern reflected in their slightly higher average episode payment.

While any change to a Medicare payment system brings with it some risk, the HHGM does not appear to be much of a threat to AMED, LHCG and KND. It appears the HLS is bit of an outlier across the metrics we examined and may need to make more adjustments in their practice than the other companies. If there is one thing we have observed about the home health industry it is that it appears to have an almost unlimited ability to adapt to changing incentives.

The biggest loser, assuming the HHGM model is adopted, would probably be contract therapy providers of which KND is one. The reduction in incentives to provide therapy will lead naturally to the provision of less therapy. That effect will be magnified by a shift in the Skilled Nursing Facility payment system which is currently in the Notice of Proposed Rule Making phase. Like the HHGM, the new SNF payment system will eliminate therapy services as a payment factor for SNF services.

Look for some signals from CMS in the home health payment rule but probably not a formal proposal.

Call with questions.

Emily Evans

Managing Director

Health Policy

@HedgeyeEEvans