The 2010 MGM outlook looks bleak and the valuation rich by historical standards. Does that mean it's a short right here?

We're not so sure. We've written about the likely low CityCenter return on investment and more importantly, the potential for serious cannibalization (see CITYCENTER: A GROWTH OR DONNER PARTY FOR MGM?, 11/23/09). The valuation at 11.5x 2010 EV/EBITDA looks high especially relative to the historical range of 7-11x. Moreover, cost of capital is likely going higher as MGM will be forced into refinancing much of its debt in 2010. We think some form of equity issuance (convertible or straight equity) is likely.

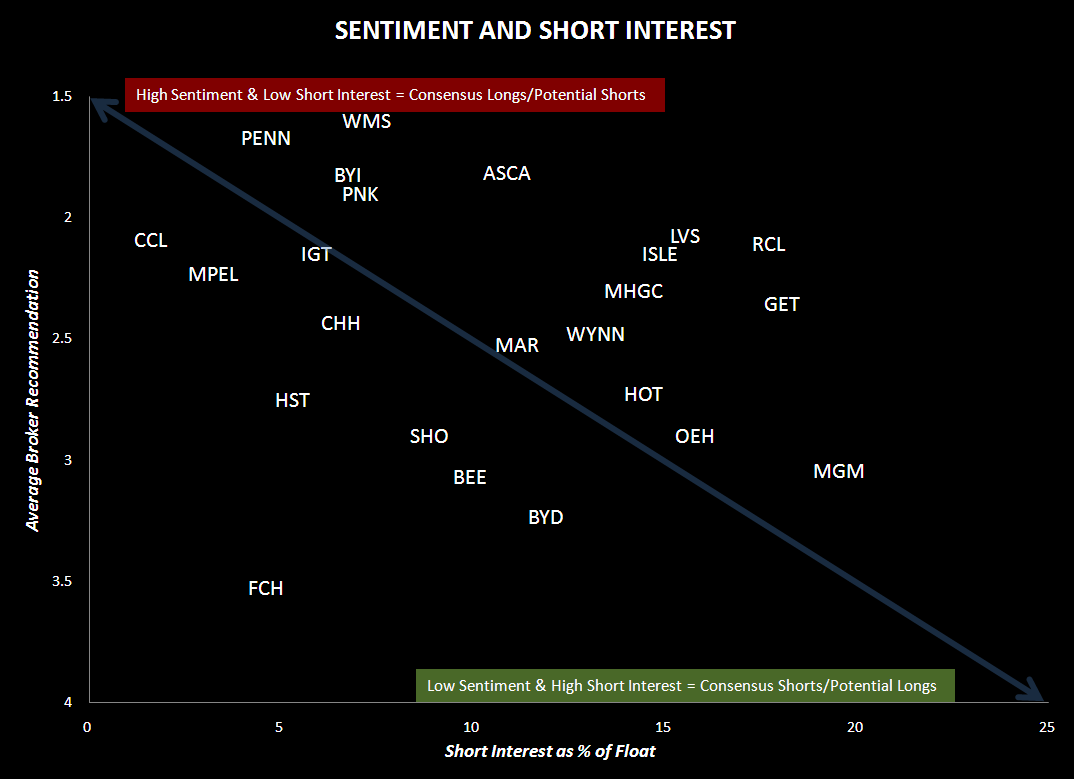

That's a compelling short story, no? The problem is that shorting MGM into the CityCenter opening this week is consensus. Look at the following chart that measures sentiment and short interest among select gaming, lodging, and leisure stocks. MGM sits farthest down the sentiment line, which measures average analyst rating along the vertical axis and overall short interest along the horizontal axis. MGM maintains the highest short interest and one of the lowest average ratings in this universe.

The sentiment surrounding MGM could hardly be worse. Even after a big two day move, the stock is 20% off its recent high in an otherwise strong stock market and the short interest has been climbing. Any encouraging data points surrounding Q1 2010 room rates or indicating a solid opening of CityCenter could spark a short squeeze. Don't forget that MGM has extra incentive to spin the CityCenter opening and market absorption favorably. After all, 2010 will be a year of financing and fundraising.

So far, we don't have any positive data points to report. Indeed, CityCenter is still pricing rooms at a discount to the peer group for January and MGM is offering attractive promotions for the Aria and now Bellagio (see below) for Q1. However, shorter seller beware.