Small Businesses represent ~99% of total U.S. Employer firms, ~50% of total Private Sector Employment and ~60% of net private sector hiring on a monthly basis.

While a fair amount of air time has been given to the post-crisis retreat in entrepreneurship and business creation, the trend in small business hiring, confidence and investment spending remains critical to aggregate trends in employment and economic activity. In short, it still matters.

That’s the contextual preface, here’s a quick update and some rumination on this morning’s August data:

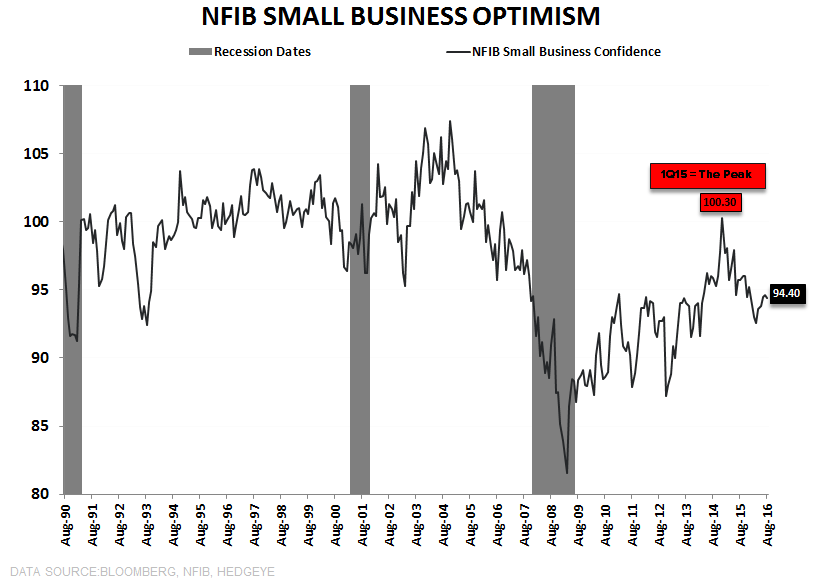

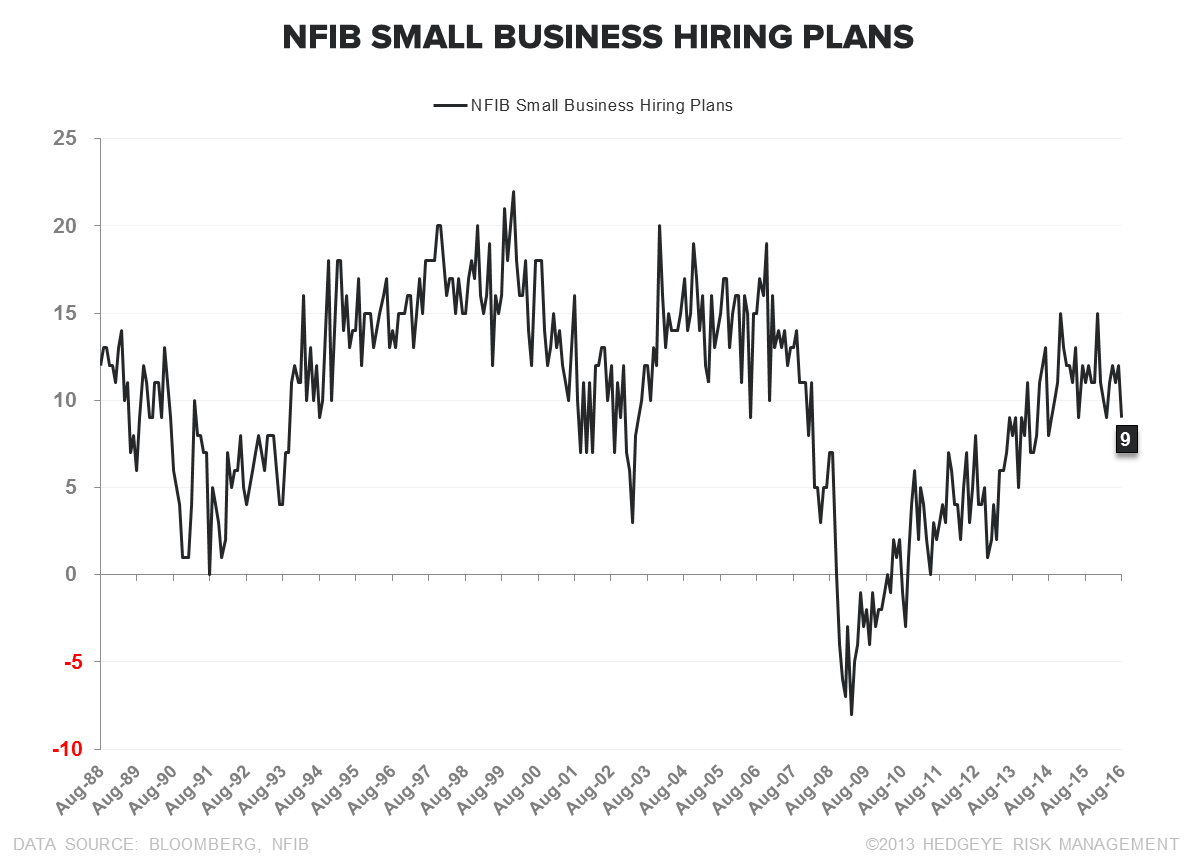

1Q15 = The Peak: Small Business Optimism fell -0.2 pts sequentially August with Hiring Plans (-3pts), Outlook for Business Conditions (-7 pts) and Sales Expectations (-2pts) leading the retreat.

