Source: Wikipedia

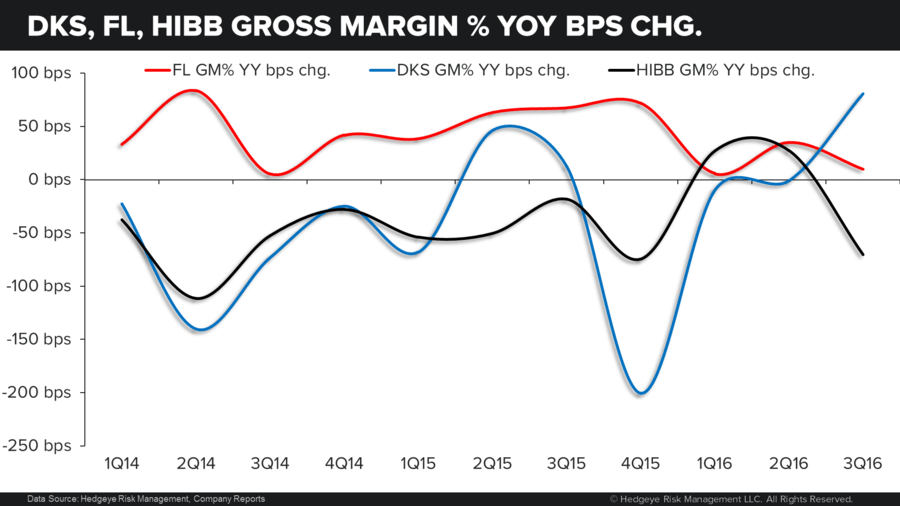

Shares of Hibbett Sports (HIBB) are down -13% today. We’ve been short Hibbett for the better part of 2-years. Sometimes with high confidence, sometimes low – but always short.

I don’t like saying that, because "perma shorts" in Retail almost never work. In other words, 2-years is a REALLY long time to be short. But expectations are consistently too high.

Last night’s miss is the second or third in a series of ‘many more’ misses barring a significant rebase in margin expectations (like coming down by another 400bp). I’d argue that this name has even more margin downside than Nordstrom (JWN).

That's because of:

- Sub-average management.

- Tapped out on store growth

- No more Wal-Mart (WMT) stores to move next to (that had been its strategy for 20 years – sell a $125 baseball bat to people who go to WMT to buy eggs).

- Moving out of core ‘bible belt’ area into regions where it has a higher cost structure because of no nearby distribution centers.

- The bull case is about 'building e-comm.' Well guess what…I’m pretty sure that it does not have ecomm because Nike told them not to. Now it’s trying to catch up to peers who have a 10-year head start. Good luck with that. That’s like ‘shopzilla’ trying to catch up to Amazon.

This is not a terminal story – there’s a definite need for it. But simply at a size 40% below where it is today, and at a margin structure nearly half of where it is today.

And, I actually don’t think this is a relevant read through to Foot Locker, the so-called basketball cycle, or whatever. It is probably not completely isolated… but this is very company specific.

I think Foot Locker (FL) is in deep deep trouble, but probably not in 1H as Nike throws it a bone to re-accelerate top line.

*Email sales@hedgeye.com for more access to and information on our institutional research.