MCD’s November same-store sales growth came in below street expectations across the board, which signals to me that the street continues to be too bullish. Relative to the ranges I outlined in my sales preview note last week, reported comparable sales trends in the U.S. and APMEA came in NEUTRAL with Europe posting a BAD number.

In Europe, comparable sales increased 2.5% in November. Relative to both the street and my expectations, Europe posted the biggest shortfall. Even adjusting for the calendar shift, 2-year average trends decelerated rather significantly on a sequential basis from October. MCD attributed the slowdown to continued weakness in Germany and more broadly, to the sluggish economy. Management has routinely stated that its business is not recession proof but recession resistant, and these reported November results, particularly in Europe, should convince investors that there is truth to that statement.

In the U.S., same-store sales declined 0.6%. Adjusting for the calendar shift, which hurt reported results in November but helped in October, same-store sales trends in November were about even with October on a 2-year average basis. Although I outlined this outcome as NEUTRAL relative to my expectations, these top-line trends which have declined from prior months are not good. MCD has now posted two consecutive months of comparable sales declines after having not reported a negative result since March 2008. And, MCD has not reported consecutive monthly declines since early 2003.

On its 3Q09 earnings call, MCD management stated that despite its expectation of flat to negative comps in October that it was still gaining market share. MCD’s continued softness in the U.S. points to share losses or a narrowing of the gap between MCD and its peers at the very least. As the first chart below shows, MCD has outperformed both Wendy’s and BKC since 3Q08. I would not be surprised to learn that BKC’s $1 double cheeseburger, which was launched nationally on October 19, is gaining share. BKC has underperformed its two biggest competitors in the most recent quarters, but I think the company will show signs of comparables sales recovery when it reports fiscal 2Q10 results.

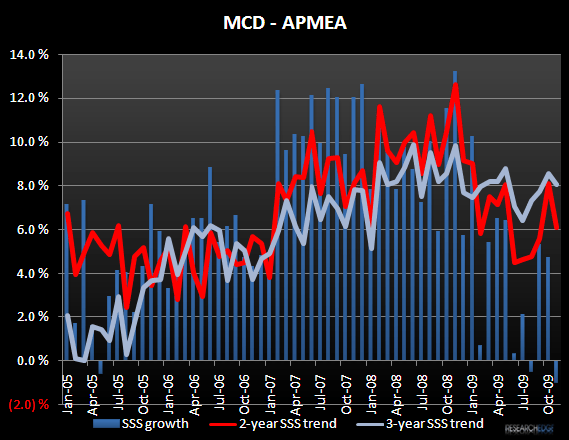

In APMEA, same-store sales decline 1%. The company was lapping an extremely difficult +13.2% result from last year so although 2-year average trends slowed sequentially from October, MCD is still putting up strong numbers in this segment. Like YUM, MCD continues to experience weakened demand in China.