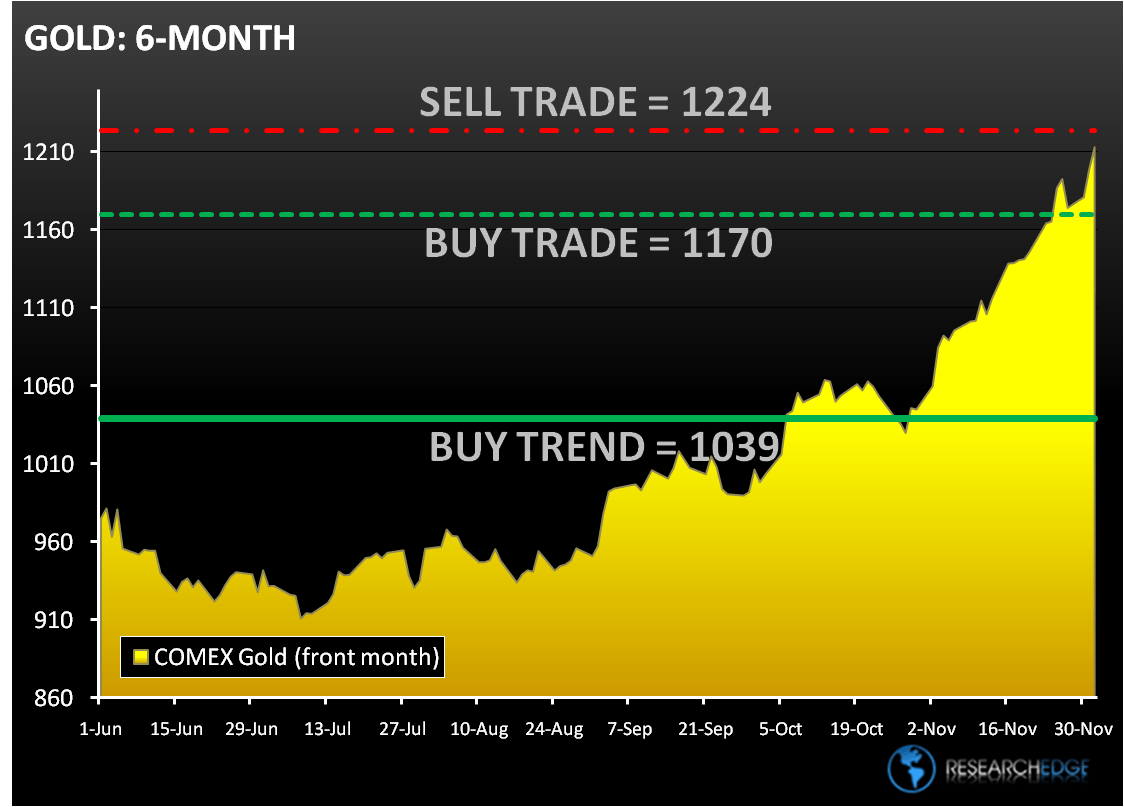

Last Wednesday our immediate term TRADE target for Gold was $1190, so we sold some. Then Gold corrected, and we bought back what we sold on Dubai Friday (gold was down, a lot).

This morning we entered the game with a 7% Gold position in the Asset Allocation Model, and I cut that in half as Gold tested our refreshed immediate term TRADE target of $1224. Unlike most sell-side strategists, we like to be on the right-side. Managing risk dynamically; changing our price targets proactively. As prices change, we do.

Some call this trading. It is – but when “long term investors” hit buy/sell buttons, that’s called trading too. What I have learned (the hard way) in this business is that it pays to manage the risk associated with price appreciation in long term TAIL positions. My daily challenge remains to improve this process, using math, as opposed to emotion. I continue to learn a great deal from chaos theory on this score. I continue to learn a lot about myself.

For now, the math says gold is in an immediate term TRADE bubble (TRADE = 3 weeks or less).

I’m not fighting it. I’m not selling all of it. I’m just selling some of it.

My risk management lines are in the chart below. I’ll be a buyer again of what I just sold on a pullback to my immediate term TRADE line of $1170/oz.

It’s ok to be long bubbles. Just be aware when you are in one (yes, Peter Schiff, that means you).

KM

Keith R. McCullough

Chief Executive Officer