It’s a quiet week for some. Yesterday the S&P 500 declined 0.1%; the NASDAQ declined 0.3%, while the higher beta Russell 2000 declined 0.4%. The S&P 500 has now closed down 4 out of the last 5 days and the Dollar Index has been lower for the past three.

The MACRO calendar continues to provide mixed signals as the momentum of the RECOVERY theme stalls. Our overall take from yesterday’s economic calendar was supportive of our concerns about the trends in the labor market and the implied health of the US consumer. Not surprisingly, the more defensive-oriented sector out performed yesterday, with the exception of Energy (XLE). Given the performance of the XLE yesterday, the Research Edge quant models are now flashing PERFECT – all nine sectors are perfect on TRADE and TREND.

Yesterday, Q3 GDP growth was revised to 2.8% vs. the previously reported gain of 3.5%. The biggest adjustments to Q3 GDP were deteriorations in the net exports and in personal consumption expenditure, reflecting a less-robust boost from the cash-for-clunkers program. In addition, consumer confidence rose to 49.5 in November from an upwardly revised 48.7 in October. The present conditions index is at a 26-year low and the labor market differential deteriorated. On the housing front, the S&P Case-Shiller index rose 0.3% month-to-month in September after a 1.1% increase in August.

Today’s MACRO calendar is full with MBA Mortgage applications, Personal income and spending, initial jobless claims, U. of Michigan confidence and new home sales--all to be reported by 10am EST.

On Tuesday, the VIX declined 3.3% and has now declined 8.7% over the past week. We are long the VXX.

While the S&P 500 was down slightly, four sectors turned in a positive performance. The best performing sector was Healthcare (XLV +0.8%), followed by Energy (XLE +0.6%), Consumer Staples (XLP +0.2%) and Utilities (XLU 0.2%). Thanks to Medtronic’s positive outlook, the Med-tech names provided the bulk of the upside, and the managed care group continues to outperform.

The worst performing sectors were Technology (XLK), Financials (XLF) and Industrials (XLI). The drag in the XLK was due to BRCD down 9% and sell-side downgrades on DELL. The XLF was being dragged down by the banks on the back of capital concerns emanating from Washington and Real Estate related names.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 35 points or 1% upside and 2% downside. At the time of writing the major market futures are pointing to a positive open.

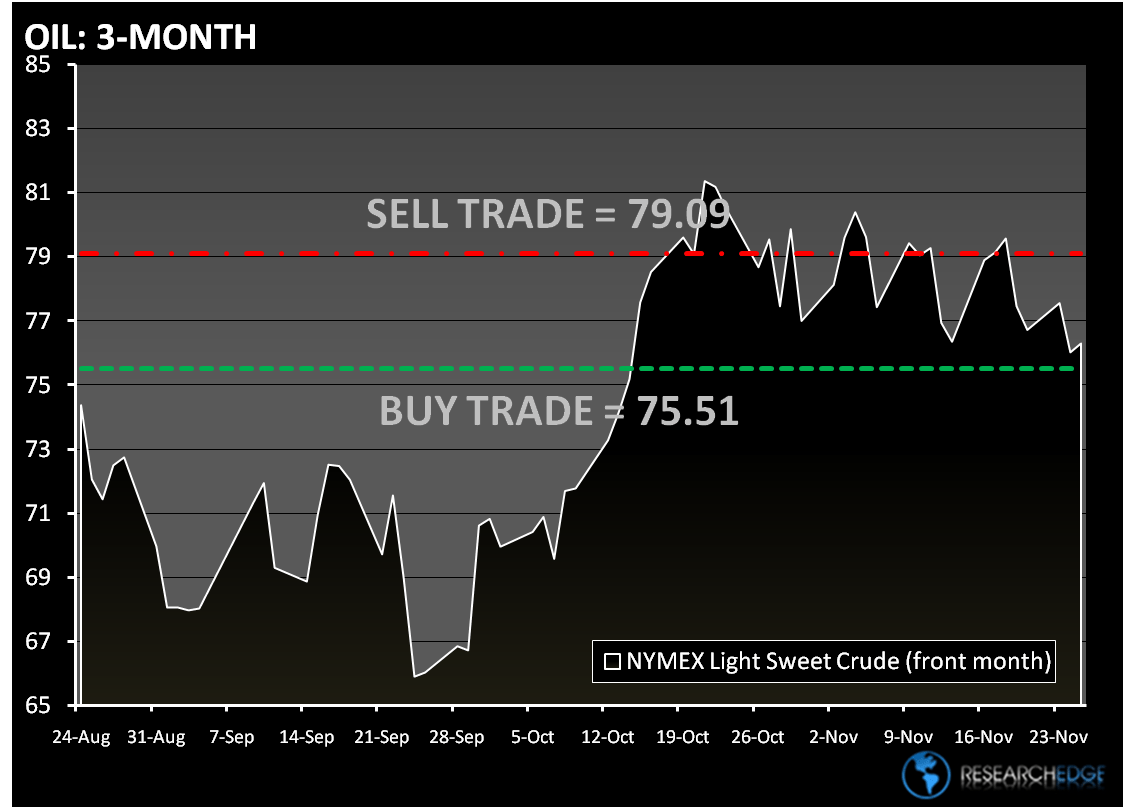

Crude oil is trading basically unchanged ahead of the U.S. Energy Department inventory report. The Research Edge Quant models have the following levels for OIL – buy Trade (75.51) and Sell Trade (79.09).

Gold rose to a record $1,176.50 an ounce in the morning “fixing” in London. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,143) and Sell Trade (1,189).

Copper is higher for the third time in four days as the dollar has declined for three straight days. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.01) and Sell Trade (3.22).

Howard Penney

Managing Director