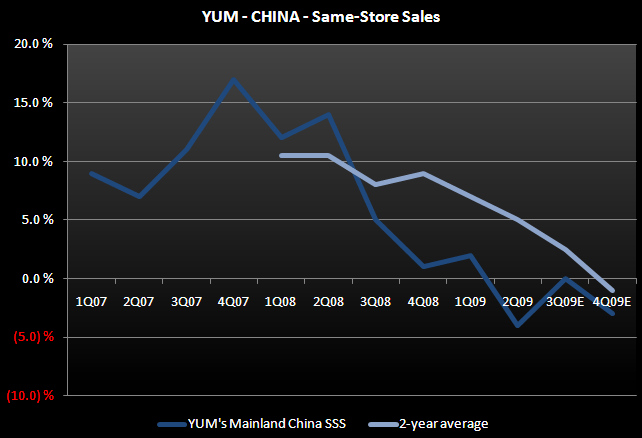

There is still no rational explanation for the decline in sales trends in YUM’s China business.

Given the sequential deceleration in same-store sales trends in China there are many unanswered questions as to WHY.

(1) The trends suggest that there are bigger issues with the Chinese consumer or there may be issues with the concept.

(2) YUM’s aggressive posture toward unit growth might be generating self inflicted issues that are complicating the country’s economic issues.

With all three of YUM’s key business units now seeing declining same-store sales, 2010 will be a challenging year for the company. The US business is in a free fall with same-store sales down 8% in 4Q09. The issues in the US are obvious and will be very difficult to correct without a major investment by the company. Given that management guided to 5% operating profit growth in the US in 2010, it must be relying on increased cost cutting to drive that growth so there does not seem to be much room for significant investment in the business.

YRI’s comparable sales turned negative in 4Q09 as well, down 1%. YRI is primarily franchised, but the top line still matters, just to a lesser degree.

This brings us to China and the question about why business is declining so rapidly. YUM’s future is extremely dependent on China and continued growth in the country. As the story goes, China has billions of consumers and can support tens of thousands of units. Unfortunately, less than a ¼ of them can actually afford to go to the concept.

To be clear – there continues to be unit growth opportunities for YUM in China. The fact remains, however, that the company is growing too fast in that market. Supporting the company’s claim that the slowdown in sales trends in China is attributable to the Chinese economy is the fact that McDonald’s is not doing well either. In response to the changing tone of business in China, McDonald’s has slowed unit growth.

I have been making the claim that YUM should slow its growth in China for the better part of a year and from where I sit, it’s more imperative now. It does not matter if the decline in demand stems from YUM-specific issues or from economic pressures on the Chinese consumer. Either way, declining sales suggest that the economic model is changing and so are returns.

Senior management does not agree with my assessment of the growth related issues in China, and has said that I am too US-centric in my analysis. I might just be a typical US restaurant analyst and I might not fully understand the China story. That being said, I do understand the math behind declining same store sales!