Lululemon opened up a new 10,000 foot Queens West store with a café, a juice bar, a lounge a ‘brainstorming area’ and other features dedicated to not generating revenue. This is yet another reminder about why this is in our top three best short ideas (behind HBI and TGT). Here’s the read on TTT…

TAIL

Great brand, but run by an incredibly weak management team that is being carried by the strength of a category. No viable strategic plan. Unit growth in North America is slowing dramatically. Incremental square footage is coming in the form of bigger stores, and unit growth in places like Albany instead of Orange County, NYC or Buckhead. Growing overseas in more expensive markets at margins that are still and will be dilutive for the foreseeable future. Ivviva (lulu for tweens) is good, but the costs associated with the brand are the same (real estate, marketing and product development) and yet the prices are 20% less than lululemon. Men’s business is definitely viable, but again, carving space away from the women’s business only can go so far. LULU is in desperate need of a wholesale model, as they need to sell product where people shop. Believe it or not, people do actually shop at multi-line stores. That will be expensive as LULU is not invested in making that work. It will take far more sophisticated product differentiation, including sub brands – which will require new development and design and marketing triads inside the organization. Focusing on delivering on a low-50s gross margin won’t get shareholders or this management team paid. Again, this is a stellar brand, and it’s a shame that the team running it did not have a better vision and the ability to execute. There’s easily $4 in EPS power, which could make this a $100+ stock. We just don’t think we’ll ever see it without taking EPS below $2 and changing up management first.

