As one indicator of sentiment that we track, the GfK released its December German Consumer Confidence report today. In contrast to yesterday’s release of the German Ifo Business Confidence Survey that showed a measurable increase in the business climate (93.9 in November versus 92.0 in October), today’s consumer report falls more in line with our overall intermediate outlook for the Eurozone’s largest economy, and the region itself.

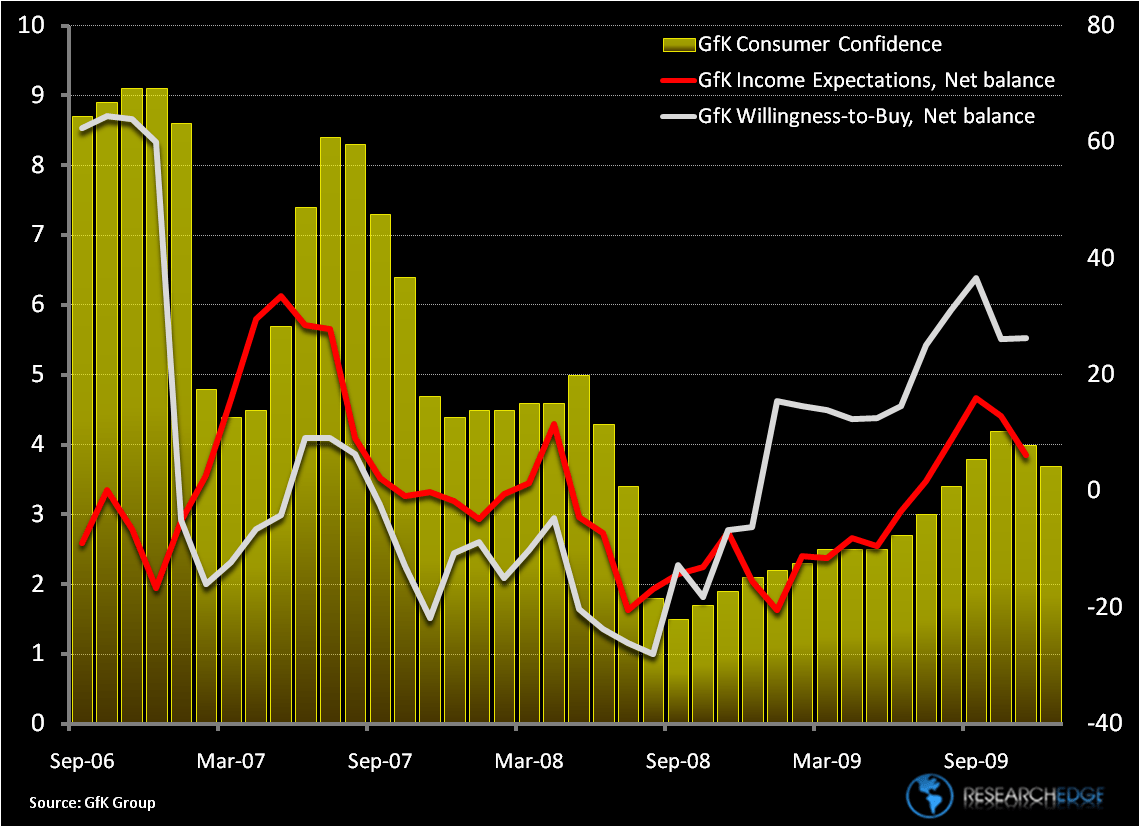

Consumer confidence fell to 3.7 in December from 4.0 in the previous month, while the sub-surveys of economic and income expectations declined significantly and consumers’ propensity to spend was flat. More broadly, the data has been trending downward over the last months (see chart below).

We continue to expect the rate of improvement in broader fundamentals to slow sequentially into year-end and in 1H ’10 for Germany, and many Eurozone countries, with mild growth next year. That said, one bullish indicator for Germany has been its rate of unemployment, which has held steady ~8.1% over the last four months. And today the government announced that its program (subsidy) of shortened work hours or part-time jobs, known as Kurzarbeit in German, which was set to expire at year-end and by all measures was the substantial crutch in maintaining employment, will be extended by another 12 months. The decision by Chancellor Angela Merkel’s government means that the state will pay up to 67% of a worker’s salary for a period of up to two years to keep workers across industry “employed”. Recent data suggests that some 1 million workers were covered under the program.

While prolonging Kurzarbeit should hinder joblessness, on the TAIL we’re left to wonder if striking jobs now would be a better solution, both limiting government expenditure and encouraging companies to right-size their labor force...

Irrespective of the government’s extension of short-time work, we still expect joblessness to be a major concern for the consumer in 2010. Neither Eurozone PMI data out this week (See Topping Off on 11/23) nor German private consumption Q3 figures suggest the consumer is ready to spend, and the stimulus associated with the country’s cash for clunkers is now rear-view. Additionally, today’s news from the Bundesbank that German banks may need to further write-down another 90 Billion Euros of bad loans won’t add confidence in the broader economy.

While we see bearish fundamental headwinds for Germany ahead, and as an extension for Eurozone countries that rely on the stronger economies of the region like Germany and France for trade, we are on balance bullish on the German economy versus some of its European peers as we believe that global demand should melt up to support Germany’s industrial and manufacturing base.

Matthew Hedrick

Analyst