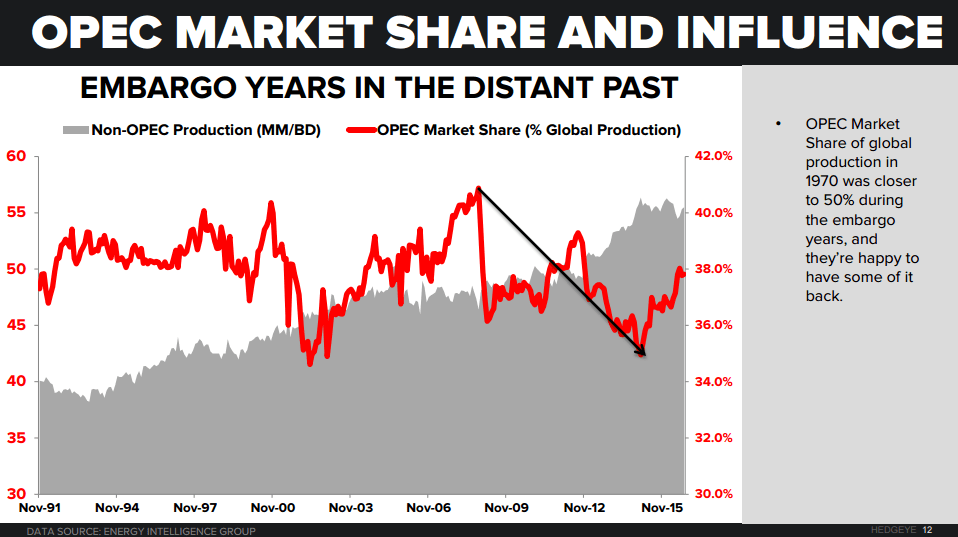

Gone are the days when OPEC controlled 50% of global oil production. The spotlight has shifted to U.S. shale among others.

That doesn’t sit well with OPEC. In an effort to break the backs of U.S. producers and maintain market share, OPEC as a whole has been pumping record levels of oil in an effort to squeeze these producers out of the market. (Fracking is a more perpetually capital-intensive extraction process and has a much higher marginal cost per barrel to pump in many regions than traditional Saudi plays)

Then came the “freeze talks.” OPEC has been talking about cutting or, at least, freezing production at current levels for some time now in an effort to boost prices. The latest oil babble is that OPEC has a “deal to agree to a deal” to freeze production at its next meeting. Make no mistake, oil-rich states like Russia and Saudi Arabia are hurting because of low oil prices, Hedgeye Commodity analyst Ben Ryan said on The Macro Show this morning. These countries have an obvious incentive to boost prices when the time is right (after more production elsewhere comes offline).

“Saudi Arabia’s economy is hurting. You’re talking about a country that receives an estimated 75% of its revenue from oil production. The oil industry contributes between 40-50% of GDP which is more than the entire private sector. The fact that oil prices have gotten absolutely crushed is meaningful. Their budget deficit relative to GDP hasn’t had this drag since the mid-80s. So to suggest that they’re fine with $40 oil is certainly not the case, but they want production to come offline more than anyone then they are more in a position to step in and talk about production cuts.”

Clearly, in the long term, higher oil prices are preferred. But until OPEC members can assert their dominance over modern, non-traditional plays on the global stage we’re skeptical this deal gets done. We’ll see.

The latest news is that Russian President Vladimir Putin – his country is not a member of OPEC – has said that should a deal be signed, Russia will freeze production too. Again, we’re skeptical of this. Russia's largest oil company, Rosneft, said yesterday it would actually increase oil production above 2015 levels. As policy analyst Joe McMonigle wrote in a research note out of the Algiers meeting at the end of September, Russia has a poor track record of cooperating with OPEC on production limits.

All of this raises an entirely different question...

Can OPEC actually control the production of its members and therefore control the direction of prices?

While OPEC sits on ~80% of global crude reserves, OPEC as a “cartel” to be reckoned with, has had virtually no impact on how much crude its members produce. OPEC sets quotas, but its member countries cheated about 96% of the time from 1982 to 2009, according to a study by Brown University professor Jeff Colgan.

A few of the more salient findings:

- OPEC announcements have an ability to move spot prices for 15 to 20 days. but there is exactly zero evidence OPEC is actually restricting output during this time

- On average, over this 1982 to 2009 period, the nine principal members produced on average 10% more oil than their quotas supposedly allowed

- The relationship between oil prices and OPEC quotas is virtually uncorrelated (r^2= 0.15)

- All but two members over-produced in more than 80% of the months during this period. The exceptions were Iran and Venezuela, which still cheated over 70% of the time

- There were 22 OPEC meetings in that same period in which quotas were increased, and in 21 cases, the new aggregate quota for the 9 principal member was lower than what those countries were producing a month prior to the change

BOTTOM LINE

Whatever OPEC members decide at their November meeting, history suggests everyone will continue to drill, baby, drill. If they still have the funds, of course.