SCVL/PSS: Yet Another Family Footwear Retailer Smokes

There’s a lot of smoking going on these days in family footwear, a space we’ve favored for two quarters now. PSS is the way to play it. I am getting worried that hype is growing – but in the end it is still not in the numbers.

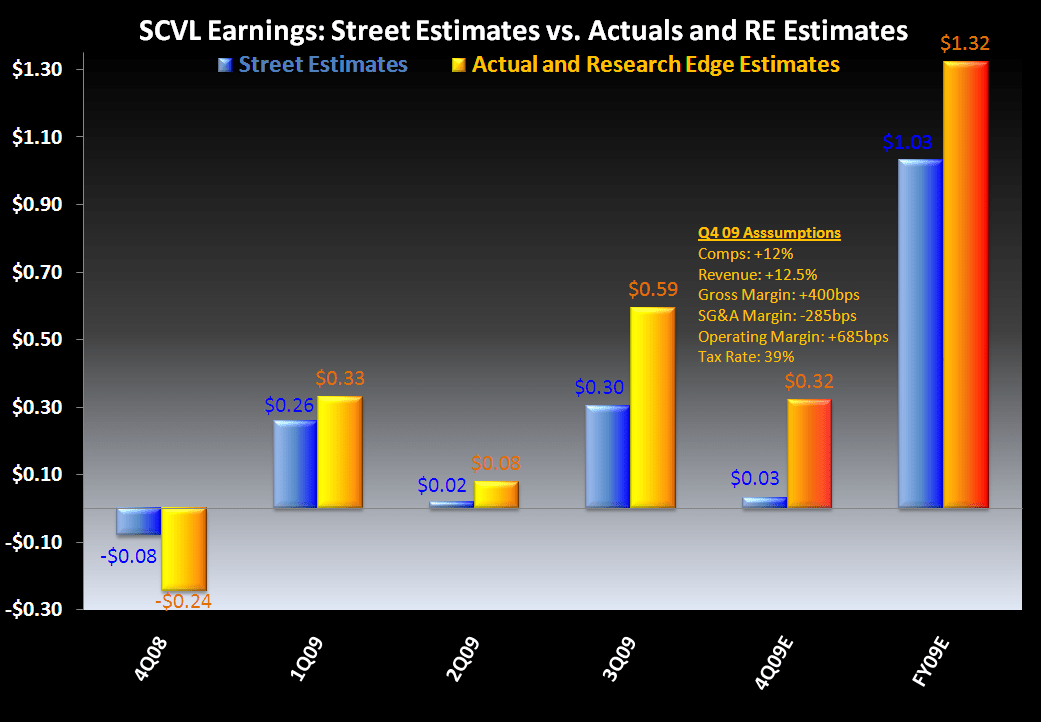

SCVL crushed the quarter on every item, lining up fundamentally to exceed the street and guidance for at least the next 2 quarters.

EPS: $0.59 vs. Street of $0.30 and Research Edge estimate of $0.40

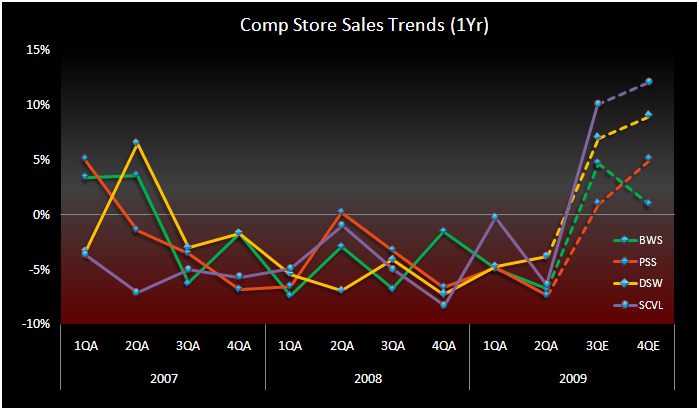

Comps were up an impressive +10%, or 2.5% on a 2-year trendline basis. Average price per pair sold was up 5.5%, footwear units sold were up 4.3%, and traffic was up 5.7%. Favorable product mix shift towards high priced footwear such as boots and athletic helped drive the comp. This represents the largest comp number in the company’s history. Comp guidance was low to mid single digit comp increases.

Revenue: +12.6%, massive sequential increase from -3.6% in Q2, 2yr jump as well.

Stores: Opened 4 stores and closed 1. Planning on closing 6 stores in 4Q, an increase of 1 store closure compared to previous guidance. Stores are working efficiently as sales per square foot grew by 11% for 3Q which was the first positive growth point since Q2 07.

Gross Margin: increased by 260bps to 29.8% compared to 27.2%.

- The merchandise margin increased 110bp primarily as a result of:

- Less clearance product (inventories +5% on 12.6% sales growth)

- Strong boot sales, which carry a higher margin.

- Buying, distribution and occupancy costs decreased 150bps, which was largely due to comp leverage.

SG&A: SG&A dollars grew by 6% but as a percent of sales fell by 150 bps, on top of a 3% decline in the year-ago quarter. The increase in SG&A was due to additional costs related to incentive compensation and employee benefits and to a lesser degree advertising and added store operational costs.

Commentary from CEO Mark Lemond: "Our large selection of value priced name brand footwear resonated well with consumers resulting in the highest third quarter comparable store sales gain in the Company’s history. We experienced higher than expected sales of athletic product during the back-to-school season and very strong boot sales later in the quarter. Our 10.2% comparable store sales gain was significantly above our expectations for a low to mid single digit comparable store sales increase for the quarter. The sales increase, combined with a higher gross profit margin and controlled expenses, resulted in our second best quarterly earnings in the Company’s history."

We’re looking at $0.32 for Q4 versus the $0.03 that the street was estimating before the results were announced.

Guidance:

Comps +3% to +5% in 4Q, which suggests -4.4% in underlying trend. CEO admitted on the call that guidance was very conservative. {note, I’ll give them the benefit of the doubt on good 4Q comps given that 3Q inventory was positive. We need to be weary of retailers whose inventory is TOO lean at end of 3Q. It there’s a snap in pos demand in holiday some companies might (ironically) be leaving money on the table.}