SO THE FED SAYS THE 2016 RATE HIKE CASE HAS "STRENGTHENED." Okay, got it.

Now go flip a coin as to what they'll say tomorrow (they've flip-flopped their rate hike rhetoric 7 times in the last 10 months) particularly in light of what Fed head Janet Yellen's *favorite* economic indicator just revealed.

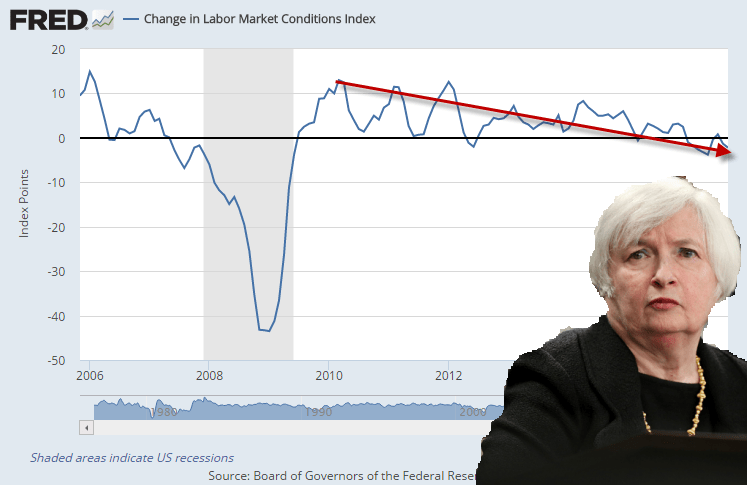

That indicator, "Change in Labor Market Conditions Index," just fell again to -2.2 for the month of September. This index has declined 8 of the last 10 months. Aside from a short-lived blip in July (a reading of 0.8), the last time the index registered positive sequential readings was back in December. Of course, that was the last time the Fed raised interest rates.

At its September meeting, the FOMC said "the labor market has continued to strengthen and growth of economic activity has picked up from the modest pace seen in the first half of this year." It will be interesting to see how continued job market weakness and slow growth filters into the Fed's rate hike calculus heading into its November and December meetings.

- Will they pull back their hawkish rhetoric ... ?

- Will they ignore economic reality and raise rates anyway ... ? (The latter would be disastrous)

Your best bet is to flip a coin with this "data dependent" Fed.