MARKET WATCH: What’s Happening? By every measure, the U.S. agriculture sector has struggled in recent years thanks first to the commodity price crash in 2014, and more recently to El Niño’s favorable weather. Now that the tropical storm cycle has passed, many farmers and agricultural firms are hopeful that the sector is primed for a 2017 rebound.

Our Take: This bullishness, however, fails to take into account what we know about weather cycles and global demand. El Niño may very well re-emerge before year’s end, while global warming will continue to act as a long-term drag on prices. Moreover, the United States is rapidly losing ground to emerging markets that have ramped up their agricultural production.

New U.S. Department of Agriculture (USDA) projections indicate that there will soon be fewer than 2 million farms in the United States—the lowest number since the Louisiana Purchase.

This troubling factoid is just the latest sign of the agriculture sector’s weakness. U.S. farms have been struggling by almost every measure since the Great Recession: A recent USDA report reveals that the United States has lost more than 100,000 farms since 2009, with total farm acreage falling by 6 million over that period.

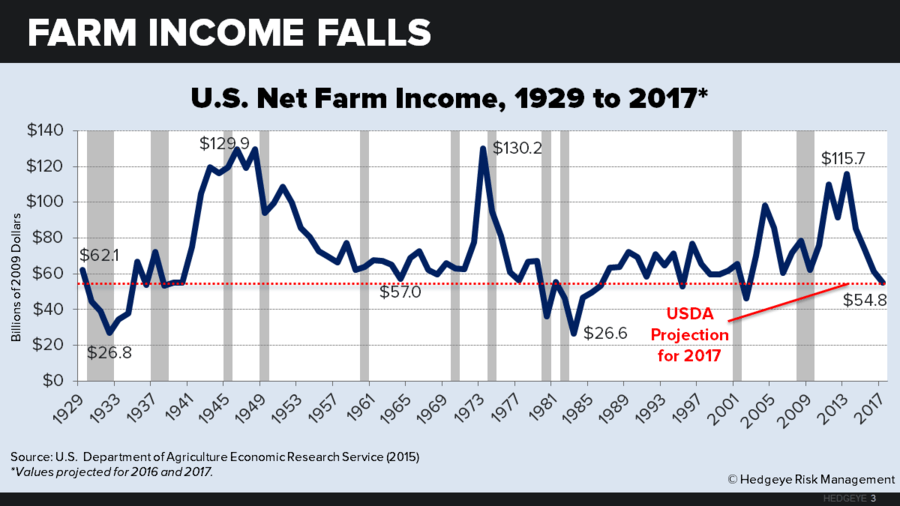

True, as recently as 2013, U.S. net farm income was on the rise—temporarily buoyed by soaring commodity prices. But those days are long gone. USDA estimates that U.S. real farm income will drop 11% YOY in 2017, which would mark the fourth consecutive year of negative growth. If farm income does indeed drop in 2017, it would tie the sector’s longest losing streak since the Great Depression.

Farming’s recent troubles have been compounded by a plunging top line. Prices of major food commodities fell for the fifth consecutive year in 2016, according to the U.S. Food and Agriculture Organization’s Food Price Index, a trade-weighted index tracking international market prices. Crops like corn and wheat, staples of U.S. agricultural production, have fared the worst. According to IMF data, corn cost $153 per ton at the end of 2016, down by more than half from its late-2012 peak. Wheat prices have dropped by nearly two-thirds over that time.

Successive banner harvests have left farmers with such a supply glut that infrastructure companies like Great Bend Co-op are building massive bunkers the size of football fields to accommodate the excess output. The grain surplus is so pronounced that U.S. farmers recently planted the fewest acres of winter wheat in more than a century.

WHY THE FARMING SECTOR REMAINS OPTIMISTIC

Despite these grim statistics, plenty of farming insiders believe that 2017 will be a rebound year for U.S. agriculture.

One such player is agricultural equipment manufacturer Deere & Company (DE). The firm recently raised its full-year profit forecast, citing strong orders in Q1 2017. DE’s optimism must hinge heavily on what company executives think about the U.S. market, considering that the firm earns 58% of its revenue within U.S. borders.

