Here’s what changed this quarter…

- Stores in core region doing ok.

- Non-core regions doing worse – core to the point about moving into areas where there’s added pressure – DKS academy.

- Store closures will increase.

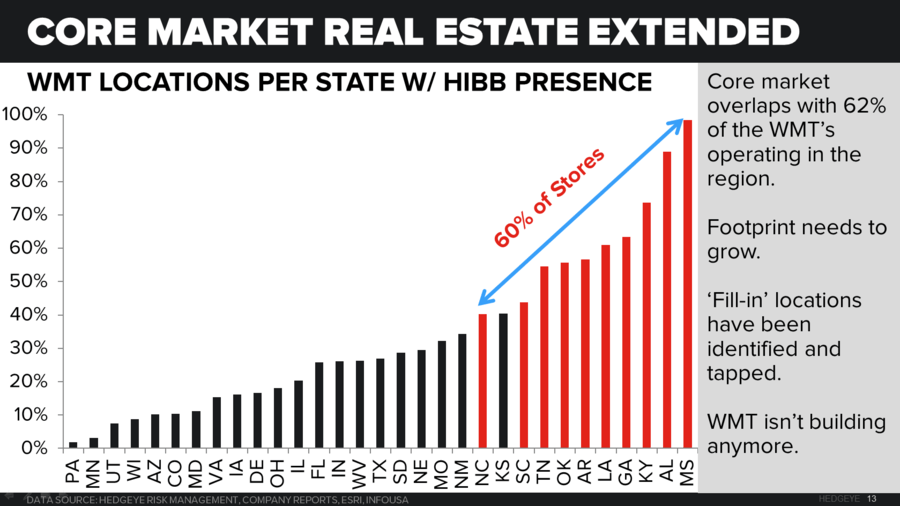

- The model has been to be near a Wal-Mart and use a weekly destination for consumers to buy a $100 baseball bat or a pair of running shoes (or anything else sports related). No more Wal-Mart’s to tap.

- Added a store in California vs the Bible/Sun belt, even though recent capex/DC was built up in home turf of Birmingham. That’s very expensive distribution with more competitive pricing dynamics.

- Talked about better pricing on sneakers – but that’s not higher ASP – it’s higher pricing dynamics for HIBB. Consider this…

- Avg price for a Nike at HIBB is $100.

- Avg price for an Adidas shoes is $70.

- The gross margin RATE is about 500bp higher when switching to an Adidas shoe. That’s bullish, but…

- Given the 40% ($30) discount to what a Nike sells for, it meaningfully pressures comp and Gross Margin dollars.

- That’s at the same time when the company needs to take SG&A higher to grow. The occupancy leverage with the old (defendable) HIBB model was a negative 1% comp – one of the few retailers with that kind of threshold. Now it’s 4-5%.

- Stores are closing, yet mix is heading towards more fashion, where it lacks a competitive advantage.

- Nevermind that this company has yet to build an e-comm platform. They hype it up that it’s coming in spring, but competition is outspending HIBB by 10x.

We think that HIBB’s earnings slide to about $1.85 over Three years, vs the Street at $3.75. We think the TREND and TAIL are both in alignment. i.e numbers in FY 2018 are 20% too high.

While the stock is still well off of the $50 level when we shorted it, it has gone the wrong way on us by 50% for the YTD. Today’s 12% correction is nice, but there’s no reason this name should not break the lows we saw in Jan. We’re still short HIBB, and will stay there until the research call changes dramatically, or the stock is in the mid-$20s.