As we head into the key holiday selling season in the absence of real broad-based consumer-driven demand, it’s important to note the product trends that are helping to drive relative outperformance. One such trend has been women’s fashion boots as highlighted in our 11/09 post “The Boot Heat Map.” The other (though arguably less publicized) trend has been in what has been dubbed the “wellness/toning” category, comprised of product’s including SKX’s Shape-Ups and Reebok’s Easy Tones. With retailers beginning to recognize the contribution of wellness product in 3Q, it will play in increasingly more important role in 4Q performance and beyond for retailers and SKX alike.

Strong demand for wellness shoes was one of the keys to our view ahead of SKX’s 3Q results. Since then, the Street has increased FY10 estimates by 50% to $1.50. While we remain meaningfully above current expectations by nearly 25% at $1.85, we are mindful that the gap has narrowed considerably over the last month as expectations have clearly risen. So the question remains – is the Shape-Ups trend more Crocs-like, or Ugg-like in duration?

I’m leaning towards the latter given the view that “function” is less fickle than fashion. While SKX is busy at work trying to introduce some level of creativity into the category in the form of different uppers (boots, sandals, leather, shearling, etc..) for next year, the wellness benefits are not to be overlooked. Whether you buy into the true technical benefits of the curved sole which is said to promote better posture, toned legs, and ease joint pressure the reality is that the perceived benefits are driving demand and product awareness. The category is expected to see a substantial influx of marketing dollars being spent on the category across all brands and SKX is well positioned with its current market leading position. Other brands in the category include the original MBT and Reebok.

In an effort to size the opportunity for wellness I incorporated DSW’s recent commentary that this category could represent 2%-3% of total revenues. Assuming that same share of revenue for other footwear retailers like SCVL and BWS (Famous Footwear) and then 1%-2% for others including DKS, TSA, HIBB, FINL, and FL one can derive a $135-$215mm opportunity. Add to that the sell-through at department stores like Macy’s and Nordstrom’s (SKX is back at JWN for the first time in three years) and you can add an additional 50% in revenues getting arriving at a market size of ~$200-$300mm domestically. Note, that doesn’t include smaller chains and independent retailers. Given tests thus far, simply doubling the domestic opportunity to account for international market potential is likely to prove conservative. Taking this approach, we get to an estimated ~$400-$600mm global opportunity for wellness shoes. Given Shape-Ups dominant position in the category, it is evident that not only is this trend at its early stages, but also that it also has legs.

For better perspective on the wellness category, we took at look at the commentary of several footwear retailers from Q3. Like boots, wellness/toning is one of the few product trends that is being called out and is still likely to drive upside in 4Q:

DSW: The position we've taken is we started with our key partner, Sketchers, and everybody has the Shape-ups program and we tested that late in Q2, early in Q3 and saw some very very promising results and positioned ourselves to be in a very strong position for 4Q going into 1Q so that is where we've taken the majority stake in the toning product. We are, however, testing product from other athletic resources in a good, better, best, price point so we'll test everything from a 39 all the way up to $79 price point in addition to the $100 Sketchers shape-up that's out there right now. Some of the early results from these test items have proved very promising…even having said that, I think you're really looking at two, maybe 3% of your total business, the total DSW business being in this toning product.

BWS: We anticipate consumer purchasing patterning will be similar to those that we saw in the third quarter…as such, we ramped up our 4Q receipts of key categories and brands, most notably boots and wellness product, which we think will be the key drivers through holiday and into spring lead by Sketcher Shapeups and Reeboks Easy Tone.

SCVL: We anticipate continued strength in the athletic category and are enthusiastic about the opportunity to have two new significant product lines in the wellness category with Skechers Shape-Ups and Reebok Easy Tone Shoes…to take full advantage of this hot selling category we have taken a strong inventory position in Wellness. Therefore, inventories are up 2.4% on a per door basis with boots and Wellness accounting for all of this increase. With the expected continued strength in boots and Wellness footwear, we currently expect our comparable store sales in Q4 to increase in the range of 3 to 5%.

We had a few stores with Wellness product in August. Actually we delivered that product early in the second quarter, and then as we saw the product selling through early in the second quarter and in August, we bought for additional stores for September. Then we bought for more stores in October and as we move through fourth quarter all stores actually within the next one week, all stores would have. So the inventory built during the quarter and as the inventory built product reap the benefits of the sale.

We have no way of telling whether or not we are bringing in a new customer. We do know, we have a unique concept. As we get product in and refill of this product has been selling out and we've been filling it back in…so we actually believe that our customers are stepping up for this product, and they've been looking for it.

We saw the trend early, and we tested those shoes in about 25 stores in early spring as soon as we can get them. And when we saw the sell through, very aggressively went after it and as the sell through continues, the more stores we put them in, we got even more aggressive. So I'm feeling very confident that we are well covered in Wellness as we go through spring.

HIBB: We actually have the toning…and we'll see that grow into our next year as well and build upon it. As long as we see good marketing around, supporting the programs now, we'll be able to support it from our end as well.

GCO: We are not involved in the wellness business. We know it's very important for a lot of footwear guys. We don't think it hits our customer. We're really much more of a fashion retailer…It's an older demographic so we've chosen thus far not the play.

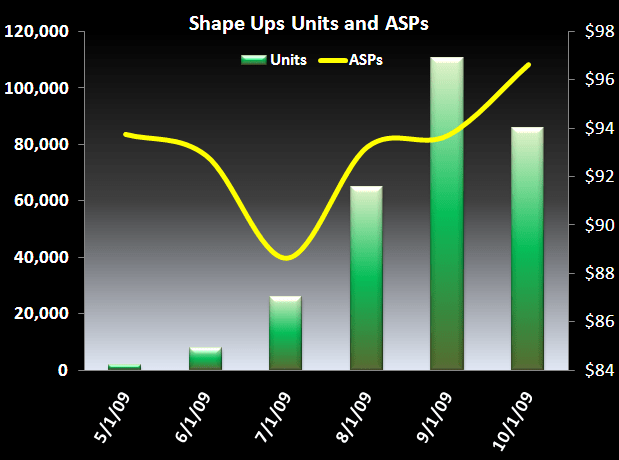

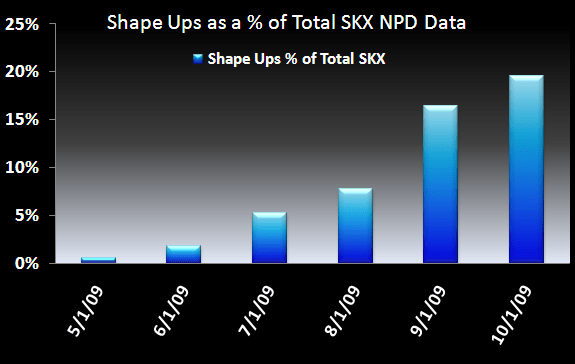

After meeting with COO/CFO David Weinberg last week at FFANY, we came away from the meeting with a few key takeaways: business is currently strong, Shape-Ups is still in its infancy, and that the opportunities to exceed earnings estimates in the near-term appear to be high. This sentiment is illustrated (and supported) in the follow charts. Note that while unit volume at retail declined in October according to NPD data, Shape-Ups as a % of SKX revenues continues to grow reflecting typical seasonality (see Figure 1).

Casey Flavin

Director

Figure 1:

Figure 2: