Editor's Note: This is an excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

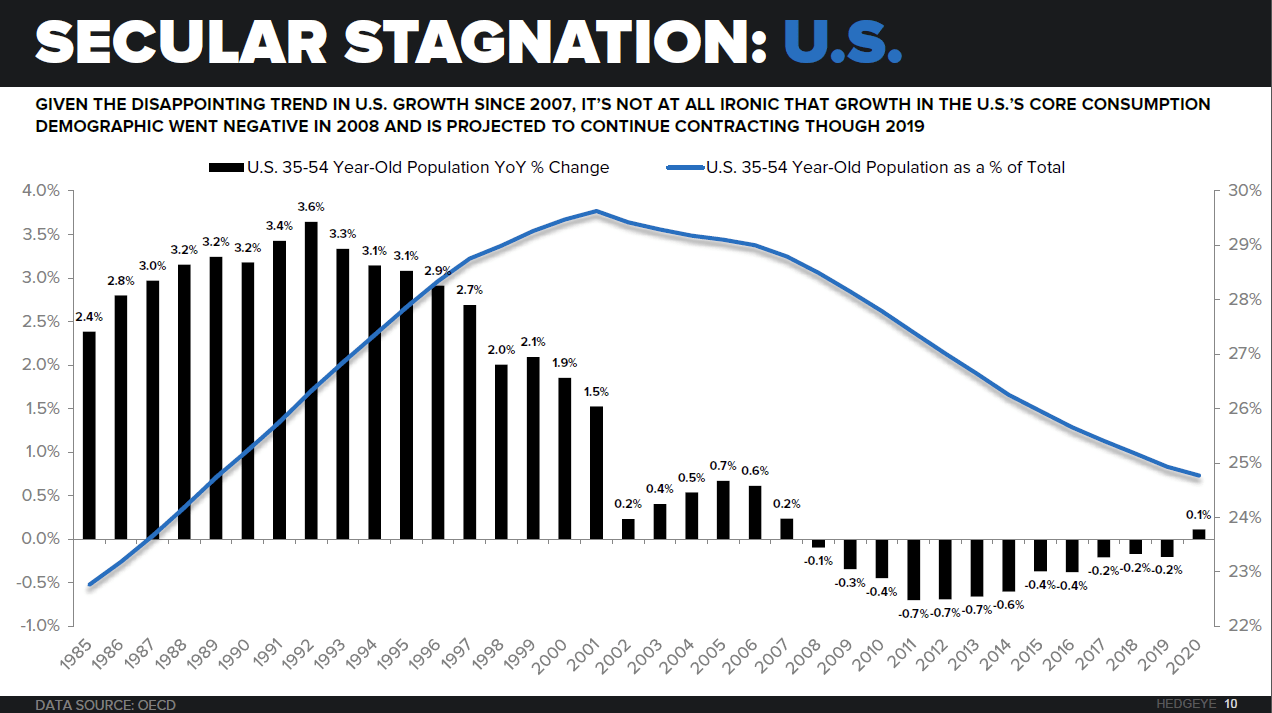

If you don’t get that Demographics is the #1 causal factor on slower and lower for longer, you’re definitely not reading Hedgeye’s Demography Research (see Chart of The Day for details on the rate of change in growth for the 35-54 year old US population).