With employment growth re-accelerating in January, Trumphoria still ubiquitous across the consumer and business sentiment surveys and the preponderance of domestic fundamental data 2nd derivative positive, it’s of little surprise that S&P 500 earnings are on pace for their strongest rate of growth since 2014.

At the halfway point in 4Q16 earnings, here are the scorecard highlights:

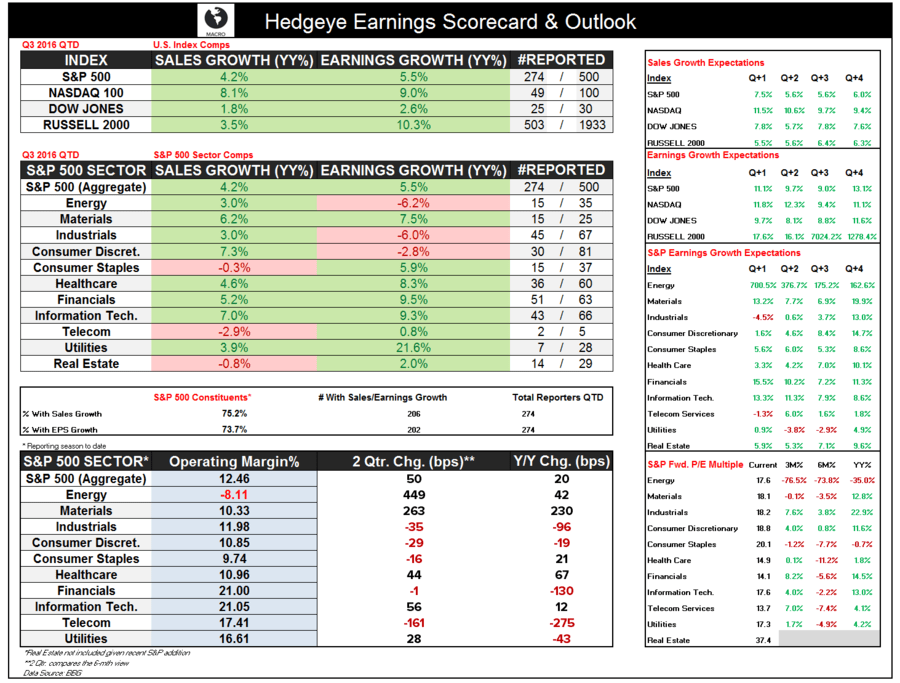

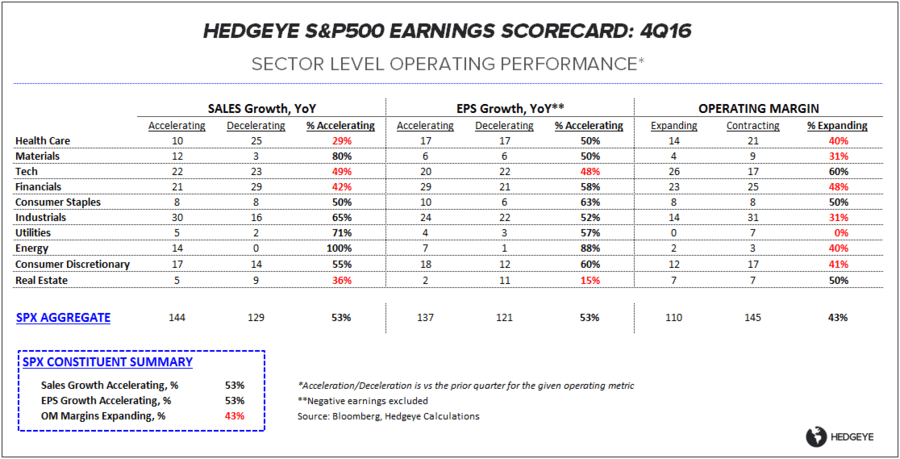

From So-So to Momo: With 274 SPX constituents having reported, aggregate sales growth is tracking +4.2% while earnings growth is running +5.5%. From an operating momentum perspective, 53 % of companies have recorded sequential accelerations in sales and earnings growth, respectively.

Looking forward, the comp tailwind in some heavily-weighted sectors should continue to be supportive of aggregate earnings growth well into 2017. The two year comp stack in the S&P 500 is still negative in the aggregate through Q4 2016 QTD results (5th consecutive quarter):

FORECASTING FAILURE: Fundamental Forecasting – particularly in terms of identifying losers – has paid nicely thus far in 4Q. 72% of companies that have missed earnings estimates have gone on to significantly underperform the market (-5.1%) over the subsequent three days. The markets treatment of Sales misses have been similar with 55% of companies missing topline estimates going on to underperform by -4.8%.

