Yesterday, the S&P 500 was essentially flat on the day but six of the nine sectors declined. For the second day in a row the Utilities (XLU) was one of the best performing sectors. Also, for the second day in a row there was no overriding theme that dominated trading.

Ahead of the November sales data the Consumer discretionary (XLY) was the third best performing sector, improving 0.3%. The gains were driven by SNA (3.4%), MDP (3.3%), RL (3.0%) and WHR (2.8%). GME was the worst performing stock trading down 8.3%. Deflation still rules with WMT cutting prices by 20% on the top 25 video games.

Yesterday’s MACRO calendar included some mixed employment data. The ADP private employment fell 169,000 in November, weaker than consensus expectations for a 150,000 decline. The absolute decline is the smallest drop since July of 2008 and the eighth consecutive monthly deceleration in job cuts.

While Materials (XLB) kept the RECOVERY trade alive yesterday, the Energy (XLE) sector was the worst performing sector on the day. Weakness in OIL following bearish inventory data and geopolitical concerns surrounding Iran seemed to be the biggest drag on the group. January crude settled down 2.3% at $76.60 a barrel. The government said crude stockpiles rose by 2.09M barrels in the week-ended November 27th, compared with consensus for a 400,000 barrel decline.

I can’t help but to think that the underperformance of the Financials are not foreshadowing some more MACRO drama on the horizon. Yesterday, the Financials (XLF) underperformed the broader market. The high quality financial institutions were among the laggards for the second day in a row.

Despite yesterdays mixed performance, the appetite for risk accelerated with the VIX down another 3.6%.

