Below are analyst updates on our thirteen current high conviction long and short ideas and Hedgeye CEO Keith McCullough's refreshed levels for each.

Please note that we added Cerner (CERN) and Copper (JJC) to the short side this week and removed Lazard (LAZ). We removed Lockheed Martin (LMT) from the long side. We will be sending stock updates from our analysts on Whole Foods, Cerner and HCA Holdings in the coming week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

LVS

Click here to read our analyst's original report.

As expected, September is off to a slow start, at least when compared to the seasonally strong August and a relatively difficult comparison.

However, comps ease considerably and The Parisian opening tomorrow should provide a base mass boost. Thus, we expect September to end flattish on a YoY GGR basis while the Hedgeye Mass Tracker suggests mass revenues could grow 5-7%, besting Q2’s surprisingly strong 4.6% growth. Accelerating mass growth drives the basis for our positive Macau thesis with LVS as the primary horse on the long side.

We would take advantage of and pending volatility to add to the Las Vegas Sands long position.

Note: Shares of LVS are up over +11% since we added it on 8/26/2016.

EXPE

Click here to read our analyst's original report.

Analysts Todd Jordan and Hesham Shaaban reiterate their long thesis on Expedia. They have no new update this week. We continue to like the set up for the remainder of the year and look forward to providing additional analysis as we near quarter end.

TLT | GLD | MUB | VYM | JJC

To view our analyst's original report on Gold click here.

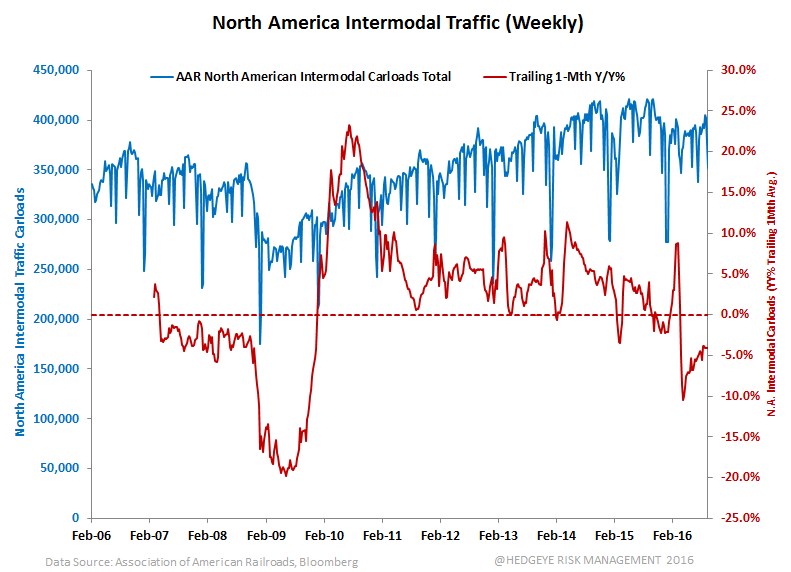

We added Copper to the short-side of Investing Ideas on Friday following additonal confirmation that the manufacturing side of the economy is stuck in a month’s long lull. Industrial production declined for the 12th consecutive month, -1.1% Y/Y in August. Durable goods ex. defense and aircraft and capital goods orders ex. defense & aircraft declined -1.6% (4th consecutive month) and -4.6% (9th consecutive month) respectively. In addition to the copper mining equipment shipments chart immediately below, we get in the weeds on the carnage in intermodal and freight traffic in North America. We’ll take a bounce in copper as a good entry point to re-short the long-term deflation of the Bernanke commodity bubble.

Below is a long-term chart of the 6 times in the last 16 months we’ve gotten to buy long-term Treasury bonds.

The relevant domestic data reported this week (in no particular order) was CPI, PPI, retail sales, and industrial production among other things.

In short, CPI picked up both sequentially and Y/Y in August (+1.1% vs. +0.8%). PPI printed a flat +0.0% Y/Y for August which was a slight acceleration from -0.2% Y/Y. One of the key call-outs embedded in the CPI number is the sharp increase in medical care costs. Medical costs increased a full 1% from July to August to +4.91% Y/Y which is the fastest pace since January 2008 – so the little inflation that can be seen is not at all friendly to the consumer.

Retail sales most likely won’t provide nearly the boost to Q3 GDP that it did in Q2 when it was a significant positive contributor. The control group of the retail sales report (the GDP input) declined -0.1% M/M and came in at +2.8% Y/Y and +0.8% quarter over quarter (annualized) for the first two months of Q3 vs. Q2. In Q2, this number was +6.1% through the first two quarters.

The weakness on the manufacturing side of the economy has now been consistent for over a year. Industrial production came in at -1.1% Y/Y, the 12th consecutive month of contraction. Capacity utilization printed -1.2% Y/Y, the 18th consecutive month of contraction. To get more in the weeds on the weakness in capital intensive industries, below we show charts of freight and intermodal traffic from the American Association of Railroads. The data comes weekly, so it’s a good real-time look – the red line shows Y/Y changes:

- Total traffic -7.1% Y/Y

- Intermodal traffic -3.1% Y/Y

- Total carloads -11.0% Y/Y

Bottom Line

We continue to observe that growth is slowing in aggregate. We continue to like bonds (TLT, MUB) and bond proxies (VYM). On the inflation front, comps get much easier moving forward (we’ve been in a deflationary environment for 2 years!). Our GDP estimates for Q3 and Q4 are below the street and Central Bank forecasts. For the full-year, we’re well below at +1.2% Y/Y vs. the Fed at 2.0%. If these estimates converge, we expect it to be dovish on the margin when coupled with our bearish rates view. The inflation comps effect and a policy catalyst are shaping our fundamental views of a longer term gold position (GLD).

HBI

Click here to read our analyst's original report.

What many people fail to fully appreciate is that e-commerce is accelerating off of a larger base. Consider this: online stores/marketplaces (think Amazon, Wayfair, etsy and even eBay) gained 263 basis points in share of retail sales over the past three years. That’s pretty huge given that it came off a base of only 7.6%. Keep in mind that the 180bps lost by a category like GAFO (General Merchandise, Clothing, Electronics, Home, etc) actually includes its own e-commerce sales. In other words, the share loss to online on the part of Kohl’s and Target came despite all their talk of growth opportunity in e-commerce when they are working the one-on-one circuit.

Here’s the kicker – of the 263 basis points in share gain for e-commerce, 177bps of it came over the past 12 months. That sentence might be worth rereading. It’s huge. And I can assure you that no self-respecting brick & mortar CEO is taking about that. Those that are probably are on their way our [case in point – Hanesbrands CEO has 16 days left on the job.

This stock remains out top short in Retail.

WAB

Click here to read our analyst's original report.

While shares of Wabtec have quietly moved higher since the 2Q16 earnings disappointment, we think the storm should come for longs with the October 20th 3Q 16 earning release.

With higher raw material costs, weak demand for rail equipment, and ongoing pressure in resource markets, we expect WAB’s margins to disappoint investors. In addition, we should get a "make or break" update on the Faiveley merger, which currently serves as the latest stop in the bull case “thesis drift”. Short of a pre-announcement on either the merger or earnings, volatility should be tame until a bit pre-Halloween uncertainty.

We continue to expect WAB’s market to decline and for shares of WAB to follow.

cern | AHS | HCA

Click here to read our stock report on AMN Healthcare Services (AHS).

Our Healthcare team reiterates his high conviction short ideas. No new updates. We will be sending two stock reports next week on Cerner and HCA.