On Monday the market was higher across the board on DEAD volume. The S&P 500 rose 1.4% (in line with the NASDAQ), while the higher beta Russell 2000 rose 1.7%. Overall, this was the first up day of the last four as a 0.75% decline in the Dollar Index provided a tailwind for the equity market.

The MACRO calendar put the housing RECOVERY theme back in play. After a series of disappointing headlines last week, existing home sales jumped 10.1% month-over-month in October to an annualized 6.1M units. This represents the highest level since February of 2007. In addition, month's supply fell to 7 in October from 8 in September, with total inventory down 3.7% from September's levels. From an equity perspective, with the exception of DRH, there was no follow through as most of the homebuilders finished lower yesterday; the extension of the homebuyer tax credit is only a temporary band aid to the issues facing the housing market.

Today’s MACRO calendar is full with a GDP revision at 8:30am (consensus is looking for 2.8%), followed by Case-Shiller at 9:00am (consensus is looking for -9.1%) and consumer confidence at 10:00am (consensus is looking for 47.5).

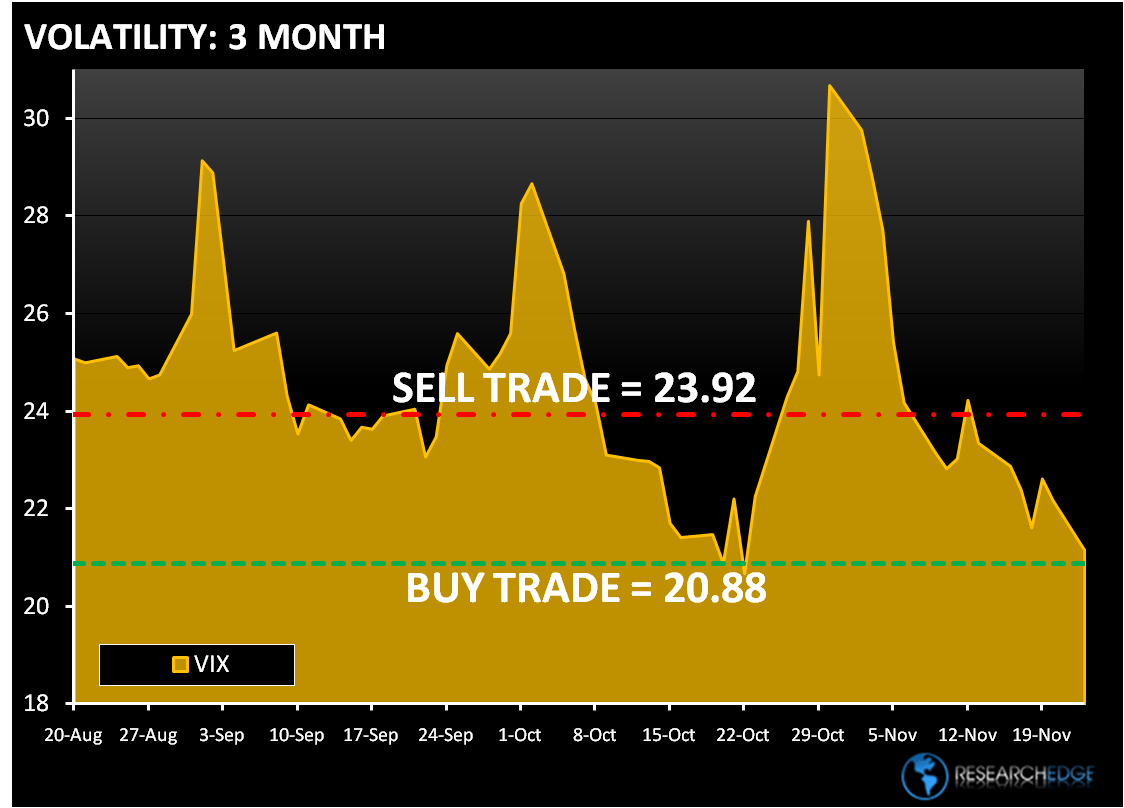

On Monday, the VIX declined 4.6% and has now declined 7.6% over the past week. Yesterday we bought the VXX. Now that the market is hitting its YTD high it is as good a time as we have seen all year to buy some volatility. Our oversold line for the VIX is 21.03.

Every sector was up on Monday, but only three sectors outperformed the S&P 500 – Industrials (XLI), Technology (XLK) and Financials (XLF). The best performing sector was the XLI, up 1.8%. GE led the XLI higher by 2.8% yesterday. Within the XLF, the banking group was one of the best performing subsectors. The regional names were among the best performers as ZION rose +12.5%, STI up 5% and RF up 4.4%.

The worst performing sectors were Healthcare (XLV), Consumer Discretionary (XLY) and Consumer Staples (XLP). While the XLV underperformed the S&P 500 by 0.5%, managed care was a bright spot as JPMorgan upgraded CI and WLP. The difficulties of Healthcare reform remain as the Democrats face an uphill battle gathering sufficient support to approve the legislation in its current form.

From a risk management standpoint, the ranges for the S&P 500, the Dollar Index and the VIX are seen in the charts below. The range for the S&P 500 is 33 points or 1% upside and 2% downside. At the time of writing the major market futures are basically flat on the day.

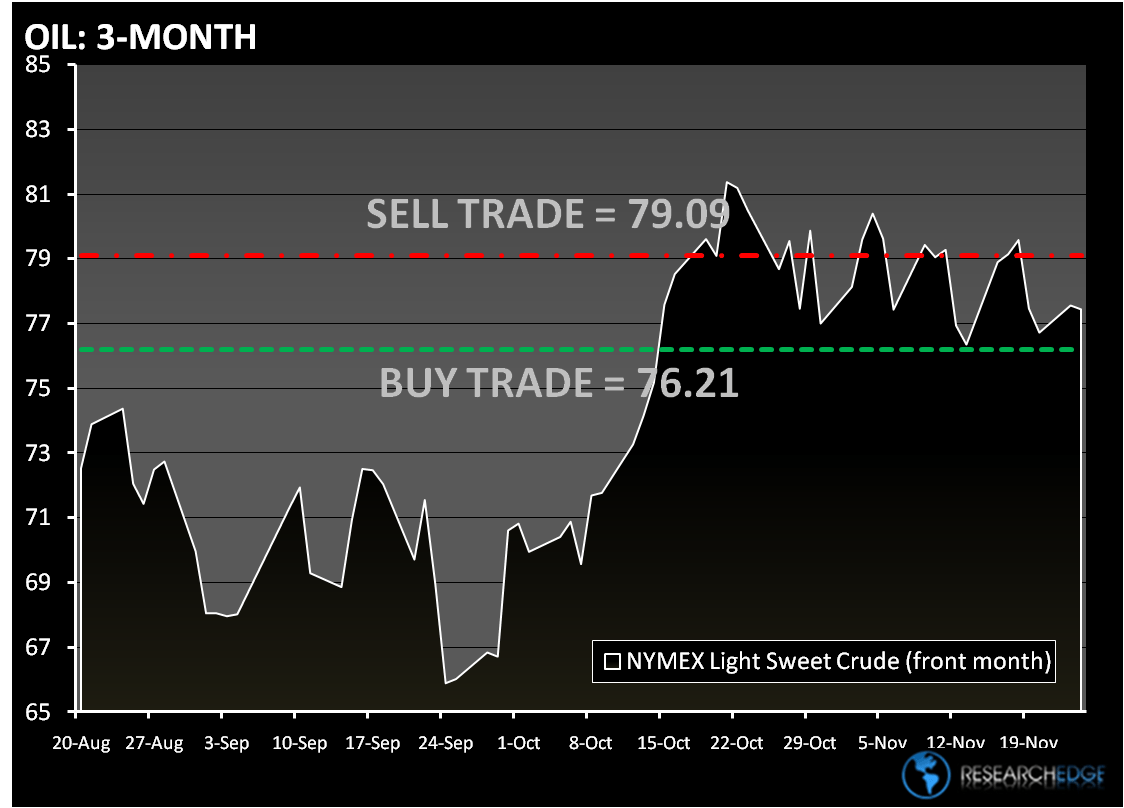

Crude oil is trading basically unchanged around $77.00 in early trading today. The U.S. Energy Department will report tomorrow that stockpiles grew by 1.5 million barrels for the week ended Nov. 20, according to a Bloomberg survey. The Research Edge Quant models have the following levels for OIL – buy Trade (76.21) and Sell Trade (79.09).

