Last week, as this chart of short term US Treasuries was making its final ascent up into the right of it’s crest, we called it one of the 3 main bubbles that He Who Sees No Bubbles (Bernanke) is not allowed to see:

- Gold (immediate term bubble)

- 2-year Treasuries (intermediate term bubble)

- Banker Bonuses (long term bubble)

So, don’t be shy about this – just see this for what it is and get hedged (SHY is the short term Treasury ETF that we shorted). With 2 year-yields testing 0.65% last week, it was mathematically impossible for yields to go much lower (unless we become Japan, which I guess is possible), particularly if you believe that maintaining a ZERO percent policy on US interest rates isn’t perpetual.

In fact, the only other times that 2-year yields have been this low are December of 2008 and all the way back in 1938 (the early months of 1939 and 2009 were not pretty for equity returns as yields moved higher from their lows).

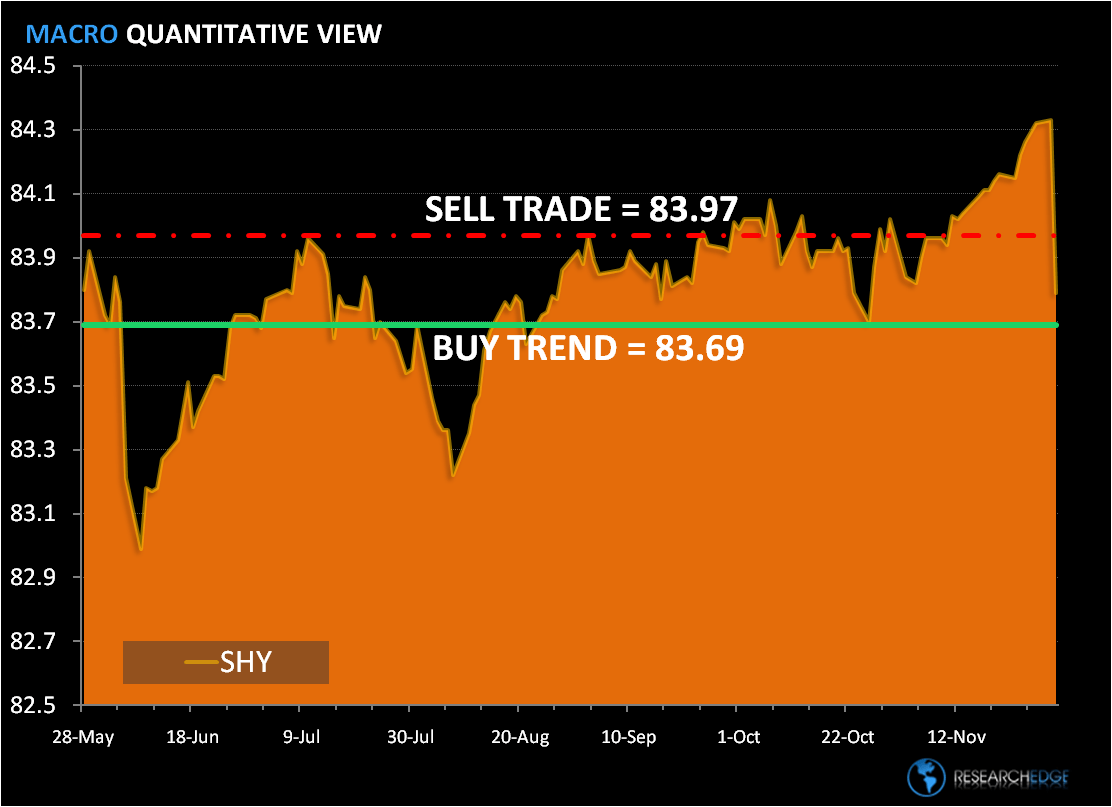

In the chart below, we have shown the SHY breaking its immediate term TRADE line (today). This raises a critical risk management signal in our macro model. It is both early and leading in terms of its indication. We will have to see if this immediate term breakdown in short term Treasuries holds.

He Who Sees No Bubbles has a unique problem with his vision – he cannot see what he is responsible for creating. Greenspan had really big glasses, but admitted in October of 2008 to missing this altogether as well. This is not new. Cheap money for a select few has plenty of unintended consequences.

KM

Keith R. McCullough

Chief Executive Officer