THE HEDGEYE EDGE

Unit Growth Decelerating In Food Retail – United Natural Foods (UNFI) has become increasingly dependent on unit growth, as same-store sales in the food retail space have evaporated. What happens to UNFI when their customers unit growth begins to subside? We are about to find out.

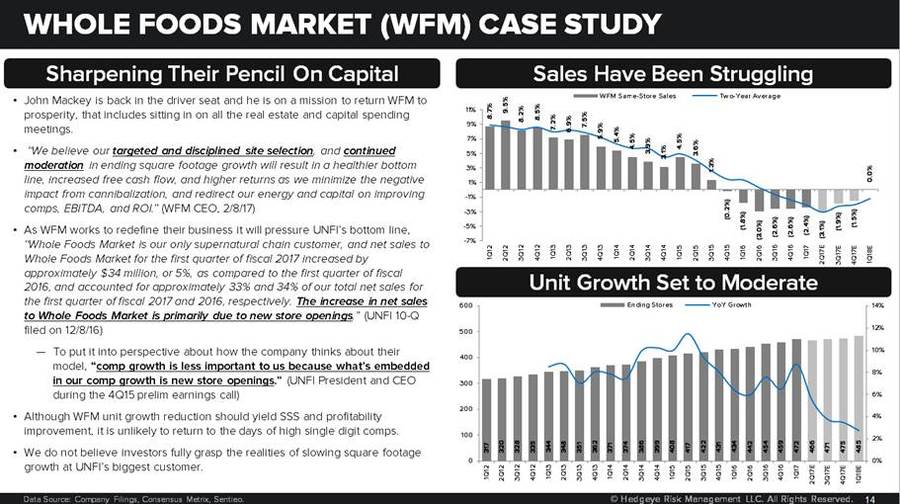

Unit growth in the industry is not what it used to be, but in our opinion we are due for meaningful contraction in new unit development at critical customers for United Natural Foods.

- Whole Foods (WFM) is suspect #1 in this case. It won’t necessarily be in 2017, but looking out to 2018 and 2019 we are predicting that we will see a meaningful reduction in new unit development, coupled with closures of underperforming units.

- Sprouts Farmers Market also noted a need to reduce new openings, pulling unit growth down to around 10% in 2018 and 2019.

- Outside of chains, independents are struggling as well, as many have had to shutter some of their doors in an effort to control costs.

Industry Pressures Not Waning Any Time Soon – Captive distribution and the proliferation of natural & organic food products are both headwinds for United Natural Foods' business.

Captive distribution is not a new threat by any means, but we believe it is underappreciated to some extent. As companies such as Boulder Brands and WhiteWave are acquired, parent companies will look to streamline operations/cut costs, which can lead to direct to customer shipments to the extent the customer is capable.

The proliferation of natural & organic products is not just a food retail phenomenon, it affects companies throughout the supply chain. This includes United Natural Foods, as natural and organic products have become more mainstream they have spread to channels beyond United Natural Foods' current reach and have gained attention from more conventional distributors.

Whole Foods is fixing its business, and one component of that is implementing a category management system in an effort to maximize their shelves. This will involve removing slow moving SKUs, which is United Natural Foods' bread and butter. To the extent this cuts down on SKUs United Natural Foods puts into Whole Foods stores, it will be a negative.

Margins Under A Microscope As Industry Evolves – As retailers battle for market share they have increasingly put pricing pressure on their suppliers. The latest news is that Wal-Mart (WMT) (not a United Natural Foods customer) is demanding suppliers lower their prices by 15%, and Wal-Mart has been on the journey towards lower price points for some time now.

A logical area to look for cost reductions is distribution. United Natural Foods is stuck between a rock and a hard place, yes they provide very valuable services for their customers while operating on razor thin margins, but what is stopping their partners from telling them to sharpen that razor just a little bit more.

We will see how this trend evolves with reflation, but we are not expecting it to get incrementally favorable in the near to medium term. Foreign exchange, product and customer mix shift to lower margins, competitive pricing pressure and moderated supplier promotional activity are expected to continue to tug and pull on margins.

ONE-YEAR TRAILING CHART