The lead story in the WSJ today – “HSBC Holdings Plc asked retail customers to remove their gold from its vaults on Fifth Avenue in New York to make room for institutional investors.” Gold rose to a record $1,170.25 an ounce in the morning “fixing” in London. The Research Edge Quant models have the following levels for GOLD – buy Trade (1,139) and Sell Trade (1,177).

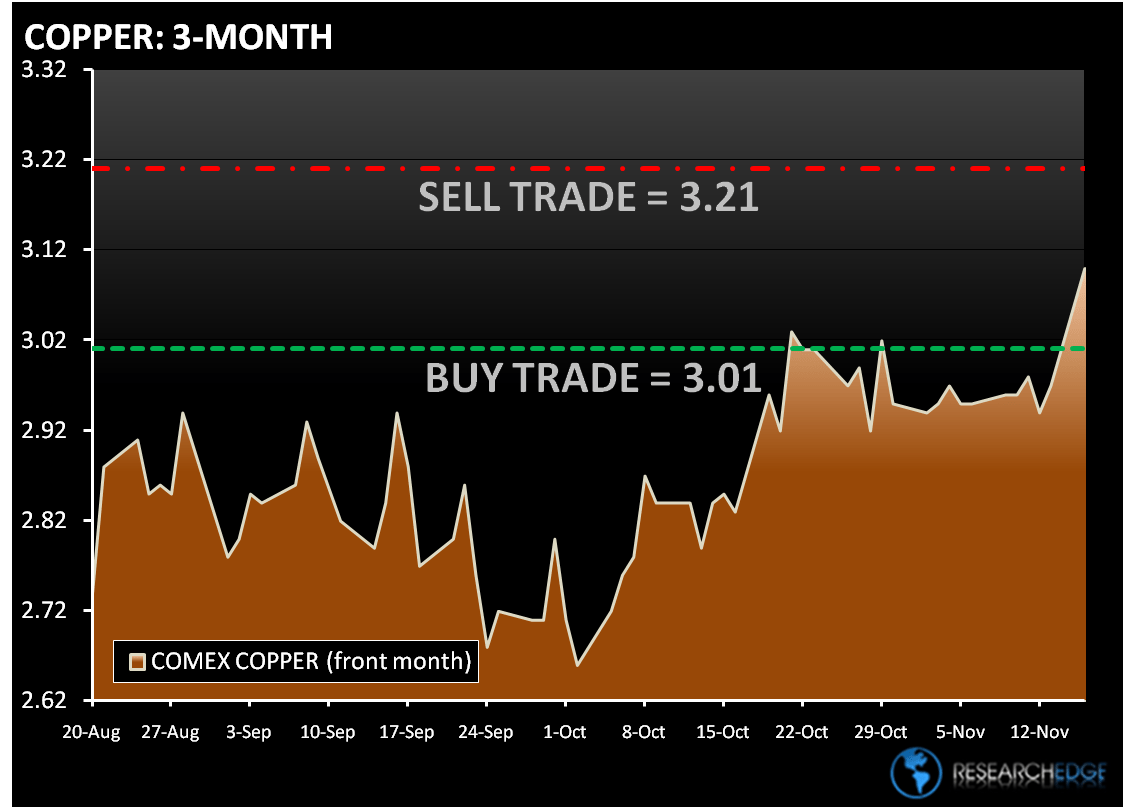

Copper fell from a 14-month high (first down day in the past three) in London as the dollar strengthened; the U.S. Dollar Index traded as high a 75.44 in early trading today. Copper for March delivery lost 0.4% percent to $3.14 a pound. The Research Edge Quant models have the following levels for COPPER – buy Trade (3.01) and Sell Trade (3.21).

Howard Penney

Managing Director