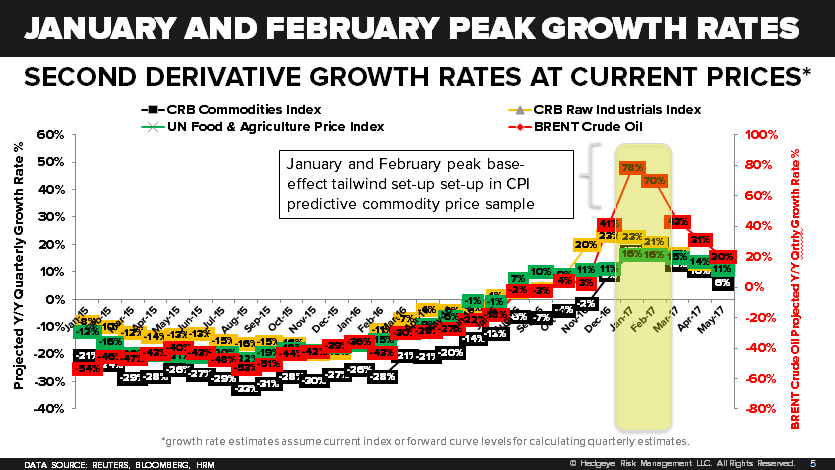

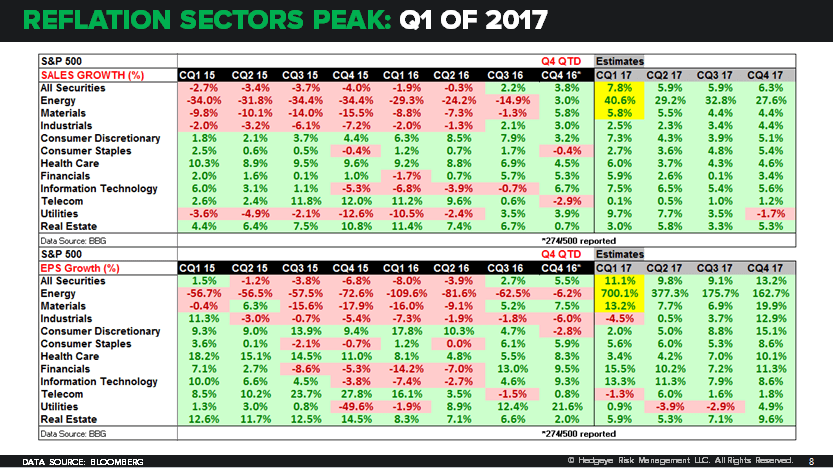

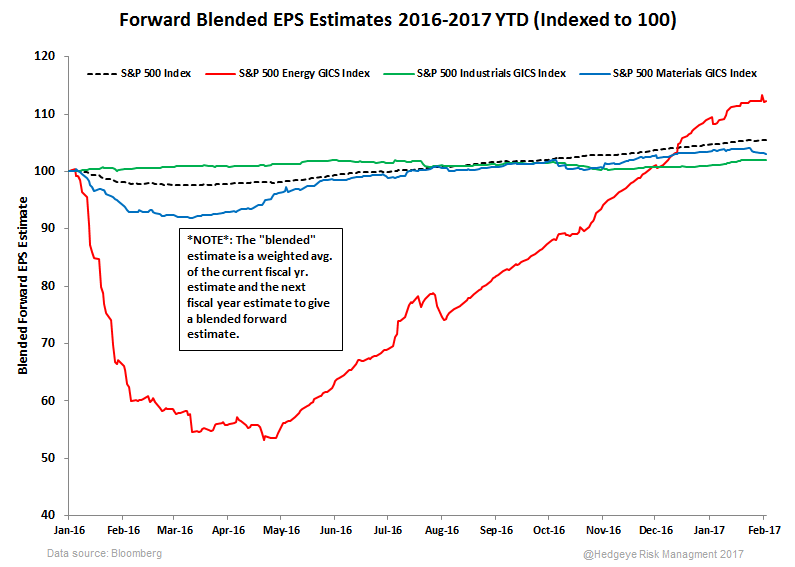

Comping the Comp: The comp tailwind for inflation-linked sectors was a key backstop to our 1Q17 Macro Theme, “Reflation’s Peak”. The growth profile across Energy and Materials is (finally) improving in 4Q against easing comps and should reflect further, significant improvement against trough comps (& sector high growth expectations) in 1Q17. While 3m/6m performance has been solid alongside the reflation tailwind, the sectors are still playing catch up to the deflationary crescendo in 1Q16.

Industrials, meanwhile, continue to comp down (-6.0% YoY), with 4Q expected to bring the negative growth streak to 7 consecutive quarters. And despite being a primary beneficiary of the Trump Trade, the group continues to carry the lowest forward growth expectations of any sector (-4.4% Y/Y in Q1 2017).

With Industrial Production and Core Capital Goods each breaking negative YoY growth streaks of 15 and 13 months, respectively, in December and global reflationary trends progressing, sector fundamentals should show progressive improvement.

Below we show the Y/Y comp tailwind for our key commodity price basket which has been a good front-runner of reported headline inflation.

Multiple Reflation: Fledgling Fundamental improvement, the step function levitation in sentiment, and the reflexive race to discount a convoluted mix of prospective policy have brough forward multiples back to cycle highs. Of course, valuation is not a macro catalyst, and expensive gets more expensive and RUST goes progressively bust when growth’s 2nd derivative holds positive.

Christian B. Drake

@HedgeyeUSA

Ben Ryan

dty