Taken together - the labor market, the trade picture, corporate profitability and the Fed's free money policy – do not support a weak dollar. Importantly, the two sectors that have benefitted the most from a weak dollar are signaling that changes are coming. The Energy (XLE) in BROKEN on TRADE and the Financials XLF is BROKEN on TRADE and TREND.

On Friday, the S&P 500 finished higher by 0.6% and closed up 1.3% on the week. The S&P 500 made a lower-high on an outside reversal; TRADE and TREND are bullish. On Friday the MACRO calendar was more supportive to the RECOVERY trade.

Friday started off with a bang as the market rallied sharply following a significantly better-than-expected November employment report, with some much needed support for the RECOVERY trade. Nonfarm payrolls fell 11,000 in November, compared with expectations for a 125K decline. Last month's decline was the smallest since December of 2007. In addition, there were significant upward revisions to the prior two months, while temporary employment, rose 52,000 in November. The unemployment rate fell to 10% from 10.2% in October as household employment rose by 227K and the labor force declined by 98K.

While the S&P pushed to another new high for the year, the market could not ignore the sharp bounce in the dollar and the reality that the Fed may have to start unwinding its free money policy sooner than expected. On Friday the dollar index (DXY) closed up 1.7% to 75.91. As a result commodities and commodity stocks were hit the hardest by the move in the dollar.

The Materials (XLB) and Energy (XLE) were the two worst performing sectors on Friday. Within the XLB, precious metals stocks were among the worst performers - DD (7.2%), FCX (4.7%) and NEM (4.3%) were the notable decliners.

The three best performing sectors were Financials (XLF), Industrials (XLI) and Consumer Discretionary (XLY). The XLF was the best performer sector after being the worst on Thursday. The three best performing stocks were MCO +7.7%, PFG +7.0% and KIM +6.5%. The improvement in the labor market was supportive of a move in the Professional Services (MWW +15% and RHI +11%) and Airlines (which helped the XLI outperform) and other select consumer discretionary names.

Semiconductor stocks finished higher for a fifth straight session Friday with the SOX +2.1%. The latest round of gains was fueled by the strong Q3 earnings and Q4 guidance out of MRVL, which was up +9.3% on the day.

Volatility got crushed last week, with the VIX down 5.4% on Friday and 14.1% for the week.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 35 points or 1% upside and 1.5% downside. At the time of writing the major market futures are trading slightly lower.

Crude oil is dropping for a fourth day in a row (trading below $75 a barrel) as the dollar is stronger on speculation the Fed will raise rates. The Research Edge Quant models have the following levels for OIL – buy Trade (74.25) and Sell Trade (78.52).

