With so many distracted by their own political spew, Long Bond Bulls roar ahead by focusing on the data. One thing is clear, neither Presidential candidate will be able to change our GDP tracker which is currently at 0.4% Q/Q for Q4.

So who do you love? Do you let your politics influence how you risk manage your portfolio? I predict volatility wins into election day; immediate-term risk range for front-month VIX = 12.01-18.78. I'm staying with Long-term Bonds, Utes, Gold, and Low-Beta as a style factor.

Why?

As I've said before, there's a ton of risk that could come out of Donald Trump's mouth between now and Election Day (see video below), not to mention more causal macro considerations like earnings season and continued U.S. #GrowthSlowing.

While I'm On #growthslowing...

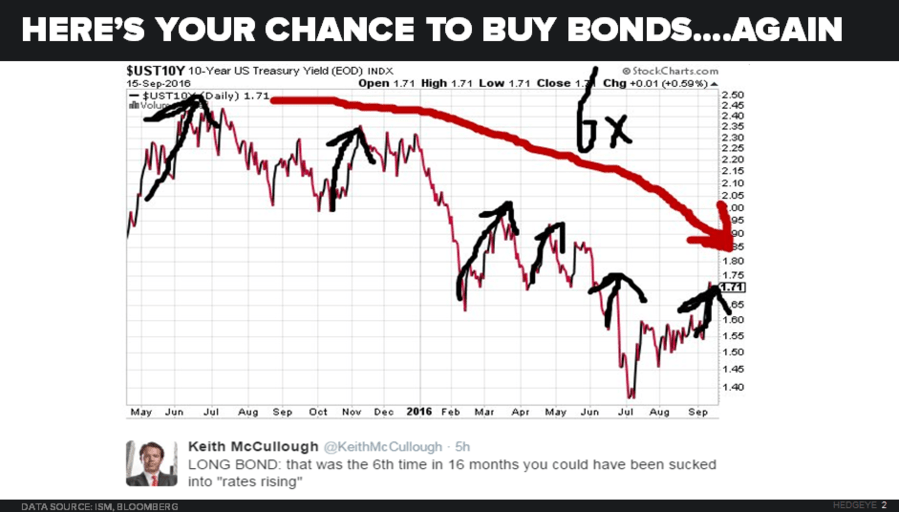

Was the pre-Fed Day hyperventilation the last big fat pitch of a buying opportunity for those who have missed #GrowthSlowing and Lower-For-Longer on rates? I think so. US Treasury 10-year yield slammed back down to 1.56%; 10s/2s spread right back to the YTD lows at 81bps and Financials (XLF) -4.4% in SEP vs. our beloved Utes (XLU) +3.2% SEP to-date.

Editor's Note: The snippet above is from a note written by Hedgeye CEO Keith McCullough and sent to subscribers this morning. Click here to learn more.