I’m not referring to Tiger Woods, but the Financials (XLF). The XLF is the first sector to break TRADE and TREND!

After a mini crisis on Friday, the market looks to open modestly higher today as some of the fears from the Dubai debt crisis are mitigated and the focus is holiday sales trends. The S&P 500 closed down 1.7% on Friday and has now been down five of the last seven days. On Friday the S&P 500 held the 1,081 TRADE line in quiet post-holiday trading.

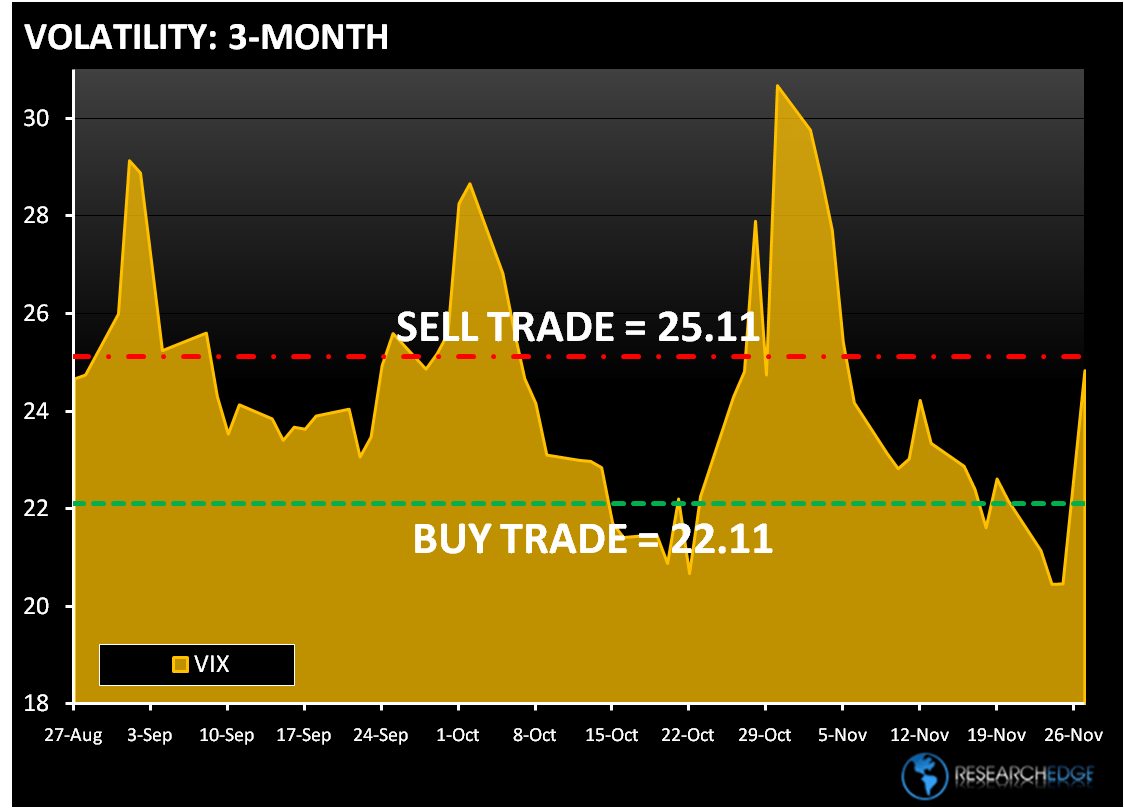

The Dubai World credit issue has taken the wind out of the sails of commodities and commodity stocks, which have been the biggest beneficiaries of the RECOVERY trade. The Dollar rose 0.2% on the day and volatility surged as the VIX rose 21% on the day.

The Holiday shortened week was relatively quiet one with the Dow and the S&P 500 basically unchanged on the week. The NASDAQ declined 0.4% and Russell 2000 1.3%. Last week the MACRO calendar provided some better-than-expected economic data on the employment and housing picture. Also adding to the positive tone was increased M&A activity and some better than expected earnings and guidance from some selected retail names.

On Friday, four sectors outperformed the S&P 500, but every sector was down on the day. Consumer Staples (XLP), Healthcare (XLV) and Technology (XLK) were the best performing sectors. The

relative outperformance came from renewed momentum in the SAFETY trade due to the strong dollar and weak commodities.

The worst performing sectors were Materials (XLB), Financials (XLF) and Consumer Discretionary (XLY). The XLF is the first sector to break both key durations - TRADE and TREND. The Energy sector (XLE) is the other sector to be broken on the TRADE duration. Within the XLF, Insurance and Diversified Financials were the worst performing industries and regional banks were the best performing names. The three best performing names in the XLF were STI, PBCT and HCBK.

