by Michael O'Rourke, Jones Trading

The obvious theme last week was that Donald Trump’s election victory never materialized into the market Armageddon that was widely anticipated. The macro movements in the market were stunning to say the least. The bond market had its worst week since 2013, and its second worst week since 2009. On the other hand, the Russell 2000 had its best week since 2011, and the global financial crisis before that.

In most cases, the Russell 2000 had dropped 10% or more in the preceding 1-2 weeks before a weekly 10% gain. In this case, it only dropped 4% over the previous 2 weeks. Those are just a couple of examples of the many extreme moves that occurred this week (chart below). Such a radical expectations’ reset in such a short period of time is a rarity. There is a combination of emotional and mechanized reactions in a volatile environment that has created several significant divergences which should create opportunity as volatility dies down.

In the bond market there were large amounts of money lost this week. There are several thematic concepts related to Trump’s victory being used to explain this move. We can start with foreign investors who are likely irked by Trump’s nationalist perspective and mistaken comments about debt renegotiation during the campaign.

The most bullish belief is that Trump will re-ignite economic growth, which will lead to higher interest rates. There is also speculation that a Trump Administration will be an aggressive spender, which will drive both growth and inflation. This sentiment shift is extraordinary.

The financial markets started the week absolutely confident that Trump would be negative for the economy. Within a few short days, it is now asserting that Donald Trump will succeed in creating growth and inflation, two areas where despite implementing unlimited unconventional polices, the Federal Reserve has failed for 8 years. We will be the first to assert the Fed was pursuing the wrong policies, but it is also hard to believe that Trump won’t experience opposition in implementing policy. Trump and opposition are words that go hand in hand.

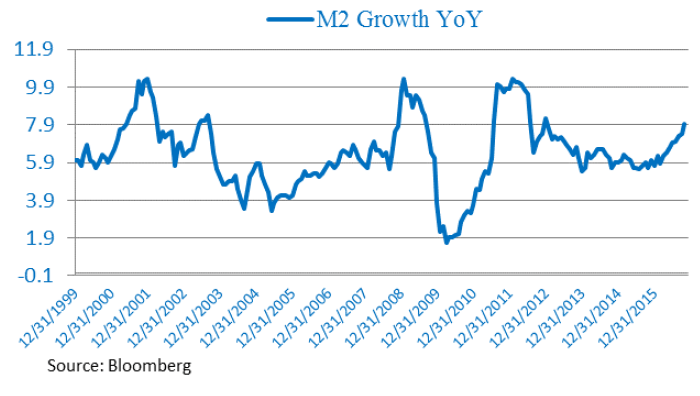

The reality is there are a couple of important constraints. M2 Money Supply has been growing very strongly all year at close to an 8% pace (chart below). That theoretically bodes well for inflation down the road, but we don’t currently have the economic momentum to see inflation pick up near term.

The S&P 500’s 1.2% post-election gain is positive, but also weak enough to be consistent with an inflationary outlook. The key exception to this thinking is the behavior of Gold, which should rise with inflation fears, but may simply be trading correlated to Treasuries.

The other key constraint to this inflationary interpretation is the Federal Fiscal Debt situation. Federal Debt to GDP is 106%, up from 63% in 2008 (chart below). While there is always the potential to pursue Japan-like strategies and go to 300% of GDP, it clearly doesn't appear to have been successful.

In short, from a fiscal perspective, there is no low hanging fruit to allow policy flexibility which will make Congressional negotiations significantly harder. The factors that are more likely to create inflation were in place before the election. While the steepening yield curve is being celebrated by Financials, the key to success there is borrowers need to come forward. Similar to the housing bubble, we have endured an extended period of time with access to cheap financing, it is more likely the back up in yields will prompt borrowers to retrench rather than increase leverage.

Bottom Line

At the moment, the economic momentum is not there to back the moves which financial markets are pricing in. It only becomes justified if Trump alone is seen as reason enough for businesses to take on additional risk, especially at higher rates. As is currently stands, most would admit Trump still represents uncertainty.

* * *

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Michael O'Rourke, Chief Market Strategist of Jones Trading, where he advises institutional investors on market developments. He publishes "The Closing Print" on a daily basis in which his primary focus is identifying short term catalysts that drive daily trading activity while addressing how they fit into the “big picture.” This piece does not necessarily reflect the opinion of Hedgeye.