TREND

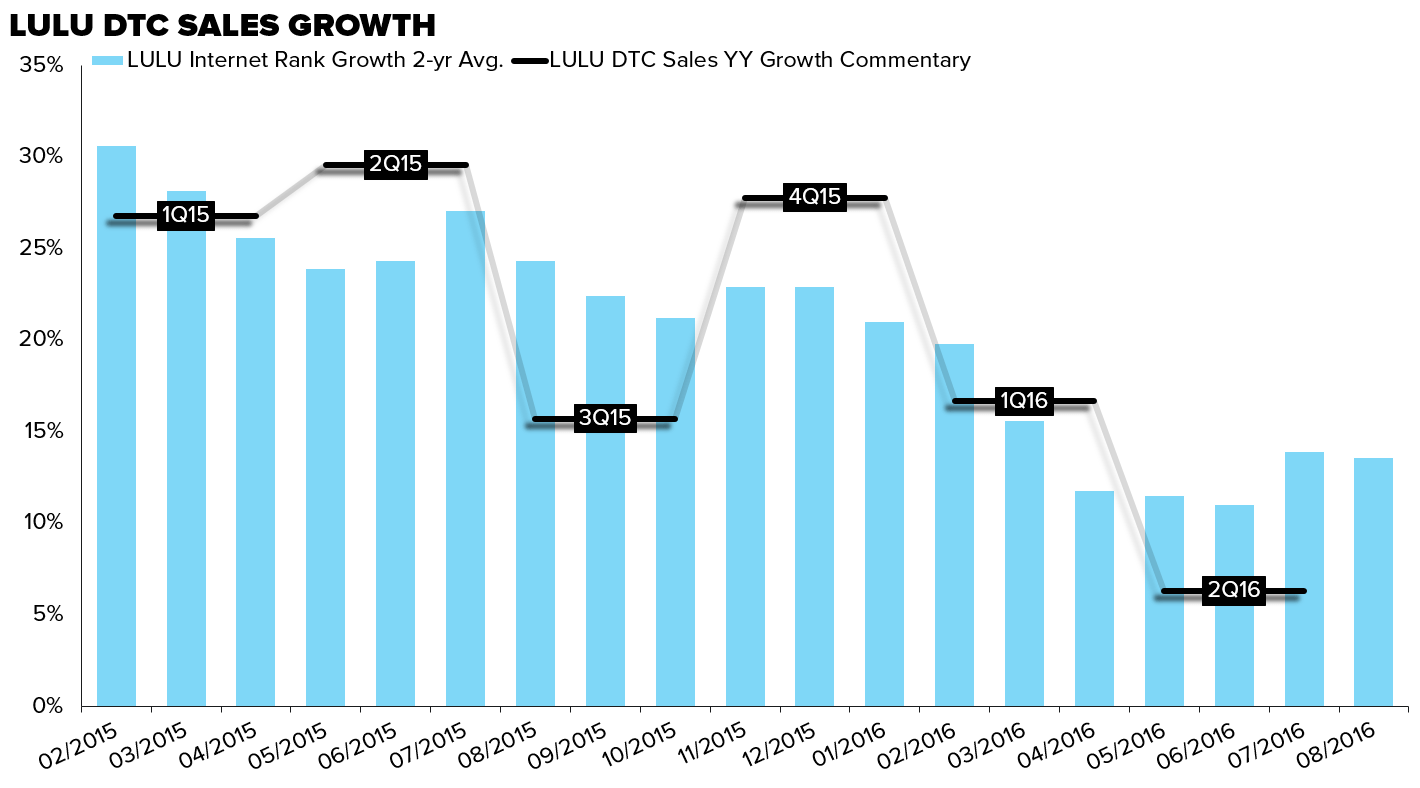

1) Revenue. Traffic continues to be a headwind, going negative in 2Q and persisting into 3Q. Pricing and UPT have done enough to offset the negative traffic growth, but the company is now comping against the pricing hikes from the pants wall refresh, by our math the average price of a SKU was up 6% in 2H15. E-commerce put up its worst growth rate in LULU’s history at 6% – which was conveniently explained away by the anniversary of an online warehouse sale which was good for 10% points of DTC comp. No matter which way we slice it, the 6% of 16% DTC comp continued the decelerating trend we’ve seen unfold in the first half of 2016. Looking ahead to the back half of the year, top-line compare remain just as difficult at 9% in 3Q and 11% in 4Q.

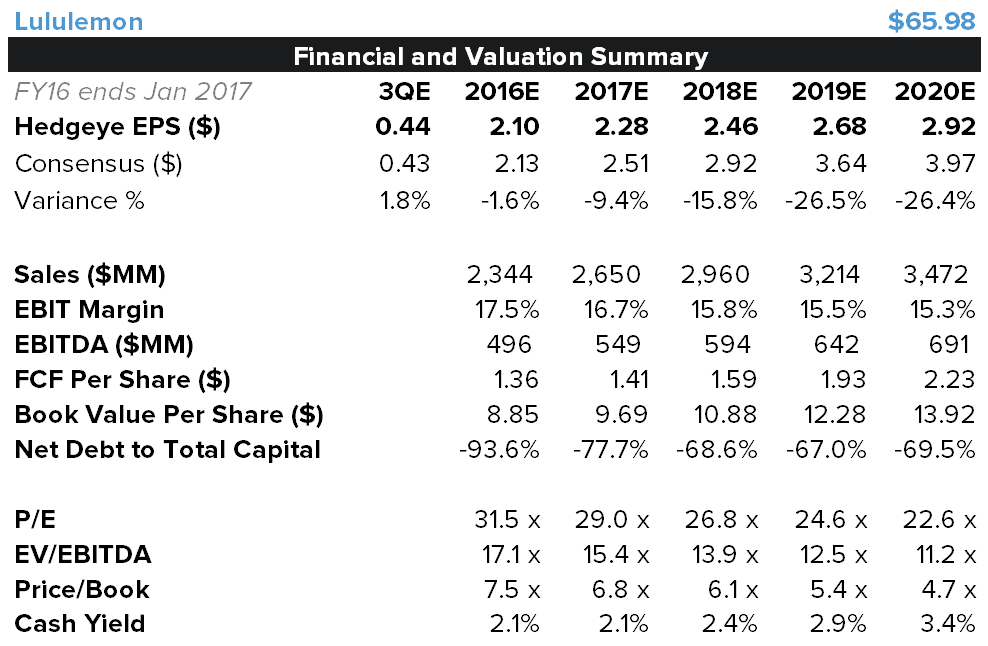

2) Margins. Gross margin came in 120bps ahead of expectations in 2Q16, good for 260bps of expansion YY. That’s in consensus numbers for the balance of the year, with consensus looking for ~250bps of GM expansion in the back half. Incremental margin after nearly 2yrs of negative growth turned positive at 4%, with the expectation that it tracks towards 24% by 4Q16. Gross margin expansion will be the main driver of that, though we think that incremental expenses in the form of business mix away from core NA lululemon towards ivivvia and international (which will account for the majority of new unit growth for the first time in the company’s history) will understate EBIT margin expansion. We’re a couple pennies below the street for FY16, with the delta between Hedgeye numbers and current Street expectations opening up to 10% next year.

TRADE

Incremental e-comm datapoints point negative. If there was only one datapoint that speaks to the incremental health of the brand, it is e-comm. Expectations call for a pop in incremental margin going from 3.8% in 2Q to 24% within three quarters. That’s in expectations already, and is clearly in the multiple – at 29x earnings and 15x EBITDA. We don’t know what type of investor is the incremental buyer here, as buying it at $69 probably means that you have to believe it’s going over $80 – which we simply cannot justify based on what the model is telling us. All in, we simply think there are more ways to win on the short side than on the long side.