For the second day in a row the S&P 500 held the 1,081 trade line. The S&P 500 finished higher by 0.4% on light volume, although most of the day was spent in negative territory. The biggest headwind continued to be the Dubai World issue, although the potential contagion from the issues appears to be limited for the time being. Yesterday was a huge day of outperformance for the Financials (XLF), inching back above the TRADE and TREND lines, barely.

Setting aside the Dubai World concerns, there were a number of positive factors at work: (1) upbeat trends for Cyber Monday, (2) better-than-expected regional manufacturing data, and (3) Global semiconductor sales rose 5.1% in October; the eighth consecutive monthly increase.

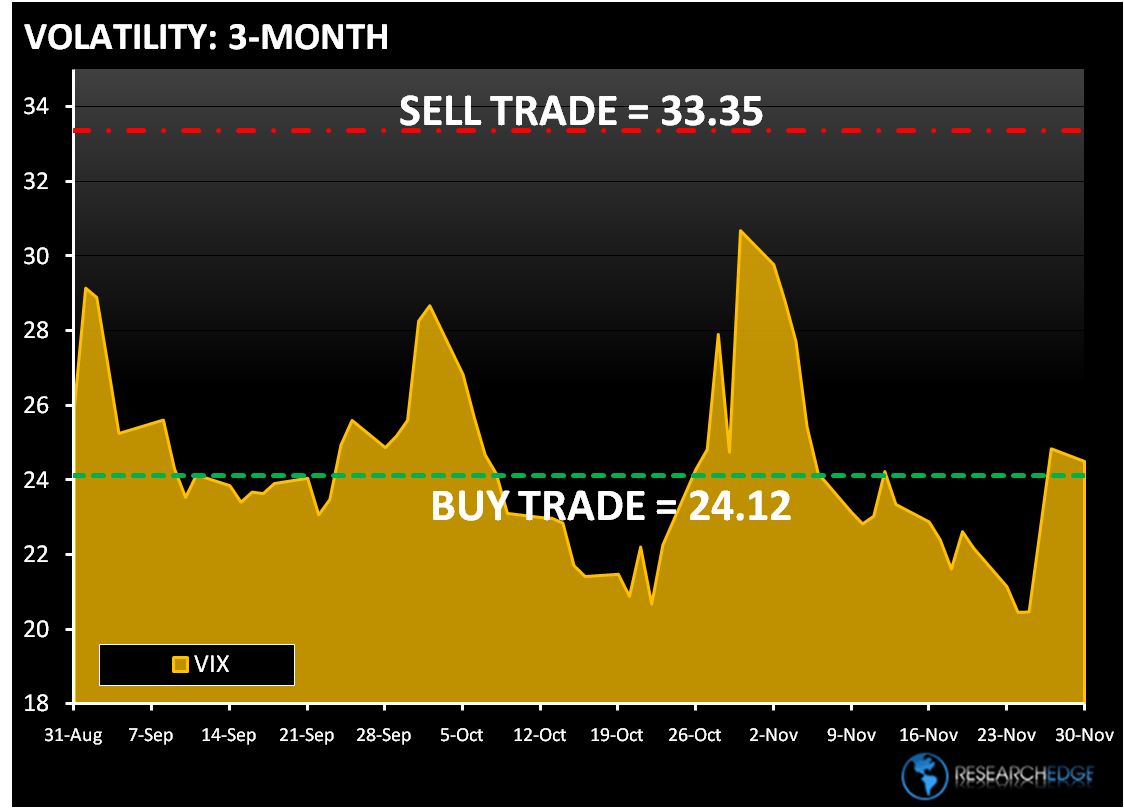

The Dollar index closed down 0.16% at 74.48 and the VIX was down slightly.

On the MACRO calendar, the Chicago PMI rose to 56.1 in November from 54.2 in October, the highest level since August of 2008. This compares to expectations for a pullback to the 53 level. New orders improved to 62.8 from 61.4, the highest level since May of 2007. Despite the good news, the names most leveraged to the RECOVERY theme underperformed. The Industrials (XLI) rose 0.3% and the Energy (XLE) was down 0.4%. It appears that Geopolitical concerns were more of an influence on the Energy related names.

On Monday, retail stocks were among the worst performers with the S&P Retail Index down 0.5%. The news from Black Friday was mixed with traffic up but average spending down.

Three sectors outperformed the S&P 500 (Financials, Materials and Utilities) and three sectors were down on the day (Energy, Healthcare and Consumer Staples). Consumer Discretionary (XLY) was flat on the day. The beneficiaries of Cyber Monday (AMZN) were offset by the weakness in the bricks and mortar retailers.

The Financials (XLF) sector was the best performer on Monday, rising 2.7%. The banks contributed most of the outperformance, with the KBW Bank index snapping a week long losing streak. Only four stocks declined in the (XLY), with AIG down 15% on the day. Concerns surrounding the potential contagion from Dubai eased on Monday.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 29 points or 1.5% upside and 1.5% downside. At the time of writing the major market futures are headed higher.

Crude oil is trading higher for a second Day as Chinese manufacturing expanded at the fastest pace in five years. The Research Edge Quant models have the following levels for OIL – buy Trade (75.11) and Sell Trade (75.58).

In London today gold rose to a record as the dollar declined and as increased geopolitical concerns over Iran’s nuclear program helping gold’s “safe-haven” status. Gold gained as much as 1.7% to $1,199.43 an ounce. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,163) and Sell Trade (1,203).

Like crude oil, Copper is trading higher for a third day as Chinese manufacturing expanded at the fastest pace in five years. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.09) and Sell Trade (3.20).

Howard Penney

Managing Director