The S&P 500 finished higher by 0.6% on light volume and we saw another outside reversal. All the major indices were higher except for the Russell 2000, which was down 0.4%. The dollar index was basically flat on the day and the VIX was down 1.5%.

On the Macro calendar, Initial jobless claims rose to 474,000, an increase of 17,000 from last week figure of 457,000. The 4-week moving average was 473,750, a decrease of 7,750 from the previous week's revised average of 481,250. This is the lowest level since October 2008.

The good news is that the number for seasonally adjusted insured unemployment during the week ending Nov. 28 was 5,157,000, a decrease of 303,000 from the preceding week's revised level of 5,460,000. While the trend may be friendly, the level of the 4-week average is suggesting continued job losses. This is consistent with the EMPLOYMENT post of 12/08/09 - the numbers reported by the labor department just don’t add up.

For the USA to see a sustainable drop in the unemployment rate, we need Initial jobless claims to drop below 390,000. This week’s Initial claims number shoots back above the 4-wk moving average, and puts everything NASTY (to be confirmed by a NASTY confidence reading on Friday and declining presidential ratings) in play.

The best performing sector yesterday was the Consumer Discretionary, led by the media names. GCI was up +7.0%, followed by SBUX up 4.7% and TWX up 4.2%. GT and IPG rounded out the top five performing stocks.

Financials (XLF) and Materials (XLB) were the two worst performing sectors. Dragging down the Financials were MBI, MI and ZION. Also underperforming were WFC (2.4%) and BAC (1.2%) on the back of increased expectations for TARP driven capital raises. Bucking the downward trend in the XLFs were TROW +3.0% and AMG +2.5%.

Healthcare also outperformed led higher by HMOs, which were up for a fifth straight day, in reaction to news concerning the public option. A Research Edge favorite, UNH, was up +6.4%.

