MARKET WATCH: What’s Happening? Big Tobacco comprises some seven enormous firms that use their scale and global reach to generate nearly $700 billion in cigarette sales annually. But the industry’s days of rampant YOY profit growth are numbered: Smoking rates are dropping across the globe, especially in the developed markets where Big Tobacco historically has grown its top line.

Our Take: While the entire industry faces heavy pressure in the coming decades, not all Big Tobacco companies are created equal. A few firms are primed for success in regions, from sub-Saharan Africa to the Middle East, that are poised to generate an ever-growing share of industry revenue. Others entrenched in the developed world and East Asia may be overvalued.

British American Tobacco (BTI) recently announced its intention to buy the remainder of fellow tobacco giant Reynolds American for $49 billion. (It already owns a 42% stake.)

The deal is poised to create the world’s largest company—and will add yet one more heavyweight to an already massive industry. Philip Morris (PM), worth a whopping $149 billion, owns six out of the fifteen best-selling cigarette brands worldwide. The firm has operated exclusively outside of the United States since its 2008 split from Altria Group (MO). Altria, a $138 billion behemoth, controls all PM brands (such as Marlboro) within U.S. borders. BTI (worth $115 billion) possesses a diverse global presence in regions from Western Europe to South America. Meanwhile, U.S.-based Reynolds (RAI), worth $85 billion, owns popular brands such as Camel and Pall Mall.

In recent decades, these firms have prospered. A 2014 JAMA study found that, between 1980 and 2012, the number of male daily smokers worldwide jumped up 41%—while the number of female daily smokers climbed 7%. The result has been a revenue boom for Big Tobacco: According to Euromonitor data, the total value of global cigarette sales has doubled since 2000 alone, hitting an all-time high of $698 billion in 2015.

Yet Big Tobacco is fighting growing aversion to the product it sells. More than the entire increase in the number of smokers since 1980 can be chalked up to population growth. In fact, the decades-long campaign waged by health advocates against the dangers of smoking has drastically reduced cigarette consumption rates worldwide. In 1980, 41% of men and 11% of women worldwide were daily smokers. By 2012, those shares had fallen to 31% and 6%, respectively.

WHAT’S IN STORE FOR BIG TOBACCO?

Going forward, the vast disparity in demographic and health trends playing out across the globe is poised to create unique opportunities—and risks—for Big Tobacco firms.

So what factors constitute an ideal market for Big Tobacco? Such regions share three main characteristics:

- Rising smoking prevalence

- Strong population growth

- Low- to middle-income grouping

The problem for firms is that, increasingly, regions that check all three boxes are tough to come by.

Prevalence will continue to decline in major Big Tobacco markets. Let’s first consider smoking prevalence. The high smoking rates seen today in much of Europe and Asia are projected to decline over the coming decade.

The World Health Organization (WHO)-defined Western Pacific region—which includes countries from China to the Philippines—currently has the world’s second-highest prevalence, at 25.9%. Countries in this region also register high cigarette consumption (cigarettes consumed per smoker annually). China smoked 2.5 trillion cigarettes in 2015, ten times the amount of any other nation. But by 2025, the region’s prevalence is projected to drop by more than 2 percentage points.

The decline is expected to be even steeper within the WHO European region. Nearly 28% of Europeans smoked daily in 2013, the highest share of any region. Europe also includes countries with exceptionally high rates of cigarette consumption like Russia, Kazakhstan, Greece, and Germany. European smoking prevalence is projected to fall by nearly 5 percentage points by 2025.

And the largest prevalence decline is expected to occur within the Americas. By 2025, smoking prevalence in the region is expected to drop by one-quarter, to 12%. A large component of this fall is generational. In the United States, Millennials have brought massive declines in all forms of risk-taking behavior into each age bracket they’ve occupied. Smoking is no exception: Monitoring the Future data show that in 2015, just 11 percent of U.S. high school seniors reported having smoked cigarettes during the past 30 days. That rate was 39 percent when Boomers were high school seniors in 1976—and was 37 percent when Xers occupied that age bracket in 1997.

One important thing to remember: If anything, these projections may underestimate the impending drop off. The WHO projects future prevalence based on the expected effect of current tobacco control policies; these figures do not take into account the “cohort effect” of heavy smokers aging out of the population and being replaced by younger nonsmokers (like we are seeing in the United States).

Population growth and income status create further headwinds. All of these markets become even less favorable when you consider their low and declining population growth rates.

From 2015 to 2050, U.N. population projections indicate that the European region will experience a cumulative population decline of 4%, while the Western Pacific population will grow by a miniscule 4%.

Digging deeper, many of the heaviest-smoking countries within these regions are primed for an even steeper population drop off. China’s population is projected to shrink 2% by 2050, while Russia’s population will plunge by more than 10%. These countries are tops in the world in terms of total cigarette consumption.

Moreover, the regions in which smoking prevalence is poised to decline the most and population is set to grow the slowest—the Americas, Europe, and the Western Pacific—include many of the world’s highest-ranked countries when it comes to per-capita GDP. This is more bad news for Big Tobacco, since smoking rates tend to decline fastest among high-SES population groups.