Farmers, meanwhile, are also showing some fight. Planters are going all-in on soybeans, which are relatively more profitable now that corn prices have tanked. Research from Farm Futures and AgriSource, two sector forecasters, reveals that U.S. farmers are poised to sow more acres of soybeans than corn in 2017—which would mark the first such occurrence since 1983.

What’s behind this optimism? The prevailing view is that recent harvests have been aided by favorable growing conditions brought on by El Niño—which ended last year. The El Niño Southern Oscillation (ENSO) is a variation in winds and sea surface temperatures over the Pacific that comes in two flavors. The first is El Niño, which sends warmer, wetter weather (i.e., favorable for crops) to North America—and cooler, drier weather to the Western Pacific. The script is flipped for La Niña, during which warm weather heads to the Western Pacific and cool weather heads to North America.

The relationship between weather and commodity prices has been well established. Recent history is full of severe weather patterns that coincided with rising or falling commodity prices. For example, much of the 2012 commodity boom can be attributed to a severe U.S. drought that hammered output.

In fact, the very timing of ENSO cycles appears to have some correlation with commodity prices. Since 1980, global corn and wheat prices usually are low and/or falling during El Niño periods, and are high and/or rising in between. Presumably, El Niño brings favorable weather to the United States (the world’s top exporter of these crops), which boosts yields and slashes prices. Thus, in the absence of El Niño, it’s reasonable to expect that prices would bounce back.

WHY INVESTORS SHOULD PUMP THE BRAKES

But the immediate and long-term future of U.S. agriculture is darker than it appears. Why?

El Niño may be on its way back. For starters, farmers shouldn’t count on a weather-fueled price rebound. ENSO does not repeat in a strict pattern: El Niño tends to occur every two to seven years (hardly regular enough to set your watch on), and can last anywhere from a few months to two years. Thus, a long El Niño cycle like the one we’ve just exited does not guarantee an equally long La Niña cycle. Indeed, the most recent National Oceanic and Atmospheric Administration data indicate that La Niña—which began just last summer—is already over. So much for a sustained dry spell that boosts crop prices.

Worse yet, consensus forecasts predict that El Niño conditions could return within the next few months, a conclusion reflected in meteorologist forecasts calling for higher spring moisture over many planting states.

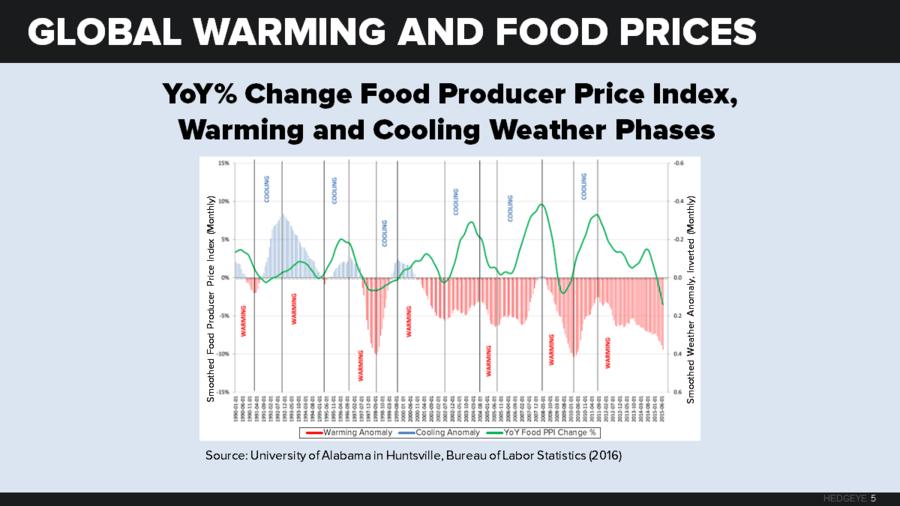

Global warming will be a long-term drag on commodity prices. Systemic climate change is working against U.S. farmers as well. For many years, there’s been a big debate about whether global warming would hurt or help agriculture, but recently the evidence has been mounting: It looks like in aggregate, a warmer global climate guarantees higher agricultural output, which pushes down prices. By plotting global temperature variations since 1990 against changes in food prices, natural resources expert Erico Matias Tavares discovered that the two are inversely related—that is, growth in food prices decelerates or turns negative as temperatures rise.

