“It’s no insult to say a dead man is dead.”

-Odysseus, Troy (2004)

There have probably been 3 substantive cinematic sea changes over the last few decades.

The early 1990’s was characterized by the unlikely but epic cresting of Kevin Costner. In short succession, the mantel was passed in what has been affectionately dubbed ‘The Hanks Crescendo’ of the mid-90’s.

Then, as we moved towards the new decade, the non-Adonis leading man movement petered, giving way to Peak Pitt in the early 2000’s …. and spawning the forgettable ascent in celebrity neologism (i.e. #Brangelina) and the early transition of “attention” supplanting “money” as the root of all social media age evil.

Since our headline quote, the last decade has seen some Dicaprio gems, the Downey Jr. renaissance and the rise of the “geriaction” star, but Hollywood has mostly meandered in its unsuccessful bid to change the guard and topple the HBO model.

Over that same multi-decade period, there have been zero sea changes in monetary policy.

Lower highs and lower lows in the Fed Funds rate have characterized successive economic cycles for the last 35 years as policy makers have Doved Slowly in their attempt to simultaneously and successively stimulate and drive debt service costs lower while marching the debt/interest rate cycle to its terminal end.

You can’t blame them really, the waters of academic economic theory are deep but, practically, active policy is about as shallow as a puddle.

The conventional theory, depicted in the chart below, is that the level of output drives inflation which, in turn, drives the policy response in a circular, counter-clockwise inflation-output loop.

As we’ve highlighted, these output-inflation cycles were the prevailing macro reality when Janet et al. were coming of age and conventional monetary policy is designed to function within the context of this (formerly) archetypical cycle.

In practice, conventional policy is predicated on manipulating the (real) interest rate to drive changes in interest rate sensitive investment and consumption and for the flow through impacts to the currency to shift net external demand.

That’s pretty much it.

It’s no insult to say a broken model is broken.

Back to the Central Bank Observation Grind…

Policy makers don’t always “judge that the case for an increase in the federal funds rate has strengthened”, but when they do, they simultaneously lower their growth, inflation and neutral interest rate forecasts to their lowest levels ever.

In terms of summarizing yesterday’s Fed action, that’s pretty much it.

The market’s reaction to the latest iteration of the Fed’s When In Doubt, Dove It Out bias was unsurprising:

Dovish => Dollar ↓ => Reflation ↑ = Gold/Utilities/Bonds Outperform, commodity reflation ↑, Financials underperform => slower-and-lower-for-longer remains the prevailing fundamental and policy outlook reality.

Much of the pre and post-conference punditry centered on how 2016 parallels 2015 with rising market angst into a no-go September decision with the stage set for a highly probable December hike.

