On Monday there was no follow thru from the big move in the dollar on Friday. Yesterday, the dollar index was down 0.2% to close at 75.76. If the dollar index closes up today it will have been up three of the last five days. Yesterday I started to make the case that if the dollar were a “stock” as an equity analyst I can make the case that the “fundamentals” are bullish. Taken together - the labor market, the rising savings rate, the trade picture, corporate profitability and the Fed’s free money policy – do not support a weak dollar.

Yesterday, the S&P 500 declined 0.2% and made a second outside reversal in as many days. While there was not any BIG theme to drive yesterday’s performance, the S&P continues to show signs of breaking down. Yesterday, comments from Fed Chairman Bernanke that the US economy faces "formidable headwinds" was a non event for the market. The MACRO calendar is quiet today except for the ABC consumer confidence number due out after the market close today.

Despite the Fed’s cautious comments, parts of the RECOVERY trade were alive and well yesterday. The three best performing sectors were Utilities (XLU), Consumer Discretionary (XLY) and Materials (XLB). Rising 6.8%, the XLU has been the best performing sector over the past week. The XLY was the second best performing sector yesterday and for the past week, benefiting from the better labor markets. Driving the XLB higher was OI (4.1%), DOW (2.0%) and BLL (1.8%).

Driving the S&P lower was the Financials (XLF). Within the XLF the REITs and regional banks were the biggest drag on performance; names such as KEY (4.4%), BBT (2.8%) and PNC (2.7%) were among the worst performers. While there did not seem to be any specific news, it should be noted that the FDIC announced six more bank failures on Friday, bringing the year-to-date total to 130 from 25 in 2008 and 3 in 2007.

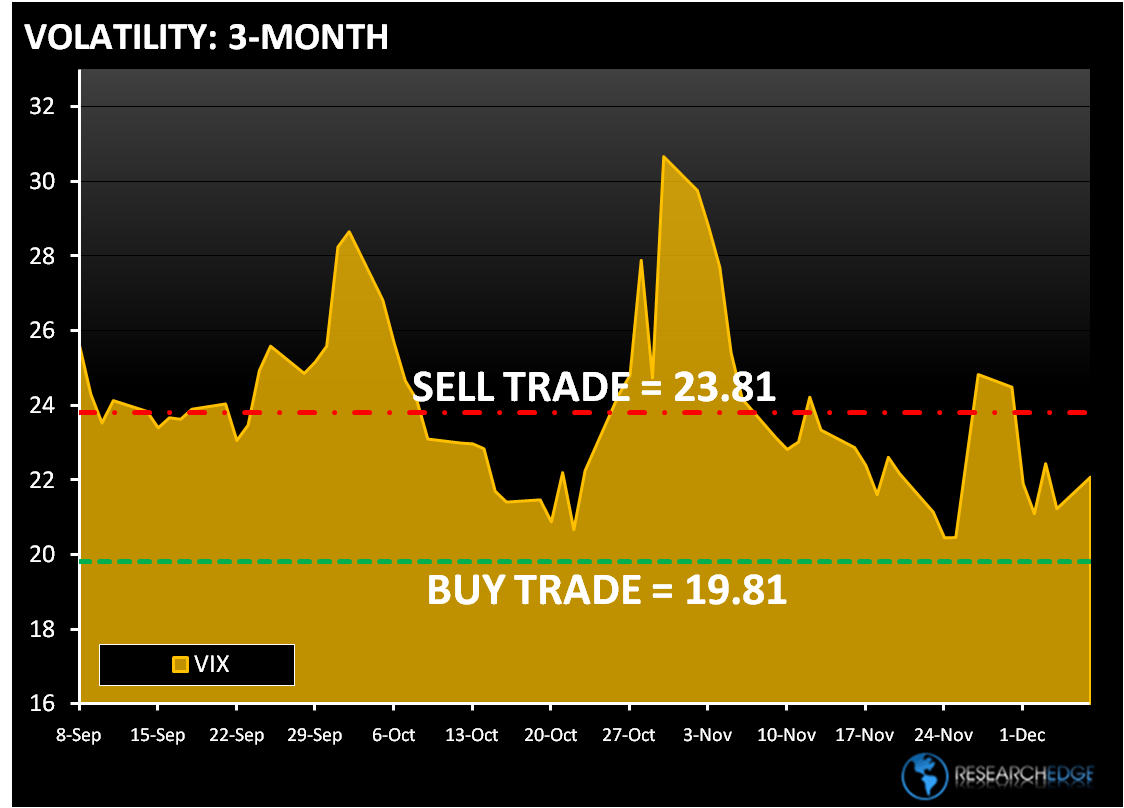

Helping to put some incremental pressure on the S&P 500 was the 4% move in the VIX. In total seven of the nine sectors outperformed the S&P 500, but only three showed positive performance on the day. The two sectors that did not outperform were the Industrials (XLI) and the Financials (XLF). Energy (XLE), the other sector broken on TREND, was down 0.2% in line with the S&P 500.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 35 points or 1.5% upside and 1.5% downside. At the time of writing the major market futures are trading slightly lower.

Crude oil is trading lower as the dollar is stronger in early trading today. The Research Edge Quant models have the following levels for OIL – buy Trade (74.30) and Sell Trade (78.11).