To the extent that global warming is occurring, this relationship will guarantee ever-lower profit margins for farmers.

Global demand for U.S. farming isn’t what it used to be. Just as dire as weather effects are shifting global trade habits that could permanently reduce demand for U.S. agricultural exports.

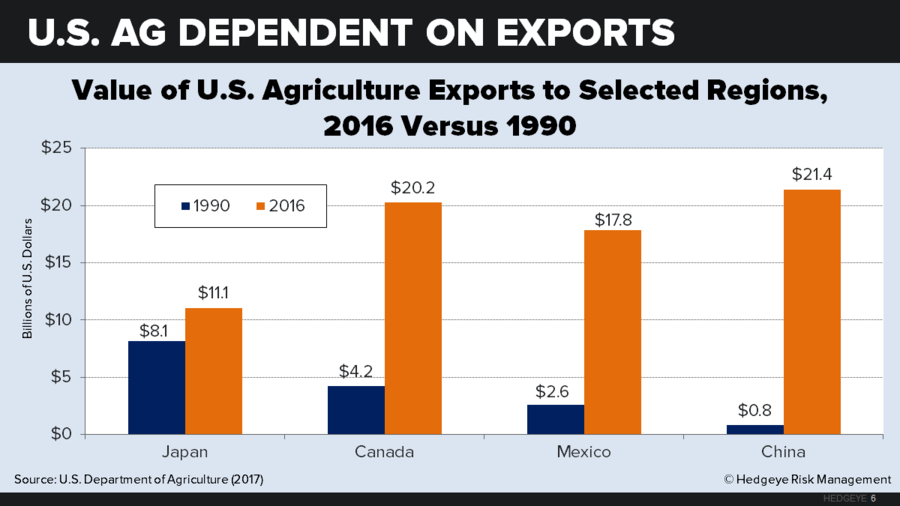

Trade has been a boon to U.S. farms for decades. Since 1990, the value of agricultural exports to China (America’s biggest export market) has surged more than twentyfold. But over the past few years, demand has cooled considerably. The value of U.S. agricultural exports to each of America’s top markets (China, Canada, Mexico, and Japan) has dropped since 2014. U.S. exports to China peaked all the way back in 2011.

Why has demand slowed? For one, a rising U.S. dollar has made America ever-less price-competitive. Yet a higher dollar wouldn’t matter if the United States was the only place to get agricultural commodities—but increasingly that’s no longer the case. Emerging markets have stepped up their farming efforts to take advantage of skyrocketing Chinese demand.

It was always unnatural that the United States would forever remain the world’s top agricultural exporter, even as it exploited its comparative advantages in IT, capital goods, pop culture, and professional services. Sooner or later, lower-wage countries would adopt our same agricultural know-how and exploit their own comparative advantage. That finally appears to be happening. China is turning away from U.S. agricultural exports in favor of Brazilian and Argentinian goods. Argentinian President Mauricio Macri recently eliminated a 23% export tariff on wheat to incentivize production. Russia, meanwhile, overtook the United States as the world’s top wheat exporter last year. Interestingly, falling energy prices seem to encourage rising global agricultural production: All these new farming competitors are raw materials exporters that have been compelled to find another revenue source—and have been given the opportunity via falling local currency/US$ FX rates.

WHAT’S AHEAD?

President Trump’s trade and fiscal stimulus policies may put even more heat on U.S. farmers. One of Trump’s first orders of business after entering office was to pull out of the Trans-Pacific Partnership, a move lauded by those who felt that TPP gave American workers a raw deal. Yet TPP was coveted by at least one group: U.S. farmers. The deal created as much as $5 billion in potential agriculture sales value by opening up Pacific Rim nations to U.S. exports.