What about India? Despite a massive and growing population—together with a low prevalence rate (which allows plenty of room for growth)—India seems on a steady trend toward even less smoking in future years. Indian cigarette sales have in fact been on a downward trajectory since 2011. A far greater share of Indian tobacco consumers prefers smokeless tobacco or cheap, handmade “bidis” to traditional cigarettes.

WHAT DO THESE TRENDS MEAN FOR FIRMS?

Some Big Tobacco companies are disproportionately exposed to these regional headwinds.

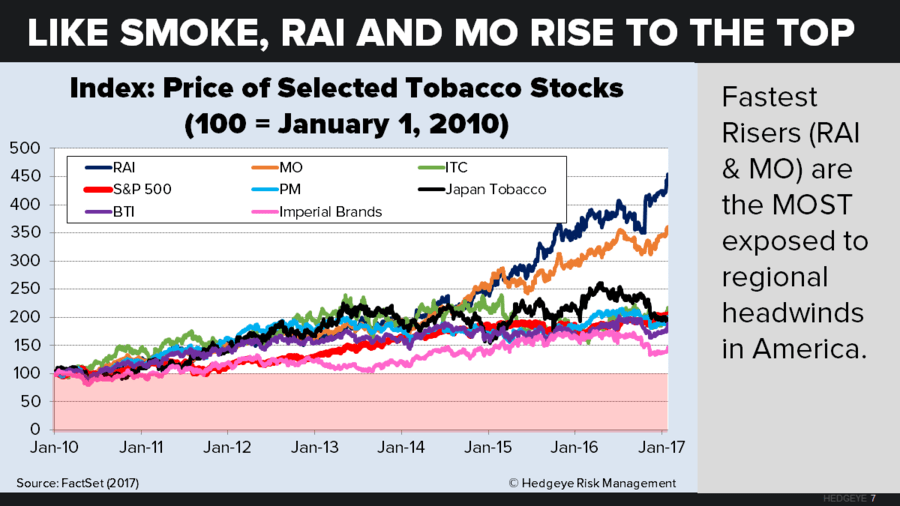

U.S.-centric firms are a risky play. In 2015, Altria earned all of its revenue within U.S. borders—yet the company still boasts an above-market P/E of 25. (Some, but not all, of this premium can be attributed to Altria’s massive scale and marketing advantages.) Reynolds too earns the vast majority (96%) of its revenue in the United States, though its P/E of 15 better reflects these risks.

The share prices of these U.S. giants are out of sync with what’s in store for them down the road. Altria and Reynolds boast by far the fastest-growing prices of any Big Tobacco company over the last few years.

Perhaps investors are betting that the two firms will succeed in their mission to bring electronic cigarettes and tobacco heating products into the mainstream. After all, Reynolds now owns four e-cigarette brands, while no other firm owns more than one. And Altria is gunning to be the first Big Tobacco company to earn the FDA’s “Modified Risk Tobacco Product” distinction for its iQOS tobacco heating device.

But significant headwinds threaten this plan of attack. Last year, the FDA expanded its definition of a tobacco product to include e-cigarettes. Starting on August 8, 2018, no e-cigarette product can remain on the market without undergoing an FDA review process that could cost $3 million per product—which, while certainly not a prohibitive cost for these giants, may cause them to reconsider the profitability of e-cigarettes.

As for tobacco burning products, it’s true that they may be safer than traditional cigarettes because they eliminate harmful constituents created during the combustion of tobacco. But non-cigarette products, whether they’re e-cigarettes or burners, generally attract only former smokers. So most of the growth that firms experience in these areas will be at the expense of their cigarette sales.

So which regions—and firms—present the most profitable future for Big Tobacco?

Africa and the Middle East check every box. Africa offers the highest projected population growth and the largest projected smoking prevalence increase of any region. Sub-Saharan population centers like Nigeria are expected to more than double in population by 2050—and low prevalence rates leave plenty of room to grow. Similarly, Northern Africa and the Middle East tout high growth projections in population and smoking prevalence.

Because incomes in Africa and the Middle East are generally so low, and because living standards here are expected to stall in the “middle-income trap,” it likely will be many decades before these regions attain the high-income status at which prevalence begins to decline. What’s more, since cigarette consumption peaks later in life within developing economies, these regions are in for a sustained cigarette boom.

So which firms are well-positioned here? BAT and PM; each earn roughly one-fifth of their revenue in Africa and the Middle East. BAT, in fact, controls 84% of the Nigerian tobacco market. PM derives 10 percent of its revenue from Indonesia. Moreover, their middle-of-the-pack P/E ratios make them highly investible.

To be sure, this industry is a long-term play. Big Tobacco has managed to find a way to keep growing its bottom line in the face of steadily declining smoking rates. It may take years, decades even, before unfavorable demographics catch up to ill-prepared firms. But if the rest of the industry cannot identify and adapt to a changing global cigarette market, some firms could eventually become acquisition fodder—or even be snuffed out altogether.