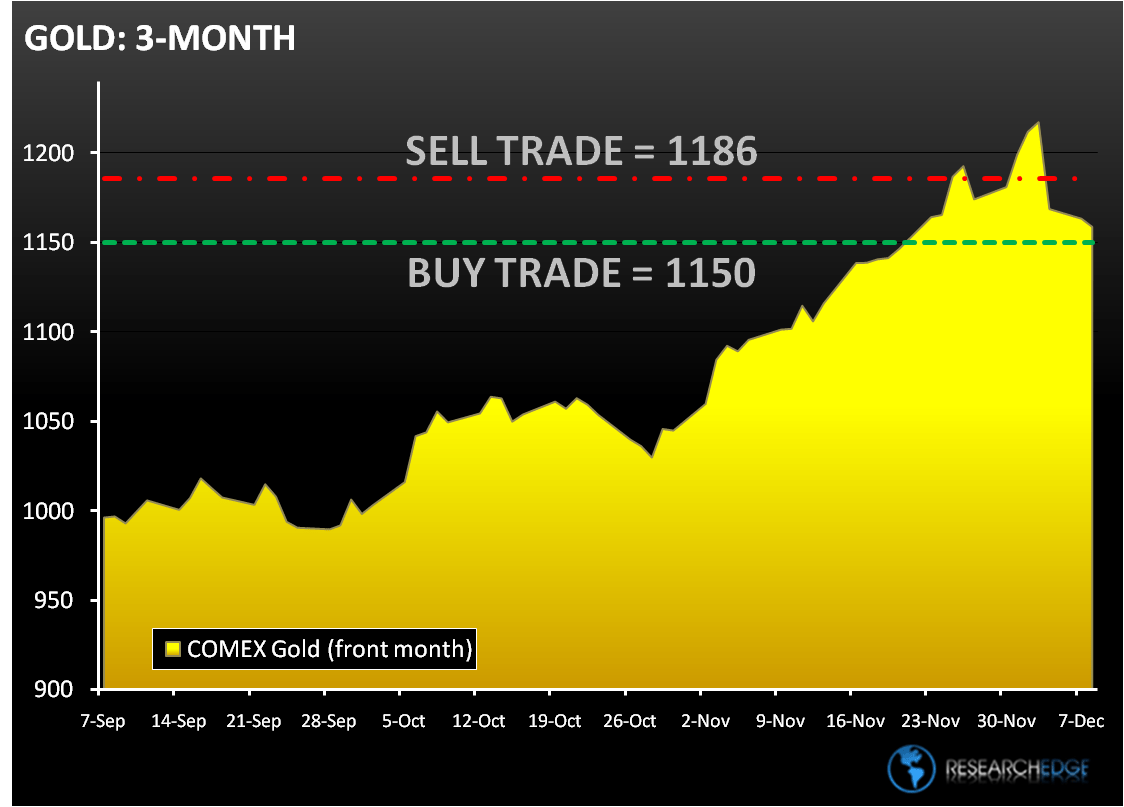

Gold is basically trading unchanged on the day, but the trends are still bullish. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,150) and Sell Trade (1,186).

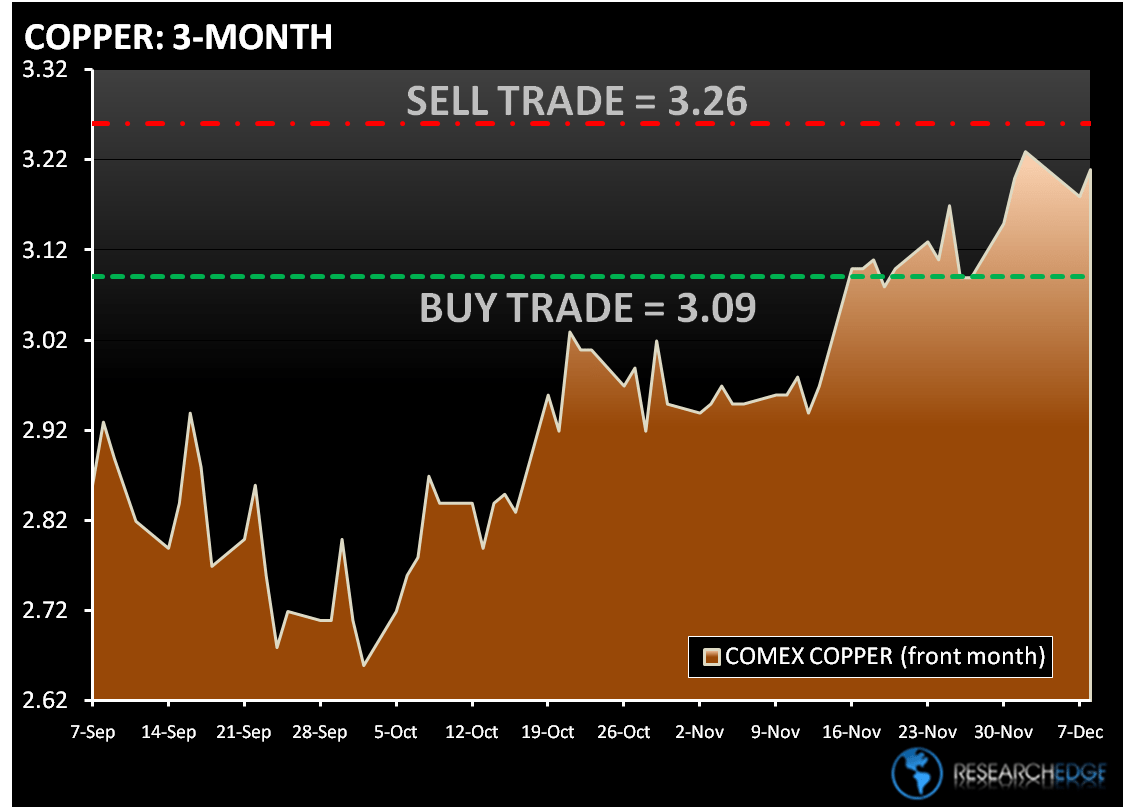

Copper is higher for the first time in four days on the back of the Fed’s comments. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.09) and Sell Trade (3.26).

Howard Penney

Managing Director