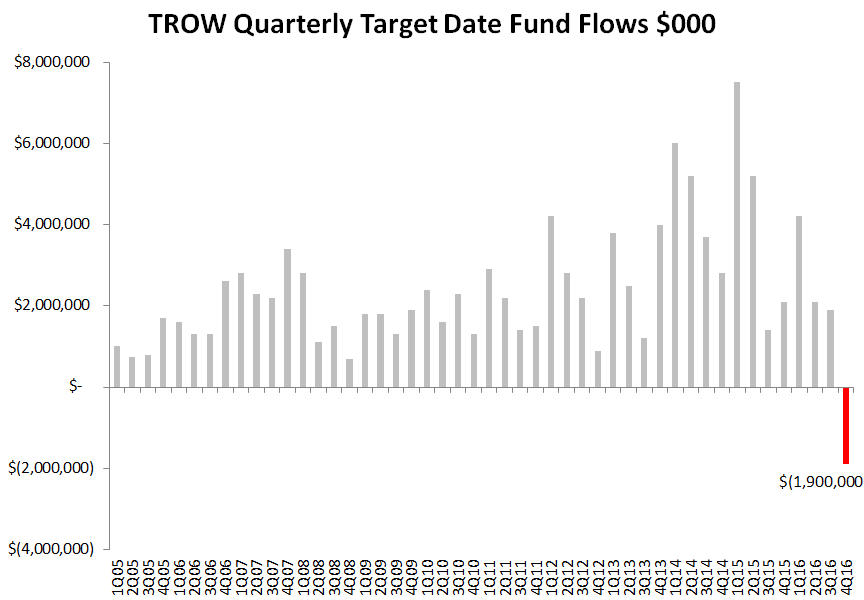

T. Rowe in its 4Q16 results put up earnings per share of $1.21 on top line revenue of $1.09 billion yesterday before the open, below Street consensus which was expecting $1.24 in EPS on $1.1 billion in revenue. The real story however outside of the slight EPS/Revenue miss was that the firm experienced its first ever quarterly redemption within its target date franchise and acknowledged substantial "headwinds" due to passives in both its core and target date businesses in its press release. While the target date business still had positive annual organic growth of $6.3 billion in all of 2016 (or a +3.8% annual organic growth rate), we believe the first quarterly redemption in the target date business will mark a turning point for TROW stock regarding its premium industry multiple and that Street consensus estimates will have several series of reductions into 2017 and 2018.

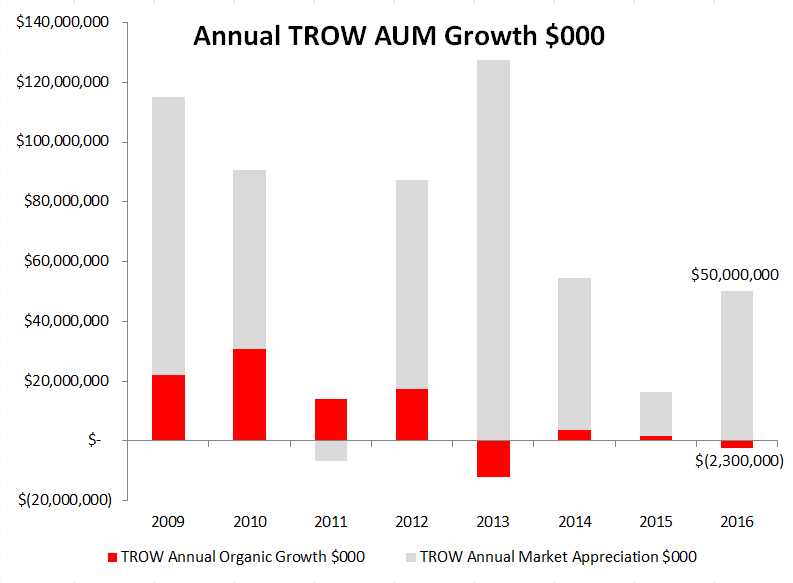

The precarious setup for TROW stock is again that the company "rode markets" in 2016 with client assets increasing by +$50.0 billion due to market appreciation versus organic growth by retail and institutional clients of -$2.3 billion. With the target date franchise now succumbing to both passive competition and also a Baby Boom investor base in net redemption within the channel, risks are increasing of earnings cuts and multiple compression. We continue to have an earnings outcome of $4.20-$4.50 for 2018, up to 20% below consensus in our probabilistic scenario. TROW continue to sit on our Best Ideas list as a Short position.

The real story within the slight revenue and earnings miss yesterday was the first redemption in the history of the firm's target date franchise:

And the firm's press release, normally a stalwart reference to the benefit of active management, was littered with references to "headwinds" and "challenges" from passives:

In our most recent Black Book we outlined that TROW has disproportionate exposure to growth in ETFs with the biggest Large Cap exposure of all the public asset managers. Large Cap is where most of passive gains are occurring:

Inroads by passives into the Target Date channel have been showing up in industry results for over a year now however TROW finally reported that it too was succumbing to passive share gains:

We are also concerned that market appreciation in this late stage Bull is the only source of client asset growth. In 2016, rising markets added $50 billion to AUM versus client redemptions of -$2.3 billion:

We continue to be cautious on the outlook for TROW earnings (and valuation). Although well run and well-resourced with $1.2 billion in cash and no debt, we have an earnings scenario up to -20% below the Street in our most Bearish outcome. TROW shares continue on our Best Ideas list as a Short position.

T. Rowe Price - Riding Markets BlackBook - December 2016

Please let us know of any questions.

Jonathan Casteleyn, CFA, CMT