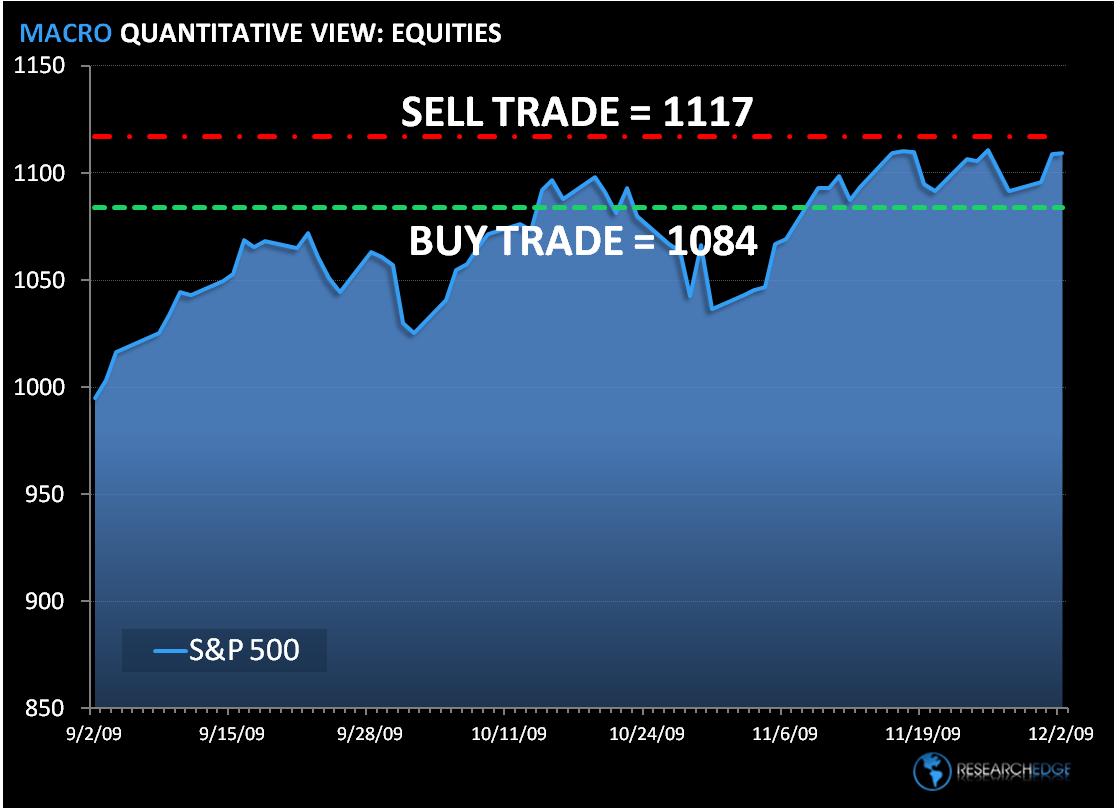

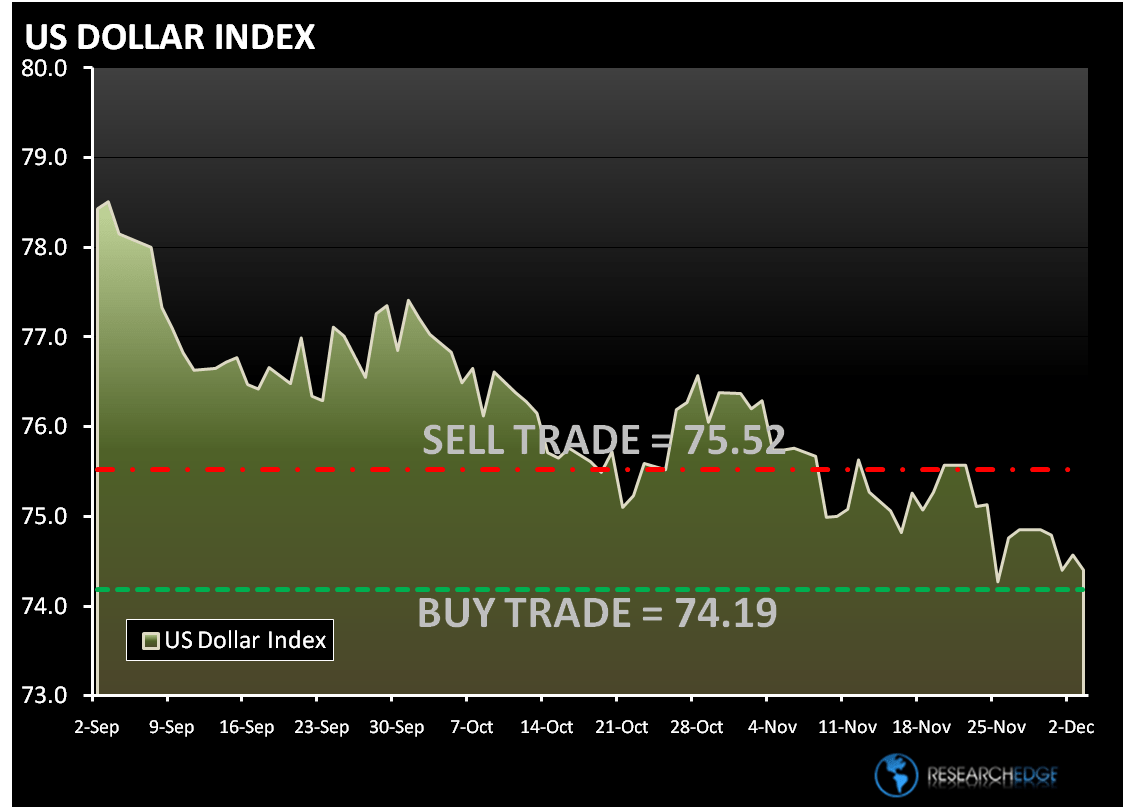

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 33 points or 1% upside and 2% downside. At the time of writing the major market futures are trading higher.

In early trading today, crude oil rose above $77 a barrel as the dollar weakened. Oil rebounded after losing 2.3% yesterday as the U.S. Energy Department reported that stockpiles swelled to the highest level since August. The Research Edge Quant models have the following levels for OIL – buy Trade (75.61) and Sell Trade (78.88).

China’s central bank views gold prices as very high and will be wary of “bubble” assets, according to the Apple Daily. The story citied Hu Xiaolian, a deputy governor at the People’s Bank of Chin! Regardless, gold rose to a record $1,218.25 an ounce in the morning “fixing” in London. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,176) and Sell Trade (1,224).

Copper futures in Shanghai advanced for a fourth day to the highest level in 15 months on global economic optimism. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.17) and Sell Trade (3.25).

Howard Penney

Managing Director