Trump’s policy agenda is not likely to do much—if anything at all—to help farmers. His plan to deficit-spend the economy out of its funk would be unambiguously bad for agriculture, since it would further boost the dollar. (Anyone recall how Reagan’s early-1980s deficit brought U.S. farmers to their knees via a skyrocketing dollar—ultimately forcing Reagan to reverse course with the Plaza Accord?) The border-adjustment tax would be a net plus, since it would shower exporters with subsidies. Keep in mind, however, that most economists believe that most of this gain would be wiped out by (yes) a further rise in the dollar.

And that’s not all. Restrictive trade policies, especially with China and Mexico (two of America’s top three agricultural export markets), would hammer U.S. farm revenue. In fact, tough trade talk is one reason why Mexico introduced a bill that would shift the country away from U.S. corn imports.

THE BOTTOM LINE

So which companies are most affected by these headwinds? Scaled-up, global firms with diverse business lines have relatively little to worry about. These include massive “agribusinesses” like Monsanto and Dow Chemical—which ironically are the very firms that brought cutting-edge agricultural technology to emerging markets in the first place. They’ve lately been globalizing through M&As to hedge themselves against U.S. market risks. (We discussed this issue at length here: “Big Ag’s Merger Madness: A Defensive Move Against Emerging Threats.”)

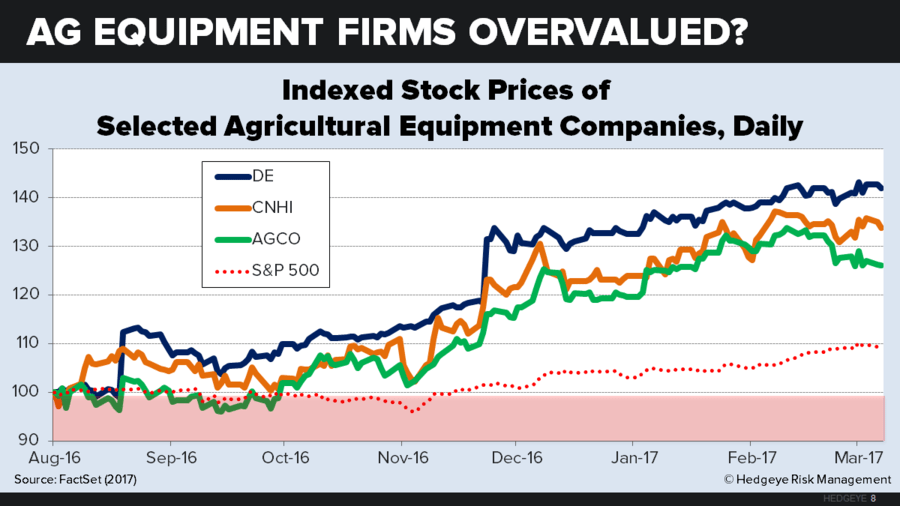

Agricultural machinery companies are a different story. Hedgeye’s own Industrials sector points out that investors seem to have priced in the assumption that the agricultural equipment market has already hit rock bottom. However, as our colleagues wisely conclude, there is still plenty more room to fall—due to the unfortunate combination of a weak U.S. farming sector and a historically young equipment fleet. DE is the most exposed to these risks, earning 58% of its revenue from the United States (and 0% from any of the emerging market hot spots mentioned earlier). DE’s main competitors, CNH Industrial (CNHI) and AGCO Corporation (AGCO), are somewhat better hedged; each earns only about 20% of revenue from the United States and 6% to 7% from Brazil.

The prospects are just as dire (if not more so) for farmland REITs, a category that includes several small-cap firms that went public around the time that commodity prices were booming in 2013. Today, U.S.-based firms like Farmland Partners (FPI) and Gladstone Land (GLAD) are competing for an ever-shrinking pool of land in a troubled sector.