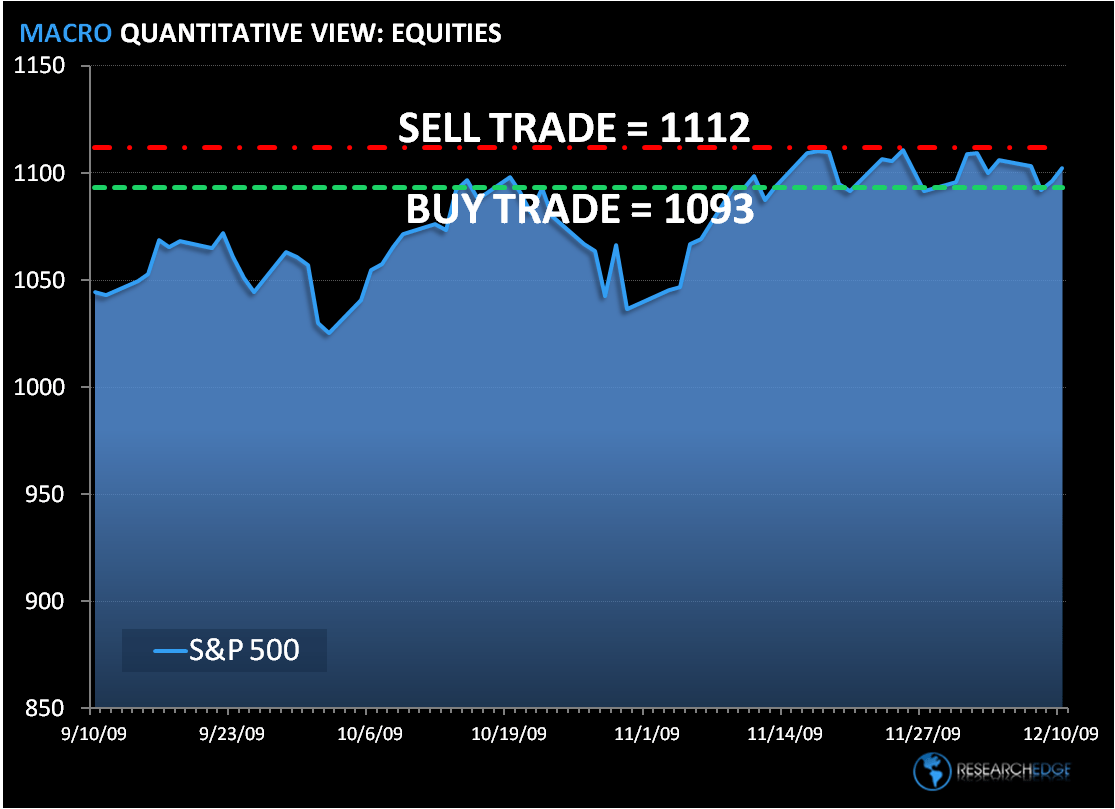

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 19 points or 1.0% upside and 1.0% downside. At the time of writing the major market futures are trading slightly higher.

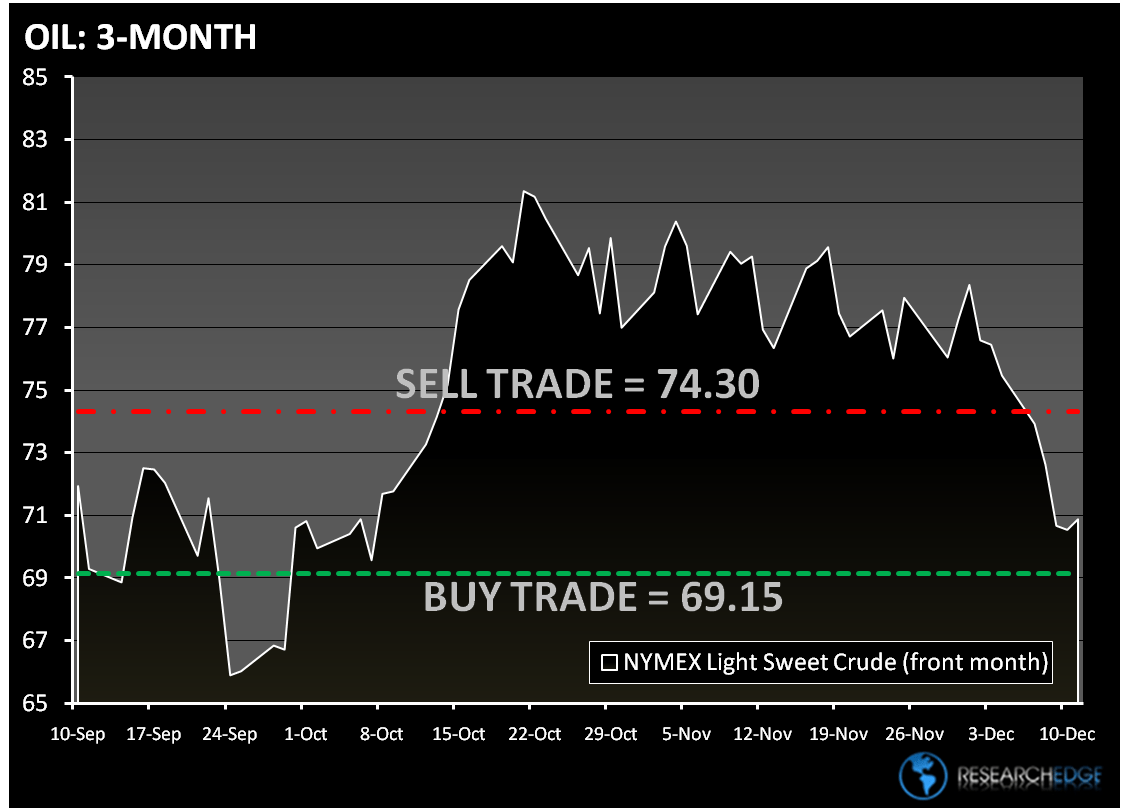

In early trading today, crude oil is higher for the first time in eight days after China’s refineries processed a record amount of crude last month. The Research Edge Quant models have the following levels for OIL – buy Trade (69.15) and Sell Trade (74.30).

In London Gold is higher on the day and looking like it will be down two weeks in a row. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,102) and Sell Trade (1,167).

Copper is higher for the first time in seven days as China’s industrial production grew more than forecast. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.10) and Sell Trade (3.26).

Howard Penney

Managing Director