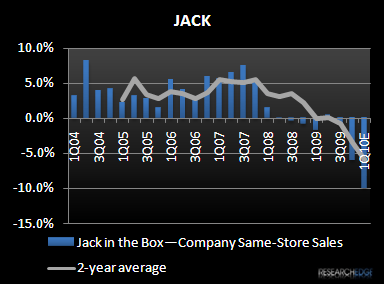

JACK’s 4Q09 6% same-store sales decline at its Jack in the Box concept came in significantly worse than my estimate, street expectations and management’s guidance of -2.5% to -4.5%. Making matters worse, trends have deteriorated further with management forecasting a 10% same-store sales decline in fiscal 1Q10 based on trends in the first seven weeks of the quarter. We have a seen significant slowdown in QSR trends, particularly at the concepts that have relatively more premium product offerings and relatively more geographic exposure to California. To that end, maybe I should not be surprised by these results, but JACK’s underperformance did shock me because trends fell off so dramatically from the prior quarter, with comparable sales declining 500 bps on a 1-year basis and 270 bps on a 2-year average basis. A -10% number in Q1 would imply another 245 bp sequential decline in 2-year average trends.

Like last quarter, management attributed the sales weakness to rising unemployment (12%-plus level in California) and increased industry discounting with the biggest fall off in trends continuing to stem from lower breakfast, side item, beverage and mid-tier priced sales. Specifically, management thinks its sales suffered from its strategic decision to go off air with its new product news as the company allocated more advertising dollars to its value offerings, which according to management, were just not compelling enough. In response to a question, management stated that BKC’s $1 double cheeseburger, which was launched nationally in October, could also be impacting JACK’s sales trends in the current quarter.

Going forward, management thinks it is extremely important to balance its advertising budget behind both its premium and value messages. In this environment, it is somewhat surprising to think that more advertising behind premium offerings would help, which is concerning because even the significantly lower same-store sales guidance for full-year 2010 of -3% to -7% assumes a sequential improvement in 2-year average trends throughout the year from current Q1 trends.

If the economic environment does not improve in the near-term, I have a hard time believing that premium offerings will drive traffic higher. According to management, being more promotional and offering an increased number of value items are not helping either. JACK was only on air with its value promotions and traffic has not improved in Q1. And, management said that significant check erosion was responsible for the sequentially worse trends quarter to date. This leaves the company in a difficult position. Increasing value at the expense of average check only makes sense if it is getting more people in the restaurant.

JACK’s full-year 2010 guidance of 15%-16% restaurant level margins implies that margins will be flat to down 100 bps YOY despite the expected 3%-7% decline in same-store sales at Jack in the Box. As I pointed out last week in reference to CKR, these operators cannot continue to hold margins (even considering current refranchising initiatives) with demand decreasing so significantly. Keep in mind that food cost favorability will moderate and go away. For reference, commodity costs were down about 5.5% in 4Q09 with beef and cheese down 17% and 31%, respectively. This level of YOY commodity favorability drove food and packaging costs as a percentage of sales down 320 bps YOY in 4Q09 and helped to push restaurant level margins 220 bps higher on a YOY basis despite the 6% decline in comparable sales. This favorable offset to declining sales will not last.