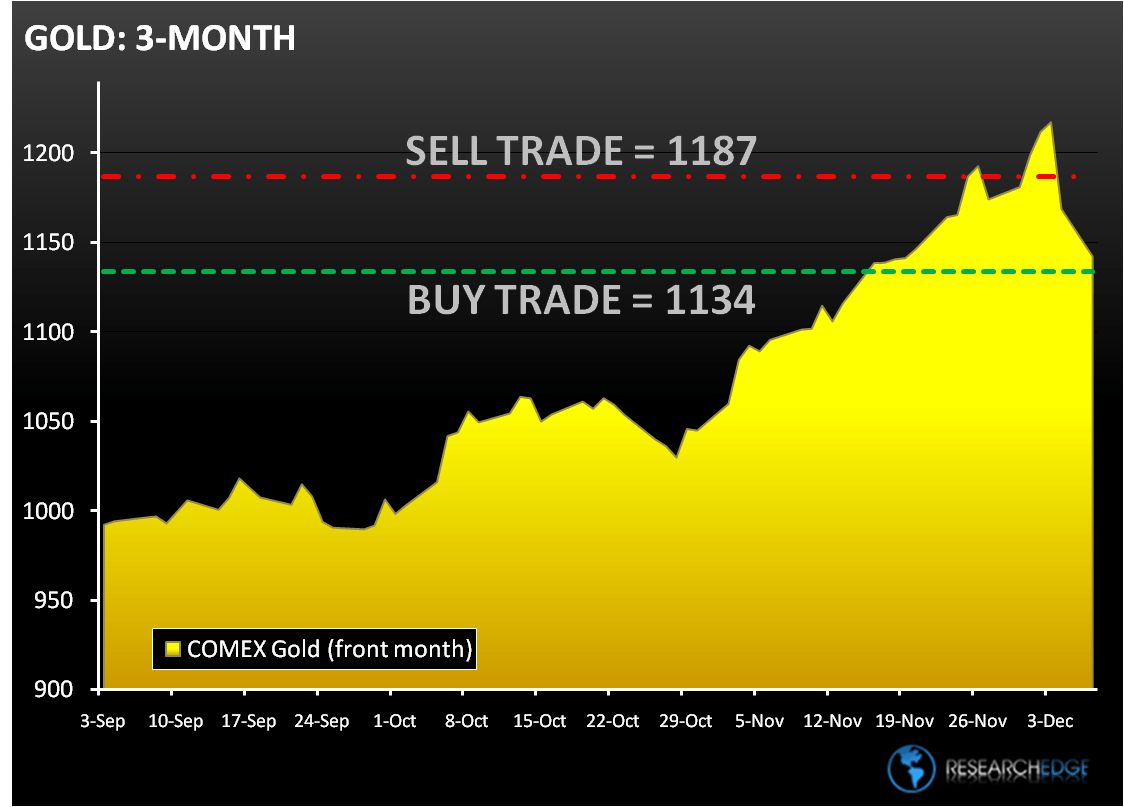

Gold fell for a third day in Asia after the dollar’s rally hurt gold on Friday. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,134) and Sell Trade (1,187).

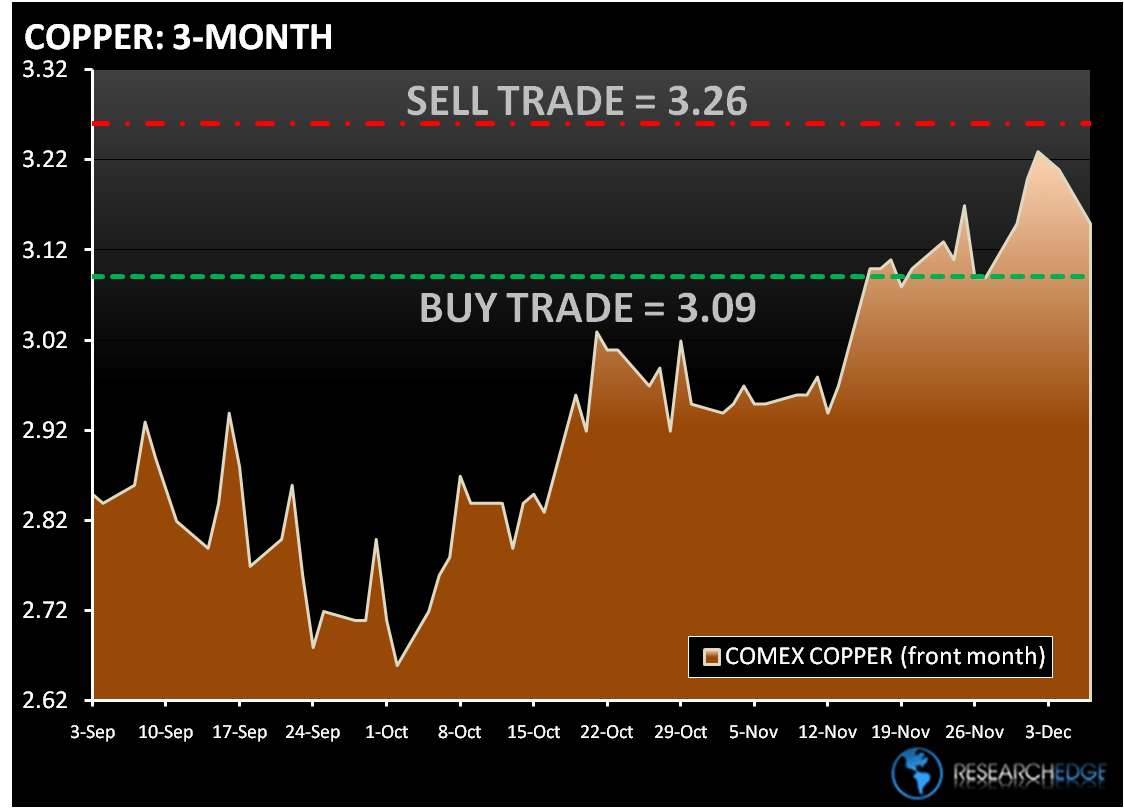

Copper is lower for the third day in a row as the dollar is stronger. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.09) and Sell Trade (3.26).

Howard Penney

Managing Director