Could be attractive at the lower end of the range. Risky but attractive long-term growth profile and we love the tax efficiency.

Sands China will price Thursday on the Hong Kong Stock exchange. Here are the offering details:

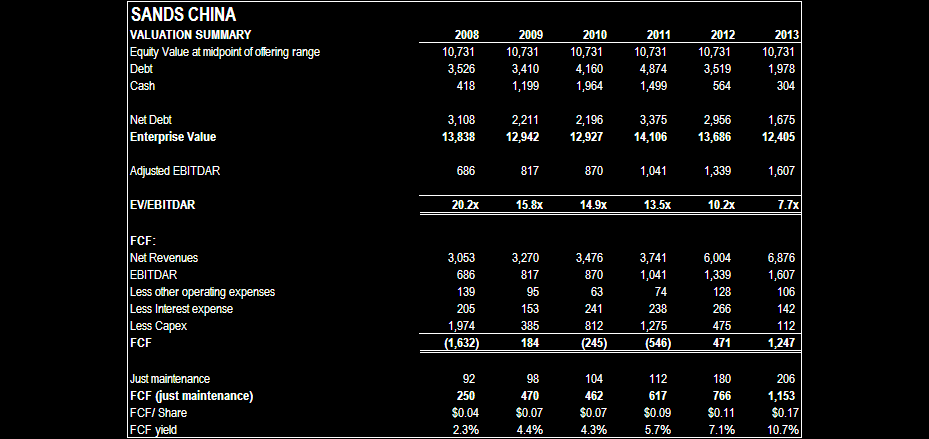

The valuation range looks reasonable, although only attractive at the $1.34 low end of the range in our opinion. Based on our numbers, the range on 2010 EV/EBITDA is 13.5-16.0x. That may look expensive but there are two major considerations. First, the net debt includes about $2 billion of capitalized costs for Lots 5&6 development without any real EBITDA contribution until 2012. We believe the initial ROI on this development will struggle to reach 10% but it does have some incremental value. Second, as we discussed in our notes on the Wynn Macau IPO, Macau does not impose a corporate income tax on gaming profits. Thus, a 16x taxed equivalent multiple is close to 10x.

To address the first point, we think it is appropriate to look out to 2012 when the first and major phase of the Lots 5&6 development will be open for a full year. The EV/EBITDA valuation on 2012 is a much more reasonable 9.5-11.0x. Relative to Wynn Macau (1128.HK), there is very little discount on 2010 and 2011. However, after giving credit for Lots 5&6 (2012 EBITDA), the Sands China discount is almost 15% from the midpoint of the offering range to Wynn Macau’s 2012 valuation. We believe that this discount is appropriate.

Here are the valuation metrics for Sands China:

The following table outlines our view of the value of Sands China. We think 2012 EBITDA deserves a 14x multiple which would take the taxed-equivalent multiple below 10x. Fair in our opinion. Discounting that back three years gives Sands China a current value of $1.51, right in the middle of the offering range of $1.34-1.79 and 13% higher than the low end of the range.