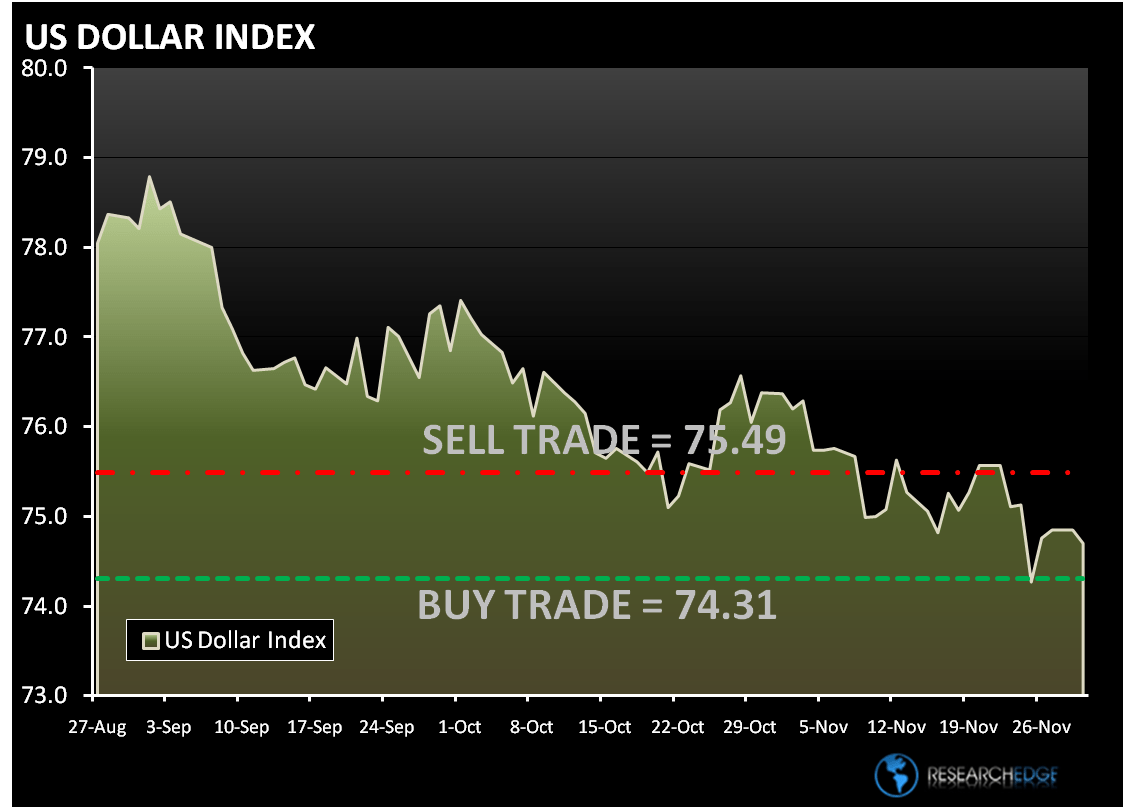

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 21 points or 1% upside and 1% downside. At the time of writing the major market futures are down slightly.

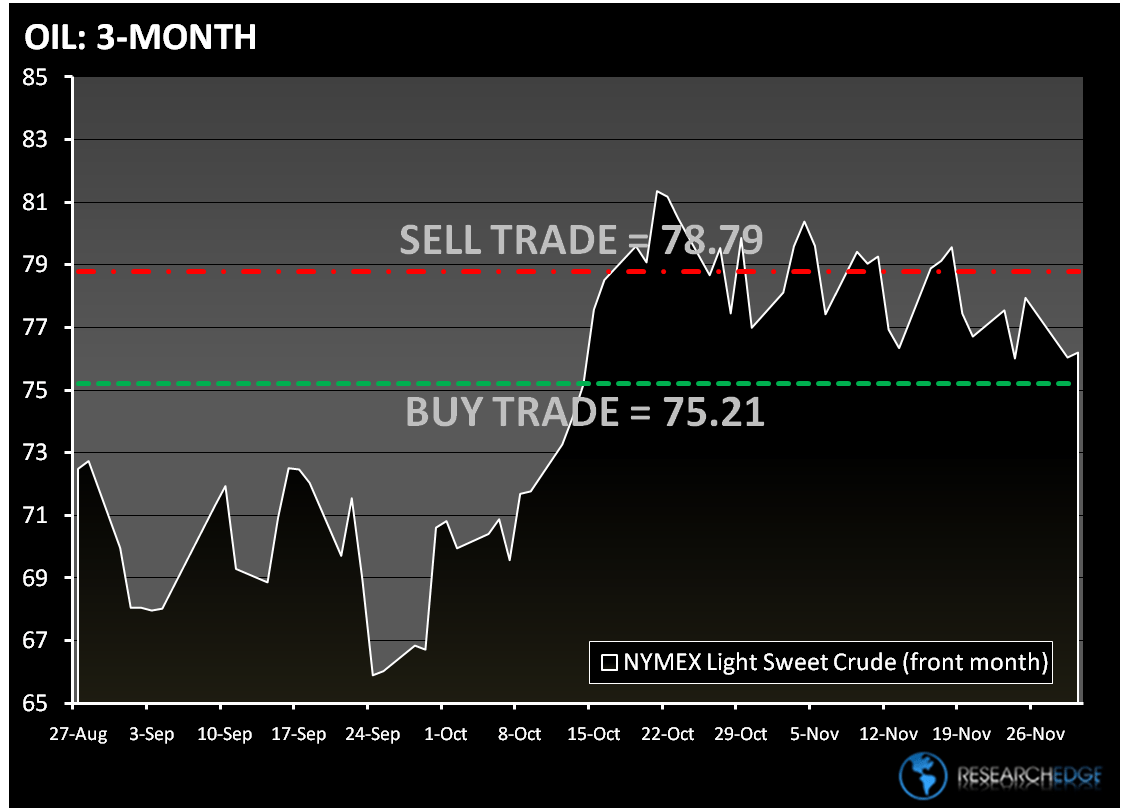

Crude oil is trading higher on U.A.E. backing of the Dubai Banks and a weaker dollar. The Research Edge Quant models have the following levels for OIL – buy Trade (74.31) and Sell Trade (75.49).

On Friday, Gold dropped over 4%, but it remains in a bullish formation from a TREND and TRADE perspective. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,163) and Sell Trade (1,190).

Copper is higher in early as concerns of Dubai World eases. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.09) and Sell Trade (3.18).

Howard Penney

Managing Director