“Choose a job you love and you’ll never have to work a day in your life.”

-Confucius

I didn’t choose this job. It chose me. For those who aren’t fans of me and/or my writing style, they will not be surprised that my first creative writing paper in college was deemed “un-grade-able.”

I figured my upside was that I could only improve from there.

From a rate of change 23 month-low in US jobs growth in December 2016 (+1.5% year-over-year), there’s only been upside to that (so far) for Donald Trump’s Presidency. Imagine the rate of change accelerates to 2-2.5% in the next 3-6 months?

Back to the Global Macro Grind…

I’m officially four months into being a US Growth Bull and I have to admit that it “feels” a lot better than being bearish while US growth slowed for 5 consecutive quarters. But you don’t read my research because you care about my feelings.

Reality is that the data “feels” nothing at all. Sure, it can take a trending time-series of data some time (2-3 months) to form tops and bottoms, but I don’t think people pay me to call tops and bottoms for them either. They pay for my team’s process.

Here’s how we read Friday’s US Jobs Report:

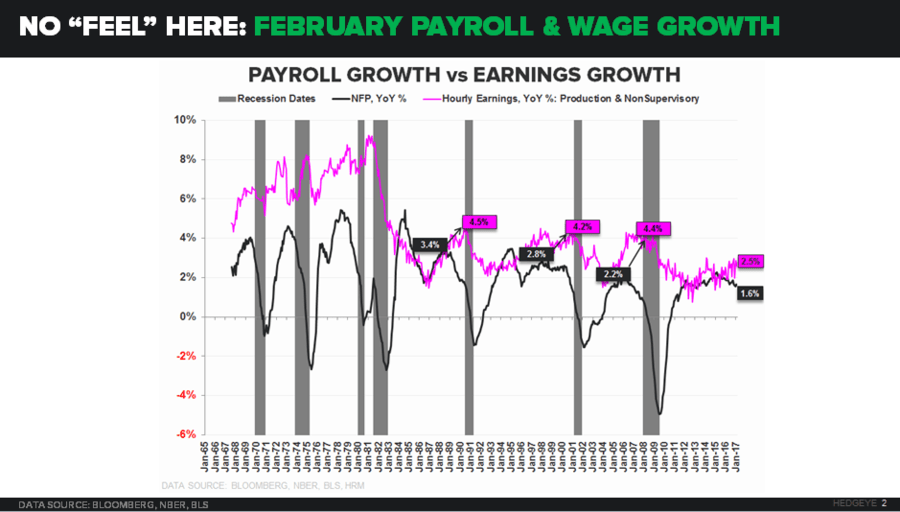

- FEB Non-farm Payrolls (NFP) = +235,000 with positive revision to JAN = +1.64% year-over-year FEB NFP growth with a probable acceleration thru May as year-over-year comps ease

- CYCLICAL GROWTH: Manufacturing = strong +28,000 gain with construction +58,000 as NFP agrees with ISM. Goods Producing employment growth accelerating a big +50bps sequentially to a 12-month (i.e. cyclical growth ↑) high

- WAGE GROWTH: JAN = revised higher and FEB accelerating off of that. Takeaway = not blockbuster but bullish TREND improvement continues; January angst over wage growth was overstated

Nope – neither did you hear a peep from the politically biased Old Wall Media about a “lack of wage growth” on Friday, nor did you see any accountability related to how wrong their consensus sources were on both the ADP and NFP reports last week.

Instead, it’s easier for my competitors (and hedgies on the wrong side of this move) to talk about my “tone.”

It’s a good thing you (and our entire profession) doesn’t get to evaluate their tone! Imagine reading a super smart hedgie’s daily take on why US growth, inflation, profits, confidence, employment, etc. really isn’t accelerating?

One guy (angry dude) literally sent me a critical email last week saying “nice call so far but I don’t believe the data.”

Alrighty then. Moving along (and right back to the data), here’s what happened in FICC last week:

- US Dollar has its 1st down week in 5, correcting -0.3% last week = +6.2% in the last 6 months

- EUR/USD bounced +0.5% last week but is still -5.0% in the last 6 months

- Yen dropped -0.7% vs. USD and the Nikkei rallied another +0.7% week-over-week, in kind

- British Pound lost -1.0% vs. USD as it tries to make a higher-low vs. the last 6 months of lows

- US 2yr Treasury Yield ramped another 5 basis points to close at a new weekly cycle high of 1.35%

- US 10yr Treasury Yield added another 10 basis point week-over-week at +2.57% (+90bps in last 6 months)

- CRB Commodities Index deflated another -3.7% on the week, taking its 6 month move back to +0.1%

- Oil (WTI) got smoked, losing -9.1% week-over-week, taking its 6 month move to -1.6%

- Gold lost another -2.0% week-over-week, taking its 6 month draw-down to -10.4%

- Copper corrected -3.8% week-over-week, taking its 6 month reflation back to +23.3%

That’s right, since #TheCycle clearly bottomed 4-6 months ago, it’s very obvious to see, in hindsight, that #StrongDollar and Rates Rising is bad for something like Gold inasmuch as it’s been bullish for the US Dollar and US Stocks:

- SP500 had its 1st down week in 7 last week, correcting a whopping -0.4% = +11.5% in the last 6 months

- Nasdaq only corrected -0.2% last week = +14.4% in the last 6 months

- Russell 2000 corrected for real, -2.1% last week, but is right in-line with the SP500 return in the last 6 months

So if you agree that both US growth and employment continues to accelerate from their respective mid-cycle slow-down lows, I say that the Russell Growth (IWO) is one of the better places to be buying the dip this week.

I know, I know. It probably looks bad on some dude’s chart or “count”, but so did the Nasdaq in both late November and late December. “Technically” speaking, I guess the Financials (XLF) looked like they were “breaking down” in January too!

And you wonder why I antagonize some people. Lol

This is a very competitive game that we’re all egregiously overpaid to play. If I didn’t try to make you feel something about the score every morning, I wouldn’t love being the coach some people love to hate.

God willing, I’ll get to play the game alongside you for many years to come. Thanks to all of you who put up with me being human… and for giving me an opportunity to wake up at the top of the risk management morning, loving what I do.

Our immediate-term Global Macro Risk Ranges (with TREND views in brackets) are now:

UST 10yr Yield 2.51-2.65% (bullish)

SPX 2 (bullish)

RUT 1 (bullish)

NASDAQ 5 (bullish)

Nikkei 192 (bullish)

USD 100.50-102.51 (bullish)

EUR/USD 1.04-1.06 (bearish)

YEN 113.17-115.37 (bearish)

Gold 1187-1224 (bearish)

Copper 2.55-2.75 (bullish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer