Our Technology Team – led by Ami Joseph – will be hosting a deep dive institutional call on our long Corning (GLW) call.

The call will take place on Wednesday March 15, at 1pm ET.

Email sales@hedgeye.com for more information.

KEY DISCUSSION POINTS

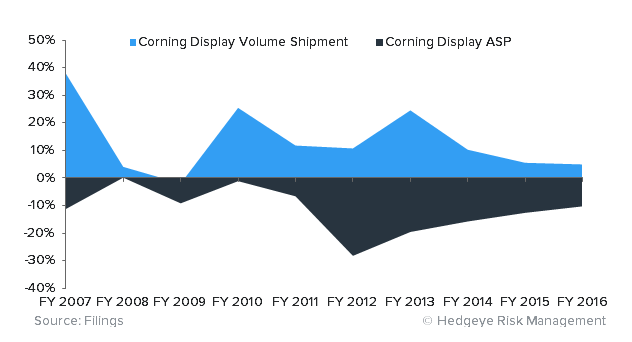

- The Unknowns here are around TV Units. We see the setup for a classic replacement cycle bubbling up, and in this deck we walk you through the math and the catalysts as well. If we are right about the direction of TV units, Corning revenue gets a boost from units + faster shift to larger screen TV + tight glass market yielding to better pricing. 2017 is the first year in a while not facing a down year in Display GM...how will all this translate to 2018 GM.

- There are several Known positives, not reflected. Gorilla Glass is getting a large content shift in the next generation iPhone. Typically, Apple leads the market and others follow, especially given the underlying technology reasons that Apple is shifting to a glass back. When we waterfall that content growth across high end smartphones, and also factor growing penetration for GG3 in the mid-tier, the effect is a ~2x on Gorilla Glass revenue by 2019. In Optical, carrier networks are investing in fiber, and in the US Corning has a strong market and technology lead. We show a # of positive vectors in this area, notwithstanding some recent lumpiness in the optical supply chain. Finally, the environmental business has a 3-4x content growth opportunity in the years ahead. All of this translates, to us, as better than wimpy 4%, 1%, and 4% growth modeled by the Street in 2017-2019.

- A Forgotten LONG whose time has come. The Street is more or less ambivalent about Corning's stock, featuring 8 buys, 10 holds, 1 sell, and more than 3 days to cover on the short side. Valuation is choppy due to the cyclicality of the industry, but if you believe in the dream, namely - that the company has multiple drivers that will lift revenue estimates in the coming 8-9 quarters, then you will be rewarded with enormous FCF, for a company returning 8% of the cap in a buyback and a 2%-plus div yield, AND, has bought back 24% of the share count in the last 24 months. And, let's be honest, in this time we all need cyclical longs we can live with, and this one is for living!!

Long awaited upside cometh!

CALL DETAILS

Ping sales@hedgeye.com for more information. Please note if you are not a current subscriber to our Technology research there will be a fee associated with this call.

ABOUT HEDGEYE

Hedgeye Risk Management is a leading independent provider of real-time investment research. Focused exclusively on generating and delivering investment ideas, the firm combines quantitative, bottom-up and macro analysis with an emphasis on timing.

The Hedgeye team features some of the world's most regarded research analysts - united around a vision of independent, uncompromised real-time investment research as a service.