GPS: Reverting Back to a Simple One Factor Debate

At this critical time of year for all retailers, GPS has but one factor we’re keeping an eye on. The re-emergence of the Gap brand is key to the next leg of the story. Can TV and better merchandising drive positive same-store sales? We can’t be sure either way, but that’s where the debate is centered.

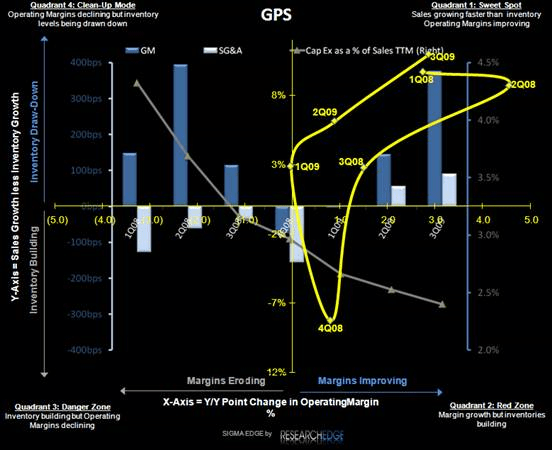

Over the past year or so we’ve gotten many questions about GPS and the sustainability of the company’s turnaround. There is no doubt along the way we underestimated management’s ability to put in place a sustainable, multi-year cost cutting plan, inventory reductions, and substantial product cost savings. Despite the profit improvements, sales have continued to decline. Although, more recently Old Navy is certainly showing signs of positive momentum.

All these efforts have resulted in a very consistent and respectable EBIT margin just shy of 12%. In the absence of any real growth (square footage is pretty much flat) and with a substantial war chest of cash (no debt) on the balance sheet of $2 billion, the company is a cash generating cow. Putting sales momentum aside, stable EBIT margins and a limited growth profile basically means GPS can produce $1.4-$1.6 billion in free cash flow annually. And while there is still some skepticism as to how long this cash flow generation and exceptional EBIT control can continue in the absence of a topline pick up, the past three years should act as a pretty good base for which to judge the limited volatility in the company’s earnings stream.

With that said, GPS is now a critical point from a sentiment standpoint. The turnaround is largely complete on the cost side. The inventories have been cut dramatically along with $700 million in SG&A expenses that are now permanently removed from the P&L. The company is moving to offense from defense. There is simply very little “addition by subtraction” left in the model, and as such investments will need to be made to drive the next leg of the story.

This is where it gets a bit less quantitative and bit more qualitative. The single biggest issue/topic/focus facing GPS the company and the shares is the ability of management to drive same-store sales back into positive territory. The recent resurgence in positive momentum at Old Navy is clearly a positive first step in the process. Merchandising, pricing, and marketing changes are all yielding positive results at a time when “value” means more to consumer than ever. The timing couldn’t be better as Old Navy regains its leadership in the world of low priced apparel/accessories sales with a fashion twist. Product cost improvements (whether it be company or market driven benefits) are allowing Old Navy to take improved profits to the bottom line while at the same time taking unit sales up. This is the ultimate recipe for success and sustained improvement, especially in the absence of a major consumer-led recovery.

But what about Gap, the brand? This is where the risk/reward lies. After years of fixing and cutting, it’s now crunch time. The next leg of the story hinges on Gap’s effort to reemerge with relevance, which will ultimately determine whether or not those comps finally turn positive. A lot is hinging on the company’s marketing plans for this holiday with the company’s return to TV for the first time in a few years. The real test here is whether the marketing message and merchandise is enough to make the brand relevant (and ultimately much more profitable) again. This is just the beginning of the process and the answer is unfortunately not known at this point. Old Navy’s recent turn suggests that there is potential here, but the brand has been losing share for years. On the risk side, these incremental marketing efforts are somewhat contained (y/y spend is forecast to be up an incremental $45 million this 4Q) which means there is no reason to be concerned that management has suddenly gone on a spending spree.

However, the real concern is what if this effort doesn’t work? Access to capital is not the problem with GPS. It’s truly the ability of Gap brand management to reinvigorate a brand that has now produced 5 years of negative same store sales in a row. I’d argue that even some moderate success is enough to keep investors interested. The leverage is substantial if productivity per foot can begin to rise again. The debate though, is now relegated to a simple one factor discussion, and unfortunately for some this debate is rooted in denim and wovens and “Holiday Cheer” and no longer in expense cutting and sourcing benefits. This makes some investors uncomfortable. Talking product is not what most investors like to do. Ask McGough if Fair Isle sweaters are in this season and you’ll see what I mean.

All eyes are on the holiday for sure. But in Gap’s case, the eyes are keenly focused on TV. November same store sales will give a glimpse of the new marketing effort’s success, but December will be the true tell tale sign. If results are positive, then there is likely a good reason to believe there are legs to the story. If it’s a huge flop, then it’s back to the drawing board for management and all eyes revert back to cash flow generation and preservation. In the near term though, there is now simply one thing to watch.