There are a lot of reasons why we don’t like Target. It’s not because of any one factor, as most of those – at least in isolation – are known. But what is underappreciated (in a very big way) is the cumulative effect of a decade of mediocre/reckless decision making that has left the company in a difficult position – a position without the leverage to drive the business, the P&L, and cash flow going forward without eroding returns. We think this is probably in numbers for the back half of this year. But this company will have to back off of guidance and expectations, and ultimately take necessary steps (higher investment) to maintain competitive position, or else see continued top line pressure and earnings misses.

Over the near-term, the stock is off just 4% from the 2Q print when the company took down full year earnings expectations by 4%. Expectations are looking for a -1% comp deleveraging into a 3% earnings decline. Those numbers look hittable to us, hence the 9% move over the past 6 trading days. Short interest remains elevated on this one, at 7% float, just off the 5yr highs back in September. Sentiment is certainly a concern headed into hittable expectations – especially given the style factors that boosted hated-retailers last week beyond levels that are analytically justifiable. While we’re not pressing this one aggressively into the print, we’re certainly not backing off given the extremely high level of conviction we have that 2017, 2018 and 2019 expectations are too high, and that Cornell will have to meaningfully up SG&A and Capex, else lose his job.

3 things worth considering…

The Practice Schedule

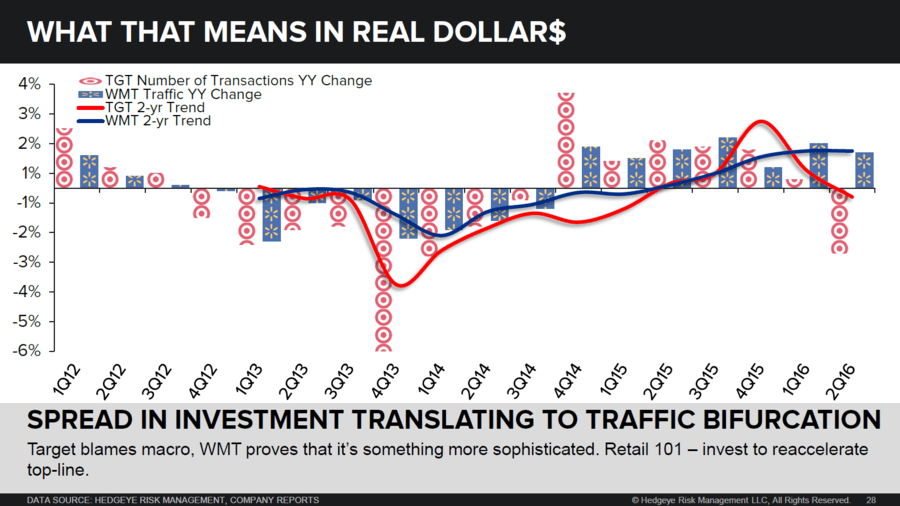

We’ve seen a huge investment spread open up between TGT and WMT. It started back in mid-2014 around the same time Cornell started his tenure in Minneapolis, and has held steady at nine-points over the past two quarters. That’s important given that Cornell is now two years into his tenure at TGT, and now has his team and strategy in place. Based on what we’ve seen to date, it can be characterized by prudent decision making when it comes to cutting Canada/Rx biz and a reluctance to spend in order to keep pace with the competition. Ultimately, we think the spread between the two needs to change dramatically – and that’s not going to be gifted to TGT from WMT as the latter company has a free pass to invest after it lowered expectations last year. That means either TGT needs to open its pockets or be content with taking what comes its way. We think it’s the prior which will be coupled with Cornell being shown the door.

The Scorecard

This is the effect and not the cause of the broader strategic decisions each team is making in order to ultimately drive traffic and win market share. There has been a clear deviation in the trend, with the spread between the two opening up to 1.2% in 1Q and 3.4% in 2Q, both in favor of Walmart. The most recent metric is good for the biggest spread we’ve seen since the TGT data breach in 4Q13, and the widest gap over the past 5 years in a normal environment. Most importantly, we don’t think this a near-term statistical aberration, as WMT is putting the dollars behind the up-tick in traffic which will continue to propel outperformance while TGT sits on the sidelines.

AMZN Not Making Things Any Easier

Today, the strategic plan for Wal-Mart vs Target vs Amazon is in the spotlight. AMZN is capturing a full 28% of incremental consumer dollars – a simply staggering number. This is closer to 40% of total online spending. On the other side you’ve got Wal-Mart, which… a) planned four years of investment in people, price, and e-commerce, and b) bought jet.com – on top of several smaller acquisitions – to build and drive its e-commerce business. In fairness, this has yet to accrue to WMT’s results. But the underlying investment is there. We’ve seen TGT underperform its original 40% e-commerce growth CAGR with the spread between WMT & TGT closing significantly in the last quarter. The punchline is TGT has a lot of dollars to invest which will ultimately lead lower margins and returns.