While the YTD trend has been muted and largely uneventful – oscillating in a 2-pt range between 92.5-94.5 – the larger Trend has been one of conspicuous slowdown. As the first 3 charts below illustrate, Business and Consumer Confidence both peaked concurrently in 1Q15 and have subsequently failed to breach to new highs.

As we’ve highlighted, when viewed in the context of the temporal procession of macro fundamentals, the peaks in consumer and business confidence come as little surprise:

2H14: Income Growth, Corporate Profits and SPX Margins Peak --> 1H15: Employment Growth, Consumption Growth, Net Domestic Investment, Forward Multiples, Business Confidence and Consumer Confidence Peak --> 2Q/3Q15: Global Equities Peak

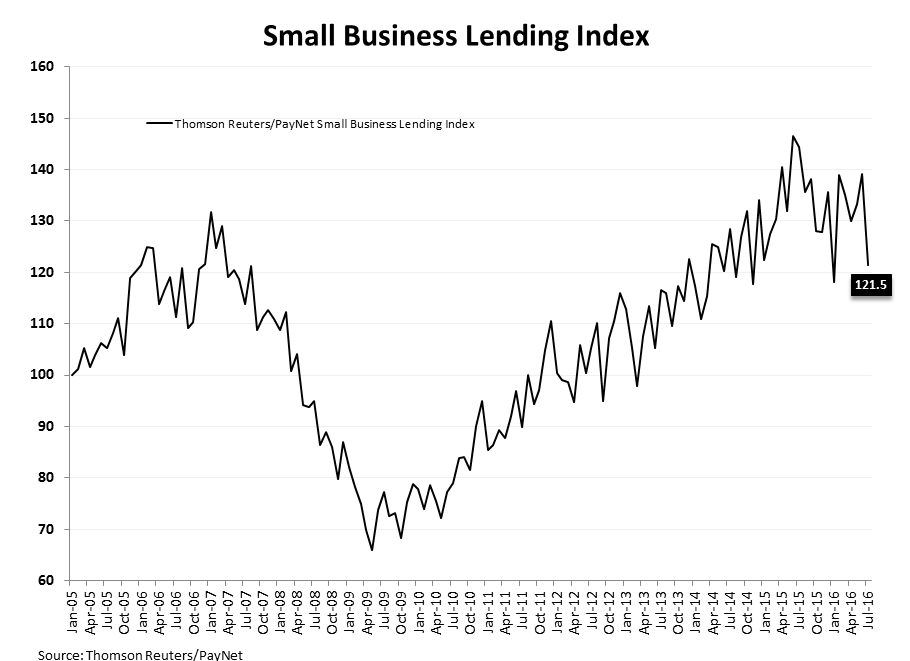

Small Business Lending ↓: Small Business lending volumes dropped -12.7% MoM in July according to the latest Thomson Reuters/Paynet Small Business Lending Index. At an index reading of 121.5, this represents the slowest pace of small business lending activity in almost two years outside of the peak growth/deflationary angst print in January.

Functionally, the slowdown in lending activity can come from tighter lending and lower credit availability, decreased demand or some combination of the two.

The Trend decline in Small Business Optimism and the continued deceleration in small business hiring support a demand side explanation. But with Small Business Deliquency rates demonstrating a fledgling negative inflection and loan standards for C&I and CRE loans across large and medium size firms showing a multi-quarter tightening according to the Fed Senior Loan Officer Survey (See: Tightening Trifecta | 3Q16 Senior Loan Officer Survey), some emergent constraint on the supply side is also not unreasonable.

Regardless of the supply/demand delineation, the growth implications are the same as ↓ lending = ↓ Spending/Investment = negative drag on growth …. And, at some point, feeds back negatively on hiring decisions.

Jobs Hard to Fill = Cycle High: The NFIB Jobs Hard to fill Index made a new cycle high of 30 in August. The challenge of finding qualified applicants has been a defining characteristic of the current expansion and one that has continued to build alongside declining labor supply and a growing spread between Job Openings and actual Hires.

There a couple of interesting potentialities that follow from this imbalance.

- If employers do find qualified applicants, it’s likely that they will have to pay up for them.

- If employers fill those positions with applicants who don’t possess the requisite skills, its likely they will still see some modest labor cost pressure give diminished labor market slack.

Given that the ability to find qualified applicants is apparently getting worse while the aggregate supply of available workers continues to decline, it’s unlikely the imbalance resolves (at least fully) via scenario A.

An obvious implication of Scenario B is that hiring people who don’t know how to do the work will not be particularly supportive of productivity – which is currently in its worst streak in 4-decades - or profitability, which remains in one of the worst non-recessionary runs of contracting earnings ever.

Whether that supply-demand-price dynamic does, in fact, characterize the future state of the labor market is an open question but some version of it is not an overly improbable scenario and the profit dystopia associated with it is evident.

Recall, aggregate nominal earnings growth has been running at a premium to nominal output growth. And if your largest input cost is growing faster than your revenue, the earnings outlook can only be so rosy. At currently prevailing demand and productivity levels, ongoing labor market strength will continued to be paid for via declining corporate profitability.

Christian B. Drake

@HedgeyeUSA