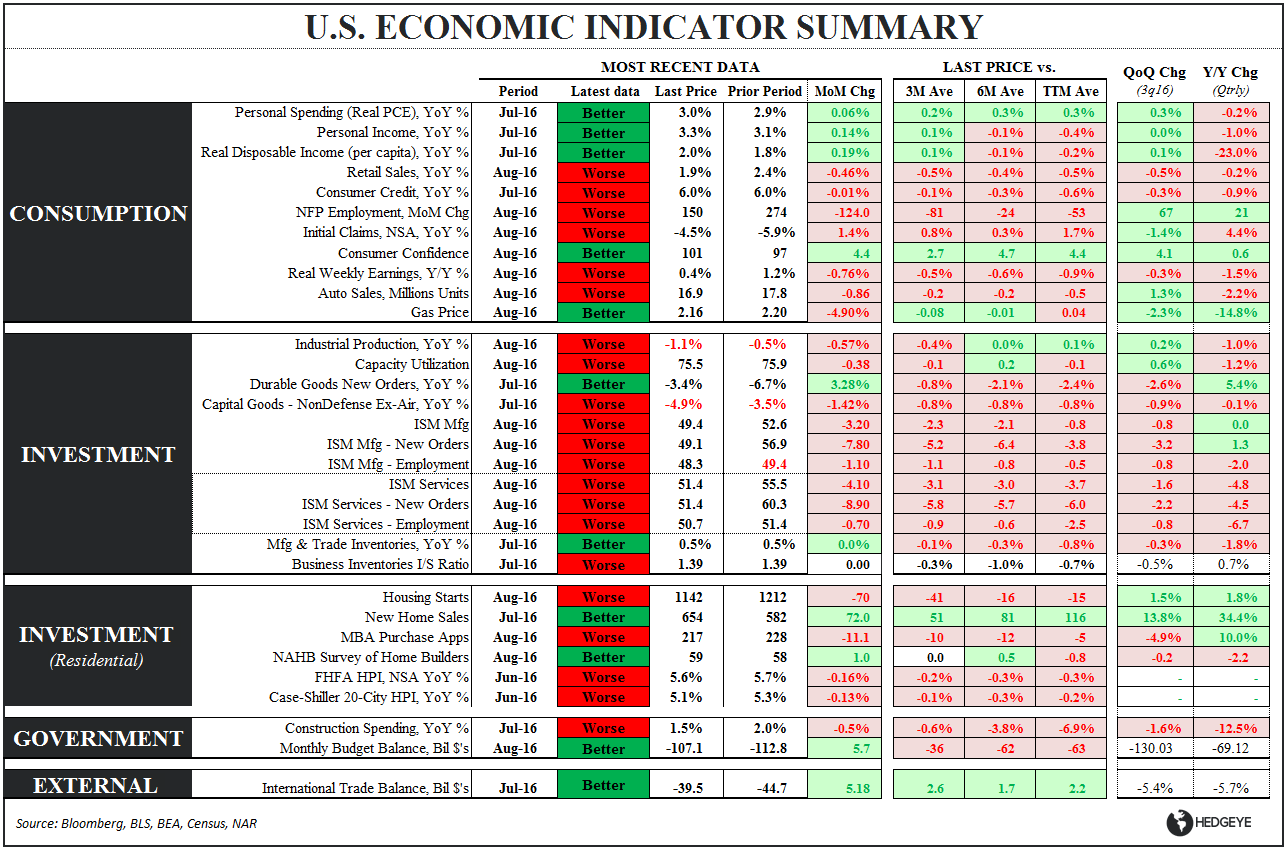

Since December is both the main talking point and the lone comp – and because Janet repeatedly highlighted the strengthening economy – let’s juxtapose current domestic macro conditions with those from December of last year.

The “improvement” is given by the delta at the far right of each series:

- TTM GDP, YoY: Dec 15 = +2.6%, Current = +1.7%, chg = -0.90%

- NFP Absolute, TTM: Dec ’15 = 230K/mo, Current = 200K/mo , chg = -30K

- NFP growth, YoY: Dec ’15 = 1.95%, Current = 1.72%, chg = -0.23%

- Aggregate Hours Growth, YoY (6-mo avg): Dec ’15 = +2.28%, Current = +1.56%, chg = -0.72%

- Labor Market Conditions Index (6-mo avg): Dec ’15 = +2.2, Current = -1.5, chg = -3.7 pts

- Aggregate Income Growth, YoY: Dec ’15 = +5.8%, Current = +4.3%, chg = -1.5%

- Consumer Credit Growth, YoY TTM: Dec ’15 = 7%, Current = 6.5%, chg = -0.5%

- Pending Home Sales, YoY TTM: Dec ’15 = +7.6%, Current = +2.4%, chg = -5.2%

- Housing Starts: Dec ’15 = 1160K, Current = 1142K, chg = -1.6%

- Auto Sales: Dec ’15 = 17.4M, Current = 16.9M, chg = -3%

- ISM Services: Dec ’15 = 55.8, Current = 51.4, chg = -4.4 pts

- ISM Mfg: Dec ’15 = 48, Current = 49.4, chg = +1.4 pts

- SPX Margins: Dec ’15 = 12.25%, Current = 11.9%, chg = -0.35%

- Capex Orders: Dec ’15 = 2 consecutive months of negative YoY growth, Current = 9 consecutive months of negative YoY growth with negative growth in 18 of the last 19 months

- Industrial Production: Dec ’15 = 4 consecutive months of negative YoY growth, Current = 12 consecutive months of negative YoY growth

- Productivity Growth, YoY: Dec ’15 = +0.4%, Current = -0.4% and in the midst of the worst streak of productivity growth in 4 decades.

It’s no insult (or unpatriotic) to say that a negative second derivative is negative.

I’m tempted to take the rest of the day off because if I hear “hawkish hold” one more time my brain may collapse in on itself in a kind of meme du jour supernova.

Anyway, the net of yesterday is that the late-cycle macro reality and the associated allocations we’ve been espousing for the last year continue to find confirmation in both the data and negative revisions to the forward outlook.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.55-1.72%

SPX 2116-2171

Nikkei 162

VIX 13.03-19.02

USD 94.60-96.31

Gold 1

To Brangelina, may it RIP.

Christian B. Drake

U.S. Macro analyst