Yesterday, the S&P 500 finished lower by 0.8% in a day of quiet trading, although a late-day selloff left the S&P 500 at the worst levels of the day! For the most part the MACRO calendar was unkind to the RECOVERY trade.

On the MACRO calendar, Initial claims fell 5,000 to 457,000 for the in the week-ended November 28th. Importantly, the four-week moving average dropped to 481,000 from 496,000; the 13th consecutive weekly decline. Continuing claims rose 28,000 to 5.46M, the first increase since August. All eyes are on today’s employment report. The consensus is for nonfarm payrolls to fall 125,000 and the unemployment rate is expected to remain unchanged at 10.2%.

Also, disappointing was the ISM non-manufacturing index which fell to 48.5 in November from 50.6 in October. Consensus expectations were for an increase to 51.5. Lastly, November same-store sales were weaker than expected.

Once again, the Financials (XLF) was the worst performing sector, declining 2% on the day. Credit card and Banks were notable underperformers, as the BKX declined 3%.

The three best performing sectors were Utilities (XLU), Technology (XLK) and Industrials (XLI). The XLU has now outperformed the S&P 500 by 3.7% over the past week. The XLK outperformed on a relative basis closing flat on the day. The outperformance of the XLK was due to the semis, which rallied for a fourth straight day with the SOX up 1.2%.

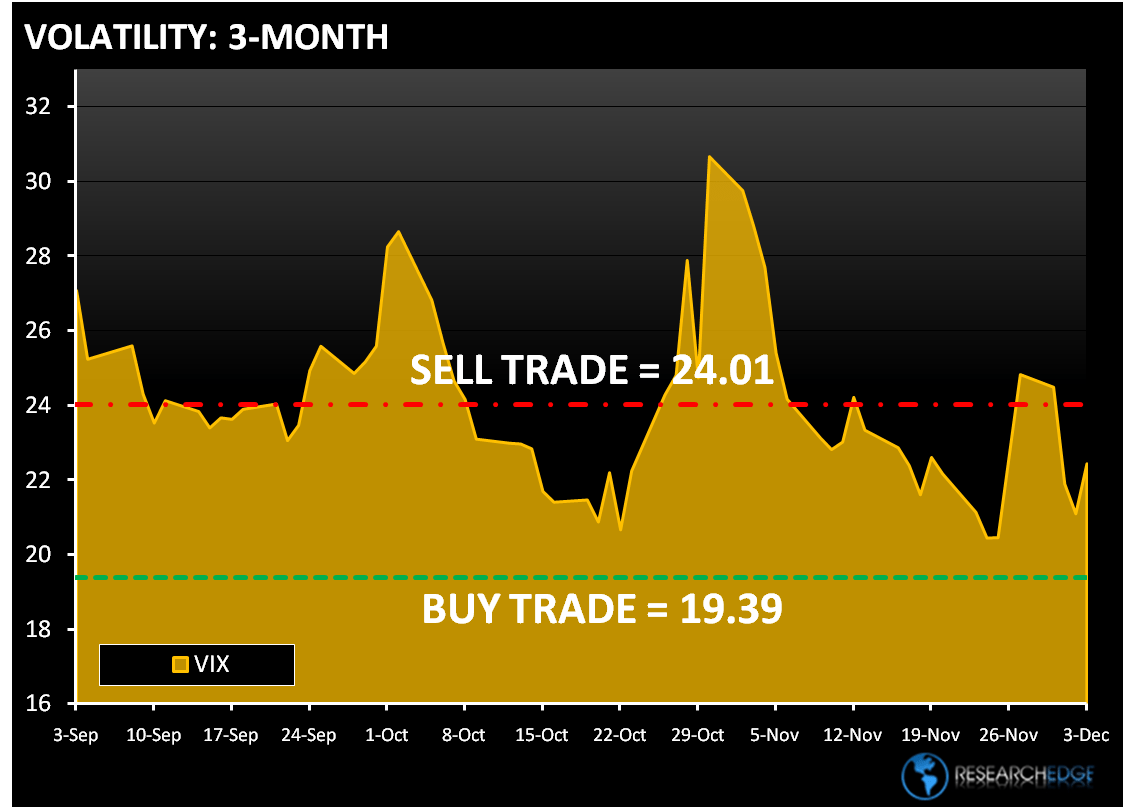

The appetite for risk is waning as the VIX was up 6.3% yesterday and 9.7% over the past week. The Dollar index was up slightly on the day.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 35 points or 1% upside and 1.5% downside. At the time of writing the major market futures are trading slightly lower.

Crude oil fell for a third day before a report forecast to show unemployment remained unchanged at a 26-year high in the U.S. The Research Edge Quant models have the following levels for OIL – buy Trade (74.18) and Sell Trade (78.37).

Gold fell for the first time this week as the dollar index is stronger in early trading today. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,186) and Sell Trade (1,224).

Copper is lower in early trading today, as inventories rose and most commodities are lower ahead of the U.S. jobs report. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.18) and Sell Trade (3.26).

Howard Penney

Managing Director