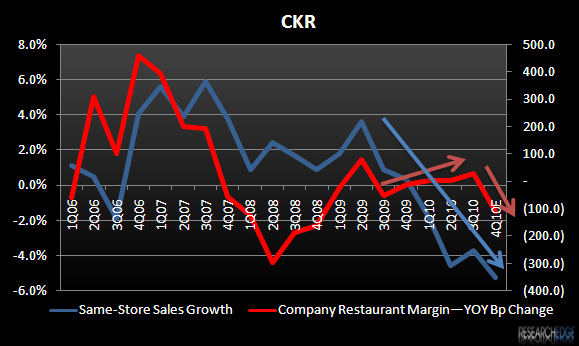

Being that CKR had already preannounced its fiscal 3Q10 sales and restaurant level margins last month, the most important news that came of the company’s earnings call was its full-year sales and restaurant level margin guidance. Management guided to -3.5% to -4% blended same-store sales and a 20-40 bp decline in full-year margins. Based on the sequentially decelerating top-line trends year-to-date, this sales guidance is not surprising. The full-year margin guidance, however, implies about a 110-200 bp decline in the fourth quarter and breaks the company’s year-to-date trend of maintaining YOY margins despite top-line weakness. We knew it was only a matter of time!

As I have said before, margins could not continue to move higher with comparable sales trends getting increasingly worse. And, period 11 comparable sales (also reported yesterday) did just that. Carl’s Jr. same-store sales decreased 8.1%, implying a 50 bp sequential decline in 2-year average trends from period 10. Although Hardee’s same-store sales improved slightly on a 2-year average basis, it was not enough to offset the free fall at Carl’s Jr. and blended 2-year average trends declined 30 bps on a sequential basis. The low end of the company’s full-year blended same-store sales guidance assumes that 2-year average trends deteriorate more than 50 bps in the balance of the quarter from period 11 levels.

Favorable commodity costs have helped to support restaurant level margins despite the significant demand headwinds with food and packaging costs as a percentage of sales declining 60 bps YOY in Q1, 140 bps in Q2 and 180 bps in Q3. The company is still expecting some commodity favorability in Q4, though to lesser magnitude than in Q3, as CKR management pointed out (as did I last month) that food prices have bottomed and are moving higher. Even with this continued favorability, margins should decline 110-200 bps YOY in the fourth quarter. What is going to happen to CKR’s “industry leading” margins once food inflation returns?

CKR outlined some of its new sales building initiatives on its earnings call, which are included in the slide below, and I am not convinced that any of them will be the game changer the company needs to stem the declines at Carl’s Jr. As far as I can tell, the only new idea on the list is the company’s strategic decision to focus more attention and advertising on its healthier options, including salads at Carl’s Jr. Although salads are not new to the concept, the company has not advertised or upgraded them in the recent past because they did not appeal to its targeted “young, hungry guys.” Management believes that this demographic is more health conscious now and that with digital media that it can more effectively market its newly upgraded salads to women without alienating its primary audience.

First, I don’t think salads will prove to be a real traffic driver for Carl’s Jr’s “young, hungry guys”. Second, and more importantly, salads typically carry lower margins and decrease add-on sales such as French fries. Management stated that the lower incidence of sales of side items and combos meals is already largely to blame for the current comparable sales trends and though this problem is not unique to Carl’s Jr., salads will not help on this front.